Subsection 88(1) - Winding-up

Cases

R. v. Mara Properties Ltd., 96 DTC 6309, [1996] 2 S.C.R. 161, [1996] 2 CTC 54

The taxpayer, which was in the business of developing and selling real estate, acquired, in an arm's length transaction and for a purchase price...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Loss v. Loss | land inventory retained character after wind-up | 229 |

Hickman Motors Ltd. v. The Queen, 95 DTC 5575, [1995] 2 CTC 320 (FCA), rev'd 97 DTC 5363, [1997] 2 S.C.R. 336

Hugessen J.A. rejected the taxpayer's submission that s. 88(1) established that property that was depreciable property to a subsidiary was...

Tory Estate v. M.N.R., 73 DTC 5354, [1973] CTC 434 (FCA), briefly aff'd 76 DTC 6312, [1976] CTC 415 (SCC)

The word "distributed" was held not to include a sale of accounts receivable for valuable consideration.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 70 - Subsection 70(3) | 130 | |

| Tax Topics - Statutory Interpretation - Noscitur a Sociis | 28 |

Administrative Policy

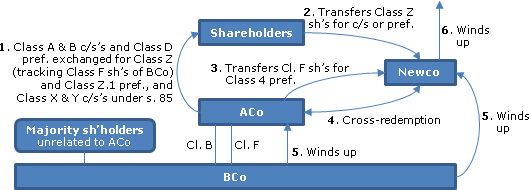

2023 Ruling 2022-0941241R3 - Internal reorganization: subs and partnerships

Background and preliminary transactions

After preliminary transactions (including the sale by Partnerships C and D of Canadian resource...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 66.7 - Subsection 66.7(16) | transfer of CRP, to the parent, out of partnerships to be wound up into the parent, to reduce risk of application of s. 66.7(16) | 229 |

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(5) | application of s. 98(5) on two successive windings-up of partnerships into parent because of the s. 88(1) wind-up of partner into parent | 267 |

11 October 2019 APFF Roundtable Q. 6, 2019-0812651C6 F - CDA and wind-up of a subsidiary

In IT-126R2, the CRA states that it considers that where the formal dissolution of a corporation is not complete but there is substantial evidence...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(2) - Paragraph 87(2)(z.1) | IT-126R2 applicable in determining when CDA of sub is added to parent’s CDA | 206 |

2014 Ruling 2014-0530371R3 - Combination of credit unions

Proposed transactions

Acquireco and Targetco, both of which are widely-held credit unions, wish to combine their businesses to form a single...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 137 - Subsection 137(4.1) | s. 137(4.1) inapplicable to Buyer of credit union who winds it up rather than becoming a member | 263 |

| Tax Topics - Income Tax Act - Section 85.1 - Subsection 85.1(1) | credit union share-for-share exchange/ cash redemption | 52 |

18 November 2014 TEI Roundtable, Q. E.4

A corporation is wound up into its parent and dissolved at a time that it had a right to receive a refund of an overpayment. Although its right to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 164 - Subsection 164(1) | refund re dissolved sub | 344 |

26 November 2014 External T.I. 2014-0551641E5 F - Winding-up and subsection 42(1)

In accordance with IT-126R2, para. 5(b), a corporation is considered to have "been wound up" on the basis that it has been liquidated and the only...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 42 | corporation permitted to claim litigation loss following effective time of winding-up | 104 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(2) | corporation permitted to claim a s. 42(1)(b) loss after (per IT-126R2) it has been wound up | 140 |

7 July 2014 External T.I. 2014-0518561E5 F - Superficial loss

Brothers A and B, who each hold 50% of the shares of Opco, dispose of those shares to Holdco (wholly-owned by Brother A.) Opco is wound-up into...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Superficial Loss | shares of Holdco as identical property to shares of Opco/transferred corporation wound-up but not dissolved within 30 days | 333 |

2014 Ruling 2013-0505431R3 - XXXXXXXXXX

In connection with an extensive reorganization, a wholly-owned subsidiary of Pubco (Newco 2) will be wound-up into Pubco. Newco 2 will be...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) | public trading in dividend recipient does not engage exclusion in s. 55(2)(a)(iv) | 848 |

| Tax Topics - Income Tax Act - Section 66.2 - Subsection 66.2(5) - Canadian development expense - Paragraph (e) | transfer of royalty from partly-owned partnership | 464 |

| Tax Topics - Income Tax Act - Section 97 - Subsection 97(2) | s. 97(2) applicable to contribution (no equity consideration) | 61 |

1 June 2004 Internal T.I. 2004-0078161I7 F - ITCs - Winding-up

After indicating that, where a subsidiary was wound up into its parent, the parent could not claim unused investment tax credits ("ITCs") of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(e.3) | ITCs incurred by sub only available to parent for post-wind-up years | 86 |

1996 Corporate Management Tax Conference Round Table, Q. 2 (C.T.O. "Wind-Up Bump Dividends")

Discussion of the effect on the "bump" of dividends paid by subsidiaries of the target corporation prior to the acquisition of control of the...

29 August 1994 External T.I. 9336515 - ADJUSTED COST BASE BUMP

An estate is not considered to acquire property from the deceased because of a bequest or inheritance for purposes of s. 88(1)(d.2). S.88(1)(d.2)...

12 August 1994 External T.I. 9415495 - AMALGAMATION/WIND-UP

Where there is a wind-up of a wholly-owned subsidiary that also owns 25% of the shares of the parent corporation, s. 88(1)(a) will deem the shares...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(3) | 42 | |

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(1) | 89 |

8 April 1994 External T.I. 9408415 - WIND-UP WITHOUT DISSOLUTION

Where a corporation has not been dissolved because it is involved in outstanding litigation, RC will accept that it has been wound up for purposes...

18 February 1994 External T.I. 9402445 - WINDING UP OF CORPORATION WITHOUT SHARE CAPITAL

The winding-up of a corporation without share capital by its sole member will not be governed by s. 88(1). Instead, s. 69(5) will apply.

92 C.R. - Q.31

The cost amount of a capital property that is debt is determined for purposes of s. 88(1)(a)(iii) pursuant to paragraph (b), rather than paragraph...

1992 A.P.F.F. Annual Conference, Q. 16 (January - February 1993 Access Letter, p. 56)

Because a licence of property or rights by a parent to its subsidiary is not extinguished until after the holder and the issuer of the license...

28 April 1992 Memorandum 912857 (C.T.0. "Winding-Up of a Canadian Corporation")

Where a corporation that otherwise would be wound up is not dissolved but is kept in existence merely to hold legal title to real estate for the...

3 September 1991 T.I. (Tax Window, No. 8, p. 21, ¶1436)

S.84(3) does not apply to deem a dividend to have been paid when shares of a corporation owned by its wholly-owned subsidiary are cancelled on the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(3) | 32 |

21 June 1991 T.I. (Tax Window, No. 4, p. 10, ¶1312)

Where a corporation ("S Co.") has owned real estate as a capital property and its shares are acquired by a corporation which includes gains from...

15 April 1991 T.I. (Tax Window, No. 2, p. 24, ¶1201)

An incorporated insurance broker will be able to claim a reserve under s. 32 on its winding-up provided that s. 88(1) applies.

25 February 1991 T.I. (Tax Window, Prelim. No. 3, p. 14, ¶1126)

A corporation will be considered to have been wound up where its assets have been distributed to the shareholders, provided the corporation has...

27 December 1990 T.I. (Tax Window, Prelim. No. 2, p. 16, ¶1072)

Late s. 88(1)(d) designations are not permitted.

21 September 1990 T.I. (Tax Window, Prelim. No. 1, p. 11, ¶1004)

Where a taxpayer inherits the shares of an investment holding company ("Fatherco") from his father at a deemed cost equal to their fair market...

June 1990 Meeting of Alberta Institute of Chartered Accountants (November 1990 Access Letter, ¶1499, Q. 2)

Dividends paid to a foreign parent by the subsidiary prior to its winding-up will not reduce the "bump" under s. 88(1)(d).

15 January 1990 T.I. (June 1990 Access Letter, ¶1265)

In response to a proposal that Corporation A, which was in the business of building apartment buildings for investment purposes, indirectly...

90 C.R. - Q40

The cost amount of inventory for purposes of s. 88(1)(a)(iii) is the value of such property immediately before the winding-up determined in...

5 September 89 T.I. (February 1990 Access Letter, ¶1110)

The cancellation, on an s. 88(1) winding-up of a wholly-owned subsidiary, of a licence of intellectual property by the parent to the subsidiary,...

IT-488R "Winding-up of 90%-Owned Taxable Canadian Corporations"

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Income-Producing Purpose | 35 |

IT-188R Archived "Sale of Accounts Receivable" 22 May 1984

An election under s. 22 is not available where debts are distributed to the parent on a winding-up under s. 88 because a sale does not take place.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 22 - Subsection 22(1) | 116 | |

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) | 17 | |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Account Receivable | 226 |

IT-126R2, "Meaning of 'Winding-Up' ", March 20, 1995

4. Generally, the dissolution of a corporation is authorized by the applicable federal or provincial statute only where it can be shown that

(a) ...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | 235 | |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(3) | 64 |

Articles

Boehmer, "Alternative to Butterfly Reorganization: Access to Investments of a Holding Company by Shareholders", Corporate Structures and Groups, Vol. IV, No. 3, p. 212

Description of considerations arising on the transfer of shares of a holding company to the operating company, followed by the winding-up of the...

Roberts, Briggs, "Winding Up", The Taxation of Corporate Reorganizations, 1996 Canadian Tax Journal, Vol. 44, Nos. 2 and 3, pp. 533, 943.

Shafer, "Liquidation", 1991 Conference Report, c. 10.

Pister, "Paragraph 88(1)(d) Bump on the Winding-up of a Subsidiary", 1990 Canadian Tax Journal, pp. 148, 426.

Williamson, "Checklists: Corporate Reorganizations, Amalgamations (Section 87), and Wind-ups (Subsection 88(1))", 1987 Conference Report, c. 29.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(1) | 0 |

Paragraph 88(1)(b)

Administrative Policy

2021 Ruling 2020-0869161R3 - Loss Carryforwards and 88(1.1)

A new corporation (the Taxpayer) was formed to acquire most of the remaining assets of a corporation (Lossco) that, together with its parent...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1.1) | accessing the losses under s. 88(1.1) of a Lossco with nominal assets | 359 |

27 November 2018 CTF Roundtable Q. 5, 2018-0780041C6 - GAAR on PUC reduction

Will CRA invoke GAAR where paid up capital (“PUC”) is reduced in the following examples to nil in order to avoid a potential s. 88(1)(b) gain...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | avoidance of s. 88(1)(b) where insufficient safe income was abusive | 393 |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(3) | no challenge of a reduction of PUC of shares of DC held by TC before redemption | 222 |

6 October 2006 Roundtable, 2006-0196011C6 F - PUC Reduction Prior To Wind-Up

GAAR will not usually be applied to a pre-dissolution reduction of paid-up capital.

2003 APFF Round Table, Q.14 (No. 2003-003-0095)

Where an operating subsidiary previously had disposed of a depreciable property having a cost amount of $100,000 to its parent for the property's...

Paragraph 88(1)(c)

See Also

Harvest Operations Corp v. A.G. (Canada), 2015 DTC 5067 [at at 5904], 2015 ABQB 327

A last-minute requirement of a Target lender for its loan to be repaid on closing resulted in the purchase price being reduced by $35M and that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Estoppel | taxpayer estoppel when it claimed a tax benefit from its mistake rather than promptly seeking rectification | 206 |

| Tax Topics - General Concepts - Rectification & Rescission | requested rectification order to fix bump did not match parties' specific plan at closing | 614 |

Administrative Policy

4 March 2025 External T.I. 2024-1009691E5 F - Bump and Qualifying Exchange

Parent acquired for $75,000 all of the outstanding shares of another taxable Canadian corporation (the Subsidiary), whose only property was a...

Articles

Steve Suarez, "Canada's 88(1)(d) Tax Cost Bump: A Guide for Foreign Purchasers", Tax Notes International, December 9, 2013, p. 935

Changes to directly-held properties before acquisition of control ("AOC") (p. 941)

The requirement [in the midamble of s. 88(1)(c)] that eligible...

Subparagraph 88(1)(c)(ii)

Administrative Policy

27 October 2006 External T.I. 2005-0157321E5 F - Winding-up of a wholly-owned corporation

Does the character of a property (here, eligible capital property) acquired by a parent corporation on the winding-up of a wholly-owned subsidiary...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Goodwill | character of property usually regarded as retained in the hands of the parent | 170 |

Subparagraph 88(1)(c)(iii)

Administrative Policy

20 April 2005 External T.I. 2005-0110421E5 F - ACB BUMP on an AMALGAMATION

Immediately prior to the amalgamation of Holdco with Opco, the only assets of Opco were woodlots. In finding that the cost of the land could not...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(21) - Depreciable Property | land included in timber limit is depreciable property | 127 |

Subparagraph 88(1)(c)(v)

Administrative Policy

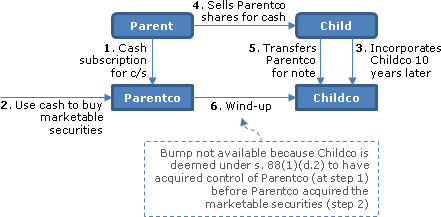

31 October 2011 External T.I. 2011-0422981E5 F - Whether property is eligible for a bump

{kind=link}

In 2000, an individual ("Parent") subscribed cash for common shares on the incorporation of "Parentco", with Parentco purchasing marketable...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c) - Subparagraph 88(1)(c)(vi) | bump unavailable given previous non-arm's length acquisition | 153 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(d.2) | properties not bumpable as not owned at subsidiary's formation by related person | 401 |

25 February 2002 External T.I. 2000-0046485 F - Majoration et Immobilisation

Mr. X owned Aco and Bco, whose principal asset was 80% (80 units) or 20% (20 units) of an eligible capital property. In connection with Mr. X...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c) - Subparagraph 88(1)(c)(vi) - Clause 88(1)(c)(vi)(B) - Subclause 88(1)(c)(vi)(B)(I) | reciprocal transactions entailed acting in concert, so that the bump was denied under s. 88(1)(c)(vi)(B)(I) given resulting specified shareholder status | 323 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(d.2) | reciprocal transactions entailed acting in concert, so that the bump was denied under s. 88(1)(c) and (d.2) by virtue of backdating acquisition of acquisition of control by parent | 321 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | co-operative use of s. 88(1)(d) bump by targets and purchasers could entail acting in concert | 100 |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Shares | arguable that preferred shares received on s. 85(1) rollover basis for eligible capital property transfer, and immediately sold, were not capital property | 62 |

Articles

Steve Suarez, "Canada's 88(1)(d) Tax Cost Bump: A Guide for Foreign Purchasers", Tax Notes International, December 9, 2013, p. 935

Purpose of anti-stuffing rule in s

88(1)(c)(v) (p. 942)

Another rule is meant to prevent the parent from transferring property with accrued gains...

Subparagraph 88(1)(c)(vi)

Administrative Policy

2014 Ruling 2013-0503611R3 - Post-Mortem Planning

{kind=link}

Overview of transactions

A testamentary spousal trust (the "Spousal Trust") whose basis in pref shares of a portfolio investment company...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | pipeline following death of spouse for a spousal trust where company holds mostly marketable securities | 585 |

17 February 2012 External T.I. 2011-0428561E5 - 88(1)(c)(vi) Bump Denial Rule

following the death of Ms. X, who was the second wife of her previously-deceased husband, Holdco is controlled by A and B (children of the first...

31 October 2011 External T.I. 2011-0422981E5 F - Whether property is eligible for a bump

In 2000, an individual ("Parent") subscribes cash on the incorporation of "Parentco" with Parentco purchasing marketable securities a few hours...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c) - Subparagraph 88(1)(c)(v) | properties not bumpable as the subsidiary control was deemed by s. 88(1)(d.2) to be acquired at the same time as it acquired the properties | 634 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(d.2) | properties not bumpable as not owned at subsidiary's formation by related person | 401 |

19 March 2003 T.I.

For the purpose of clause 88(1)(c)(vi)(A) of the Act, the reference to the term 'acquire control' means the time that the parent actually acquired...

17 November 2000 External T.I. 1999-0008585 - Winding-up

"The determination of whether a person is a 'specified person' for purposes of subclause 88(1)(c)(vi)(B)(I) of the Act is made at the time any...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | 45 |

29 October 1998 External T.I. 9821355 - WINDING-UP "BUMP"

Where Target transferred a depreciable property to a newly incorporated wholly-owned subsidiary (Newco) in exchange for newly issued treasury...

Articles

David Carolin, Marissa Halil, Manu Kakkar, "Grandchildren Can Trump the Bump?", Tax for the Owner-Manager, Vol. 26, No. 2, April 2026, p. 6

S. 88(1)(c)(vi) bump denial rule (pp. 6-7)

- S. 88(1)(c)(vi) denies the s. 88(1)(d) bump where a prohibited person receives bumped property.

- In...

Peter Lee, Paul Stepak, "PE Investments in Canadian Companies", draft 2017 CTF Annual Conference paper

Potential unavailability of “bump and run” where management are expected to retain interest in company (p. 15)

Where Target is a 10(f)...

Paul Stepak, Eric C. Xiao, "The 88(1)(d) Bump – An Update", 2013 Conference Report (Canadian Tax Foundation), pp.13:1-60

Sequencing of steps (p. 13:35)

The steps set out in the plan generally include the repayment of historic Target debt, the cash-out or rollover of...

Brian R. Carr, Julie A. Colden, "The Bump Denial Rules Revisited", Canadian Tax Journal (2014) 62:1, 273-99.

Purpose of bump denial rules (p. 276)

…Generally, the bump denial rules were introduced into the Act to prevent so-called back-door...

Steve Suarez, "Canada's 88(1)(d) Tax Cost Bump: A Guide for Foreign Purchasers", Tax Notes International, December 9, 2013, p. 935

Policy of bump denial rules (p. 946)

The policy behind the bump denial rule is deceptively simple: The parent should not be able to buy and wind...

Mark Jadd, Richard Lewin, "Anatomy of a Deal: Income Tax Issues Facing a Non-Resident Purchaser of a Public Canadian Corporation", International Tax (CCH), October 2006, No. 30 p. 9.

Nathan Boidman, "Unwinding or Otherwise Dealing With 'Sandwich' Structures Resulting From an International Merger or Acquisition", Tax Notes International, 10 May 2004, p. 601: Discussion of restrictions on bump where a Canadian corporation has been acquired by a foreign acquiror.

Clause 88(1)(c)(vi)(B)

Subclause 88(1)(c)(vi)(B)(I)

Administrative Policy

3 December 2024 CTF Roundtable Q. 7, 2024-1038221C6 - Post-Mortem Pipeline Bump Planning

The estate of an individual who, on death, wholly-owned Aco, included a charity entitled to 11% of the Estate. The Estate will implement a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(d.2) | an 11% estate beneficiary becomes a specified shareholder of the deceased’s corp. concurrently with its deemed acquisition under ss. 88(1)(d.2) and (d.3) | 266 |

16 November 2004 External T.I. 2004-0064821E5 F - 88(1) Bump

A third party (Buyco) acquires a 70% equity stake in Opco (previously wholly-owned by Holdco, with which Buyco dealt at arm’s length) by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c.3) - Subparagraph 88(1)(c.3)(ii) | acquisition by Buyco of Target shares before its acquisition of control accommodated through restrictive interpretation of s. 88(1)(c.3)(ii) | 245 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c.3) - Subparagraph 88(1)(c.3)(i) | example of situation where the acquisition of shares of parent by vendor would not be within s. 88(1)(c.3)(i), but would fall within s. 88(1)(c.3)(ii) | 58 |

25 February 2002 External T.I. 2000-0046485 F - Majoration et Immobilisation

Mr. X owned Aco and Bco, whose principal asset was 80% (80 units) or 20% (20 units) of an eligible capital property. In connection with Mr. X...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c) - Subparagraph 88(1)(c)(v) | reciprocal transactions entailed acting in concert, so that the bump was denied under s. 88(1)(c)(v) | 296 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(d.2) | reciprocal transactions entailed acting in concert, so that the bump was denied under s. 88(1)(c) and (d.2) by virtue of backdating acquisition of acquisition of control by parent | 321 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | co-operative use of s. 88(1)(d) bump by targets and purchasers could entail acting in concert | 100 |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Shares | arguable that preferred shares received on s. 85(1) rollover basis for eligible capital property transfer, and immediately sold, were not capital property | 62 |

Subclause 88(1)(c)(vi)(B)(II)

Administrative Policy

28 November 2010 CTF Annual Roundtable Q. 19, 2010-0386041C6 - Deemed ownership of shares

Is the reference to "all of the shares" in s. 88(1)(c)(vi)(B)(II) a reference only to shares of a subsidiary that is subsequently wound-up into...

Articles

Paul Stepak, Eric C. Xiao, "The 88(1)(d) Bump – An Update", 2013 Conference Report (Canadian Tax Foundation), pp.13:1-60

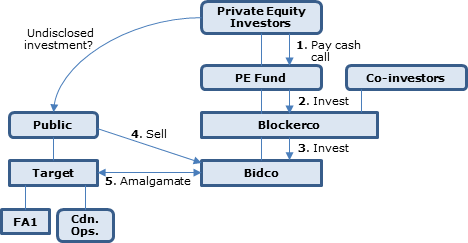

Cash calls on private equity investors who also are prohibited persons (pp. 13:38-39)

Figure 9

{kind=link}

Private equity (PE) buyers can raise challenging...

Brian R. Carr, Julie A. Colden, "The Bump Denial Rules Revisited", Canadian Tax Journal (2014) 62:1, 273-99.

Overview of aggregation rule (p. 283)

In addition, the bump will be denied if distributed property or substituted property is acquired as part of...

Subclause 88(1)(c)(vi)(B)(III)

Administrative Policy

2013 Ruling 2011-0397081R3 - Bump Transaction

{kind=link}

Buyer

Buyer is a listed non-resident corporation, and owns all but the exchangeable shares of a Canadian public corporation ("BuyerSub"). ...

Articles

Brian R. Carr, Julie A. Colden, "The Bump Denial Rules Revisited", Canadian Tax Journal (2014) 62:1, 273-99.

Specified shareholder must not also own 10% of shares of an acquiror (either alone or with non-arm's length persons): s....

Paragraph 88(1)(c.2)

Subparagraph 88(1)(c.2)(i)

Articles

Paul Stepak, Eric C. Xiao, "The 88(1)(d) Bump – An Update", 2013 Conference Report (Canadian Tax Foundation), pp.13:1-60

Parent relatedness to mooted specifed person from moment of its incorporation if not a shelf corp. (p. 13:22-23)

[A]t the time the parent is...

Brian R. Carr, Julie A. Colden, "The Bump Denial Rules Revisited", Canadian Tax Journal (2014) 62:1, 273-99.

Related status before incorporator's share issuance (p. 297)

The joint [CBA/CICA] committee noted in its submission that there are deficiencies in...

Steve Suarez, "Canada's 88(1)(d) Tax Cost Bump: A Guide for Foreign Purchasers", Tax Notes International, December 9, 2013, p. 935

Examples of prohibited persons (pp. 947-8)

The most useful way to illustrate the wide range of potential prohibited persons is by using the...

{kind=link}

Subparagraph 88(1)(c.2)(ii)

Articles

Brian R. Carr, Julie A. Colden, "The Bump Denial Rules Revisited", Canadian Tax Journal (2014) 62:1, 273-99.

Look-through specified shareholder definition v. s. 88(1)(c.2)(ii) entity approach (p. 288)

As a result of the interaction of subparagraph...

Subparagraph 88(1)(c.2)(iii)

Clause 88(1)(c.2)(iii)(A)

Articles

Paul Stepak, Eric C. Xiao, "The 88(1)(d) Bump – An Update", 2013 Conference Report (Canadian Tax Foundation), pp.13:1-60

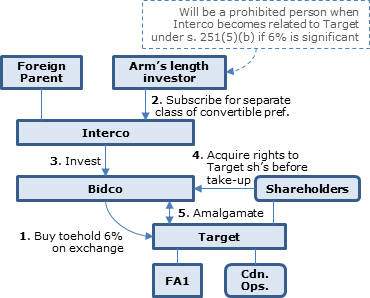

Meaning of "significant" in s. 88(1)(c.2)(iii)(A) (pp. 13:46-48)

{kind=link}

[F]oreign Parent owns Interco, which owns Bidco. Bidco has acquired a toehold...

Clause 88(1)(c.2)(iii)(A.2)

Articles

Paul Stepak, Eric C. Xiao, "The 88(1)(d) Bump – An Update", 2013 Conference Report (Canadian Tax Foundation), pp.13:1-60

Remedying under s. 88(1)(d)(c.2)(iii)(A.2) of pre-winding-up agreement for sale of bumped shares

[P]rior to the [s. 88(1)(d)(c.2)(iii)(A.2)]...

Paragraph 88(1)(c.3)

Subparagraph 88(1)(c.3)(i)

Administrative Policy

2012 Ruling 2012-0451421R3 - Purchase of Target and bump

Ruling that Parent guarantees of the amended notes of Target will not constitute substituted property as described in s. 88(1)(c.3). See detailed...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(18) - Paragraph 212.3(18)(c) | deemed investment on amalgamation of subsidiary | 833 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(4) - Paragraph 88(4)(b) | Target Amalco 2 formed post-AOC and pre-bump (occurring on amalgamation of Target Amalco 2 with Bidco) is a continuation its predecessors for s. 88(1)(c) midamble purposes/prepackaging transactions before formation of Target Amalco 2/Target asset buyers agree not to purchase Target shares | 995 |

16 November 2004 External T.I. 2004-0064821E5 F - 88(1) Bump

CRA noted that an example of a situation where the acquisition of shares of a parent corporation by the vendor would not be covered by s....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c.3) - Subparagraph 88(1)(c.3)(ii) | acquisition by Buyco of Target shares before its acquisition of control accommodated through restrictive interpretation of s. 88(1)(c.3)(ii) | 245 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c) - Subparagraph 88(1)(c)(vi) - Clause 88(1)(c)(vi)(B) - Subclause 88(1)(c)(vi)(B)(I) | where Buyco acquired Target shares before acquiring control of Target, Vendor would be a person described in s. 88(1)(c)(vi)(B)(I) | 217 |

31 January 2000 External T.I. 1999-0010965 - EARNOUT CLAUSES AND INELIGIBLE PROPERTY

"Where an earn-out or any similar type of agreement is clearly for the sole purpose of providing a mechanism to determine the fair market value...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c.3) - Subparagraph 88(1)(c.3)(ii) | earn-out | 97 |

Articles

Warren Pashkowich, Daniel Bellefontaine, "Participation-Based Payments: What Are They and How are They Taxed", 2017 Conference Report (Canadian Tax Foundation), 9:1-25

Potential treatment of earnout as substituted property (p. 9: 12)

[T]here can be a denial of the bump where property distributed on the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(g) | 351 |

Ian Crosbie, "Recent Transactions of Interest, Part I", 2015 CTF Annual Conference paper

Application of substituted property rules where consideration paid to target (Kodiak) shareholders was over 10% of shares of U.S. acquiror...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(2) | 729 |

Paul Stepak, Eric C. Xiao, "The 88(1)(d) Bump – An Update", 2013 Conference Report (Canadian Tax Foundation), pp.13:1-60

10% attributable property test applied only during the series of transactions (p. 13:12-13)

[W]hen read in a textual, contextual and purposive...

Brian R. Carr, Julie A. Colden, "The Bump Denial Rules Revisited", Canadian Tax Journal (2014) 62:1, 273-99.

Upstream equity or debt as substituted property (p. 280)

Any upstream equity interests (such as shares of the parent or other upper-tier...

Steve Suarez, "Canada's 88(1)(d) Tax Cost Bump: A Guide for Foreign Purchasers", Tax Notes International, December 9, 2013, p. 935

10%-plus properties as prohibited property (p. 951)

2. Property Deriving More Than 10 Percent of Its FMV From Distributed Property Post-AOC...

Carrie Smit, "Amendments to 'Bump' Rules May Permit Foreign Shares as Deal Consideration", International Tax, No. 68, February 2013, p.1

… where a foreign purchaser ("Forco") sets up a Canadian acquisition corporation ("Bidco") to acquire a Canadian target company ("Canco"), and...

Subparagraph 88(1)(c.3)(ii)

Administrative Policy

16 November 2004 External T.I. 2004-0064821E5 F - 88(1) Bump

A third party (Buyco) acquires a 70% equity stake in Opco (previously wholly-owned by Holdco, with which Buyco dealt at arm’s length) by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c) - Subparagraph 88(1)(c)(vi) - Clause 88(1)(c)(vi)(B) - Subclause 88(1)(c)(vi)(B)(I) | where Buyco acquired Target shares before acquiring control of Target, Vendor would be a person described in s. 88(1)(c)(vi)(B)(I) | 217 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c.3) - Subparagraph 88(1)(c.3)(i) | example of situation where the acquisition of shares of parent by vendor would not be within s. 88(1)(c.3)(i), but would fall within s. 88(1)(c.3)(ii) | 58 |

31 January 2000 External T.I. 1999-0010965 - EARNOUT CLAUSES AND INELIGIBLE PROPERTY

"Where an earn-out or any similar type of agreement is clearly for the sole purpose of providing a mechanism to determine the fair market value...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c.3) - Subparagraph 88(1)(c.3)(i) | earn-out | 97 |

7 August 1998 External T.I. 9727435 - BUMP-REVERSE TAKEOVER

Respecting the acquisition by a public company (Aco) of shares of another public company (Bco) in a reverse takeover, CRA stated that "the shares...

Income Tax Technical News, No. 9, 10 February 1997

The words "wholly or partly attributable to" in subparagraph 88(1)(c.3)(i) are very broad and would apply, for example, to a share or interest in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Other Legislation/Constitution - Federal - Indian Act - Section 87 | 30 | |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Subparagraph 212(1)(b)(vii) | events must be beyond borrower's control | 79 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | loss transfer must be to affiliated person - related not enough | 50 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | 71 | |

| Tax Topics - Income Tax Regulations - Regulation 4900 - Subsection 4900(12) | 71 | |

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(1) - Paragraph 53(1)(e) - Subparagraph 53(1)(e)(i) | avoidance of double taxation through absence of ACB adjustment | 137 |

Articles

Firoz Ahmed, "Substituted Property for Purposes of the Section 88(1)(d) Bump", Canadian Current Tax, Vol. 7, No. 7, April 1997, p. 70

Where a public corporation ("Smallco") makes a successful takeover bid for another corporation ("Bigco"), RC is prepared to rule that shares of...

Paragraph 88(1)(c.4)

Articles

Angelo Nikolakakis, Alain Léonard, "The Acquisition of Canadian Corporations by Non-Residents: Canadian Income Tax Considerations Affecting Acquisition Strategies and Structure, Financing Issues, and Repatriation of Profits", 2005 Conference Report (Canadian Tax Foundation), 21:1-61, at 21:24-25:

Policy for exclusion of shares or debt of foreign corporations (p. 280)

Why is it that shares of a non-resident Bidder should not constitute...

Subparagraph 88(1)(c.4)(ii)

Articles

Paul Stepak, Eric C. Xiao, "The 88(1)(d) Bump – An Update", 2013 Conference Report (Canadian Tax Foundation), pp.13:1-60

Is debt of Target non-specified property after it is amalgamated with Bidco? (pp. 13:16-19)

On a literal reading of old paragraph 88(1)(c.3),...

Brian R. Carr, Julie A. Colden, "The Bump Denial Rules Revisited", Canadian Tax Journal (2014) 62:1, 273-99.

Dissent payment rights under a plan of arrangemnt as indebtedness (p. 292)

If the plan of arrangement ultimately receives shareholder approval,...

Paul Stepak, J. Scott Wilkie, "Relieving and Clarifying Changes to Canadian Bump Rules", Corporate Finance, Volume XVIII, No. 3, 2012, p. 2130 at 2132:

- Indebtedness issued for money is specified property – this rule now confirms, from and after 2001, that indebtedness issued solely for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c.9) | 96 |

Paragraph 88(1)(c.9)

Articles

Paul Stepak, Eric C. Xiao, "The 88(1)(d) Bump – An Update", 2013 Conference Report (Canadian Tax Foundation), pp.13:1-60

Options granted by virtue of employment not part of series (p. 13:29)

[A] stock option granted to an employee by Bidco or Bidco's Canadian parent...

Brian R. Carr, Julie A. Colden, "The Bump Denial Rules Revisited", Canadian Tax Journal (2014) 62:1, 273-99.

No relief under s. 88(1)(c.9) for conventional option exchange (pp. 294-5)

Technically, however, the proposed amendment provides no relief if an...

Paul Stepak, J. Scott Wilkie, "Relieving and Clarifying Changes to Canadian Bump Rules", Corporate Finance, Volume XVIII, No. 3, 2012, p. 2130 at 2132:

- References to a share in the definition of specified property includes a right to acquire a share – this rule now confirms, from and after...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c.4) - Subparagraph 88(1)(c.4)(ii) | 89 |

Paragraph 88(1)(d)

Cases

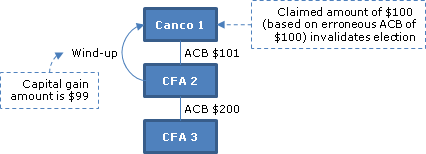

Deml Investments Limited v. Canada, 2025 FCA 204

In finding that it abused s. 88(1)(d) to bump the ACB of the interest in a Canadian partnership (DERP 2) holding Canadian resource properties for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | it abused the rationale of s. 88(1)(d) to bump the ACB of a resource partnership interest | 631 |

Canada v. Oxford Properties Group Inc., 2018 FCA 30

When Oxford Properties was sold to an OMERS subsidiary, the purchaser first negotiated that Oxford would drop various properties down into LPs on...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | using the s. 88(1)(d) bump on newly-formed rental property LPs to avoid indirect recapture income under s. 100(1) was abusive | 975 |

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(3) - Paragraph 98(3)(c) | s. 98(3)(c) bump is intended to avoid gain realization where there has been no economic gain | 267 |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(11) | 3-year time limitation in s. 69(11) did not establish safe harbor for avoidance of recapture on sale after that period | 382 |

| Tax Topics - Income Tax Act - Section 100 - Subsection 100(1) | purpose is to ensure that latent recapture will be recognized on sale to tax exempt | 254 |

| Tax Topics - Income Tax Act - Section 97 - Subsection 97(2) | object includes ultimate taxation of the deferred gain | 234 |

| Tax Topics - Income Tax Act - Section 171 - Subsection 171(1) | GAAR question as to determining a provision’s object was subject to correctness standard | 169 |

| Tax Topics - Statutory Interpretation - Hansard, explanatory notes, etc. | statement that amendment was for “clarification” was self-serving | 209 |

| Tax Topics - Statutory Interpretation - Interpretation Act - Subsection 45(2) | determination of whether amendment merely clarified requires review of pre-amendment state of law | 146 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(2) | consequential s. 245(2) adjustment must be scaled to the abuse | 391 |

See Also

Oxford Properties Group Inc. v. The Queen, 2016 TCC 204, rev'd 2018 FCA 30

A corporation (“BPC”), which was mostly owned by a Canadian pension fund (“OMERS”), obtained the agreement of a predecessor of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | no abuse in using 88(1)(d) bump to avoid s. 100 after 3-year s. 69(11) period | 557 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | subsequent sale part of series as it utilized the benefit of previous LP packaging and bump transactions | 387 |

| Tax Topics - Income Tax Act - Section 97 - Subsection 97(2) | purpose not to tax underlying recapture on subsequent LP unit sale | 431 |

| Tax Topics - Statutory Interpretation - Interpretation Act - Subsection 45(2) | subsequent amendment shed light on scope of previous version | 107 |

| Tax Topics - Income Tax Act - Section 100 - Subsection 100(1) | S. 100 operates only on outside basis gain | 290 |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(11) | Parliament provided safe harbour for sales after 3 years | 204 |

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(3) - Paragraph 98(3)(c) | purpose: to preserve high outside basis through push down | 293 |

Slate Management Corporation v Canada (Attorney General), 2016 ONSC 4216

A purchaser used a newly-formed AcquisitionCo to acquire a Target, and asked for and received a computation from its accounting firm of the amount...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Rectification & Rescission | a generalized intent to achieve a s. 88(1)(d) bump was a sufficient basis to rectify in order to redo an amalgamation | 202 |

Administrative Policy

30 May 2019 Internal T.I. 2019-0806761I7 - Late filing of 88(1)(d) designation

A non-resident corporation formed a Canadian “Acquireco,” which acquired all the shares of a public corporation, and then vertically...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4) - Paragraph 152(4)(b) - Subparagraph 152(4)(b)(iii) | late designation policy coordinated with extended reassessment period | 242 |

14 March 2016 Internal T.I. 2015-0609671I7 - Earnout, Amalgamation, Cost of Shares and ECE

Pursuant to a share purchase agreement, Acquisitionco (a newly-formed Canadian subsidiary of another corporation) purchased all the outstanding...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 14 - Subsection 14(5) - Eligible Capital Expenditure | payments made by Amalco in satisfaction of earnout obligation for acquisition of one precedessor by the other were not ECE | 224 |

| Tax Topics - Income Tax Act - Section 54 - Adjusted Cost Base | earnout payments an addition to cost of shares which had since disappeared | 150 |

| Tax Topics - General Concepts - Purpose/Intention | attribution of predecessor's intention to Amalco | 140 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) - Subparagraph 20(1)(c)(i) | position on interest deductibility following target amalgamation is based on policy and ITA scheme rather than technical | 350 |

30 March 2016 External T.I. 2016-0629701E5 F - bump-up 88(1)(d)

Mr. A holds all the shares of Corporation A, whose only property which is capital property with an ACB of $100,000. Corporation B, which is an...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Real Estate | land developer accesses capital property status of land held in acquired subsidiary | 64 |

S4-F7-C1 - Amalgamations of Canadian Corporations

1.39 …[T]he designation of any bump amount must normally be made in the new corporation's Part I income tax return for its first tax year....

21 November 2011 External T.I. 2011-0416881E5 F - Late-filed designation - paragraph 88(1)(d)

CRA generally allows a late-filed designation under s. 88(1)(d) to the extent that (1) the parent corporation agrees to allocate the excess...

19 May 2011 IFA Roundtable, 2011-0404521C6 - calculation of tax-free surplus balance

In the situation where the Canadian target holding a foreign affiliate (FA) is wound up into the Canadian acquisition company (resulting in a...

7 January 2009 External T.I. 2008-0286111E5 F - 88(1)d) and 87(11)-Late-filed designation

Regarding its position regarding a late designation under ss. 88(1)(d) and 87(11), CRA stated:

... CRA ... allow[s] on an administrative basis, a...

2006 Ruling 2006-0178571R3 - Purchase of Target and Bump

Bump ruling provided respecting transactions which apparently involved the transfer of assets on a rollover basis by the target (Mergeco), with...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(1) | amalgamation with parent as survivor (forward triangular "D" merger) | 588 |

2 August 2001 External T.I. 2001-0074575 F - Désignation - Validité

The parent corporation designated an excessive amount in respect of a particular capital property of the subsidiary that was distributed to it on...

23 October 1995 External T.I. 9513425 - ARM'S LENGTH TEST

Where Acquisitionco, subsequent to its acquisition of Targetco and prior to the winding-up of Targetco and its child and grandchild subsidiaries...

1994 A.P.F.F. Round Table, Q. 14

Section 8 of Supplement 12 IC88-2 (respecting the incorporation by Target Corporation of its three businesses prior to the purchaser of Target...

10 February 1993 T.I. (Tax Window, No. 28, p. 12, ¶2405)

No late election can be made under s. 88(1)(d).

26 August 1992, T.I. (Tax Window, No. 23, p. 13, ¶2168)

S.88(1)(d) merely requires that a property be a capital property to the subsidiary at the time the parent last acquired control of the subsidiary...

21 May 1991 T.I. (Tax Window, No. 3, p. 9, ¶1260)

The parenthetical words ("other than a corporation acquired by [the parent] from a person with whom it was dealing at arm's length") at the end of...

Articles

K.A. Siobhan Monaghan, "Safe Income and the Elusive Subsection 88(1) 'Bump' - and other Problems in a Series", Corporate Structures and Groups, Vol. V, No. 3, 1999, p. 274.

Mark D. Brender, "Interaction of the Mark-to-Market Rules with Step-Up Transactions", Corporate Structures and Groups, Vol. V, No. 2, 1998, p. 256.

M. Ton-That, "Changes to the 'Bump' Rules: Transactions Where It Can Now Be Denied", Corporate Structures and Groups, Vol. V, No. 1, 1998, p. 244.

Subparagraph 88(1)(d)(i)

Administrative Policy

28 January 2016 External T.I. 2015-0617771E5 F - Bump calculation

Is the balance of the “future income tax liabilities” (being an accounting provision which was not deducted in computing income) presented in...

Subparagraph 88(1)(d)(i.1)

Articles

Henry Shew, Florence Marino, "The interaction between corporate-owned life insurance and bump transaction",

Bump may be combined with use of insurance-generated CDA (p.3)

- In post-mortem pipeline transactions, the estate might transfer shares of...

Subparagraph 88(1)(d)(ii)

Administrative Policy

23 April 2013 External T.I. 2012-0461741E5 - Calculation of bump limit under 88(1)(d)

At the date of acquisition of control of the subsidiary by the parent, it owns 3,000 shares of a public corporation with a cost of $10,000 (for an...

Articles

Steve Suarez, "Canada's 88(1)(d) Tax Cost Bump: A Guide for Foreign Purchasers", Tax Notes International, December 9, 2013, p. 935

Buy, bump and sell transactions of foreign acquirer (p. 937)

The introduction of the foreign affiliate dumping (FAD) rules in 2012 makes the...

Variable C

Administrative Policy

17 May 2023 IFA Roundtable Q. 8, 2023-0964561C6 - Tax-free Surplus Balance and Paragraph 88(1)(d)

2011-0404521C6 indicated that in the situation where the Canadian target holding a foreign affiliate (FA) is wound up into the Canadian...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5905 - Subsection 5905(5.4) | no surplus calculations needed where FA of Canadian target is acquired by Forco through a Cdn. Buyco and then promptly bumped (under s. 88(1)(d)) and distributed to Forco | 250 |

Subparagraph 88(1)(d)(ii.1)

Articles

Steve Suarez, "Canada's 88(1)(d) Tax Cost Bump: A Guide for Foreign Purchasers", Tax Notes International, December 9, 2013, p. 935

Summary of s. 88(1)(d)(ii.1)

… Expressed conceptually, the FMV of the partnership interest is deemed to be reduced by an amount representing...

Paragraph 88(1)(d.2)

See Also

3295940 Canada Inc. v. The Queen, 2022 TCC 68, rev'd 2024 FCA 42

The taxpayer (3295940) was a holding company holding a shareholding in a Target with a low ACB (even after using safe income on hand to step up...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | circular use of capital dividends abused the purpose of the CDA | 966 |

| Tax Topics - Income Tax Act - Section 83 - Subsection 83(2) | use of capital dividend to avoid s. 55(2) abused the capital dividend system | 533 |

Administrative Policy

3 December 2024 CTF Roundtable Q. 7, 2024-1038221C6 - Post-Mortem Pipeline Bump Planning

The estate of an individual who, on death, wholly-owned Aco, included a charity entitled to 11% of the Estate. The Estate will implement a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c) - Subparagraph 88(1)(c)(vi) - Clause 88(1)(c)(vi)(B) - Subclause 88(1)(c)(vi)(B)(I) | estate beneficiary not considered to acquire 10% interest in estate company prior to deemed s. 88(1)(d.2) and (d.3) acquisition | 236 |

31 October 2011 External T.I. 2011-0422981E5 F - Whether property is eligible for a bump

{kind=link}

In 2000, an individual ("Parent") subscribed cash for common shares on the incorporation of "Parentco", with Parentco purchasing marketable...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c) - Subparagraph 88(1)(c)(v) | properties not bumpable as the subsidiary control was deemed by s. 88(1)(d.2) to be acquired at the same time as it acquired the properties | 634 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c) - Subparagraph 88(1)(c)(vi) | bump unavailable given previous non-arm's length acquisition | 153 |

25 February 2002 External T.I. 2000-0046485 F - Majoration et Immobilisation

Mr. X owned Aco and Bco, whose principal asset was 80% (80 units) or 20% (20 units) of an eligible capital property. In connection with Mr. X...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c) - Subparagraph 88(1)(c)(v) | reciprocal transactions entailed acting in concert, so that the bump was denied under s. 88(1)(c)(v) | 296 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c) - Subparagraph 88(1)(c)(vi) - Clause 88(1)(c)(vi)(B) - Subclause 88(1)(c)(vi)(B)(I) | reciprocal transactions entailed acting in concert, so that the bump was denied under s. 88(1)(c)(vi)(B)(I) given resulting specified shareholder status | 323 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | co-operative use of s. 88(1)(d) bump by targets and purchasers could entail acting in concert | 100 |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Shares | arguable that preferred shares received on s. 85(1) rollover basis for eligible capital property transfer, and immediately sold, were not capital property | 62 |

17 July 1995 External T.I. 9505095 - MEANING OF "BECAUSE OF A BEQUEST OR INHERITANCE"

Where the shares of a Canadian corporation are held by the estate of the deceased shareholder until probate, then distributed to the beneficiary,...

Articles

Julien Théberge, "The Interaction Between Corporate-Owned Life Insurance and Bump Transactions", Tax for the Owner-Manager, Vol. 20, No. 2, April 2020, p. 3

No bump on IBT because of application of s. 88(1)(d.2) (pp. 2-3)

- In an intergenerational business transfer (“IBT”), there generally is no...

Paragraph 88(1)(d.3)

Administrative Policy

2021 Ruling 2021-0887301R3 F - Post-mortem pipeline transaction

Father bequested his shares of an investments holding company (Aco) directly to his surviving wife (Mother) and to a spousal trust (Trust) for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | double pipeline entailing the application of s. 84.1 and s. 88(1)(d) bump | 368 |

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2) - Paragraph 84.1(2)(a.1) - Subparagraph 84.1(2)(a.1)(ii) | application of ss. 84.1(1) and (2)(a.1)(ii) to transfer of shares by spousal trust that had received such shares from the testator who had stepped such shares up under s. 110.6(2.1) | 194 |

15 June 2022 STEP Roundtable Q. 7, 2022-0928291C6 - paragraph 88(1)(d.3)

2009-0350491R3 ruled on the use of an alter ego trust of the s. 88(1)(d) bump following the death of its settlor and life beneficiary (Mr. X). At...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(4) - Paragraph 104(4)(a.4) | deemed disposition under s. 104(4)(a.4) is not itself sufficient to access s. 88(1)(d.3) regarding a subsidiary of the trust | 252 |

2021 Ruling 2019-0800431R3 - Alter Ego Post-mortem Pipeline and Bump Planning

Around when he was placed in a long-term care facility, the “Deceased” transferred his shares of two companies with investing businesses (Aco...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | pipeline for alter ego trust with preliminary elimination of NR beneficiary and application of s. 88(1)(d.3) | 367 |

| Tax Topics - Income Tax Act - Section 212.1 - Subsection 212.1(6) - Paragraph 212.1(6)(b) | pipeline ruling for an alter ego trust includes a preliminary deletion of a non-resident beneficiary | 233 |

2020 Ruling 2020-0860231R3 - Post-mortem planning

CRA ruled on pipeline transactions respecting common shares of Opco which the deceased held on death, in which:

- the estate transfers its common...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | redemption of shares stepped up with CGD, giving rise to s. 164(6) carryback, and pipeline followed by s. 88(1)(d) bump, having regard to s. 88(1)(d.2) and (d.3) | 516 |

2010 Ruling 2009-0350491R3 - Alter Ego Trust Planning

The terms of an alter ego trust (the “Trust”) established by Mr. X, and to which he had transferred all the common shares of XCO (which, in...

Articles

Brian Nichols, "Post-Mortem Tax Planning Using Paragraph 88(1)(d) Bumps", Tax Topics, No. 1609, 9 January 2003, p. 1.

In order to take advantage of the "reset" effect of paragraph 88(1)(d.3), care must be taken to ensure that a child does not obtain de jure...

Rhonda Rudick, "Bump Denial Rules: Time of Acquisition of Control in the Context of Post-Mortem Estate Planning", Corporate Structures and Groups (Federated Press), Vol. VII, No. 1, 2001, p. 355.

Son already had s. 186(2) control of Opco

[A]n individual (father) dies on October 1, 2001 and leaves all of his assets to his son, who is also...

Paragraph 88(1)(e)

Articles

Kevin Yip, "Recent Legislation Affecting Partnerships and Foreign Affiliates – Subsection 88(1) and Section 100", Canadian Tax Journal, (2013) 61:1, 229-256, at 245

After noting that s. 88(1)(e) can apply even if no ineligible property was transferred on a rollover basis, as s. 88(1)(e)(ii) only requires that...

Paragraph 88(1)(e.1)

Administrative Policy

9 January 2004 External T.I. 2003-0049195 F - Winding Up or a Contractor Subco

Opco, which is wholly-owned by Holdco, and has been using the percentage-of-completion method in computing its income from its construction...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Timing | exclusion of contract holdbacks and unapproved invoices from construction contractor’s income is unaffected on s. 88(1) wind-up and flows through to parent | 174 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(m) | deferred revenue of construction contractor would not be triggered on its s. 88(1) wind-up and parent would be put to claiming any available new s. 20(1)(m) reserve | 161 |

Paragraph 88(1)(e.2)

Administrative Policy

S3-F3-C1 - Replacement Property

Preservation of ss. 13 and 44 replacement property rollover

1.50 Similarly, paragraph 88(1)(e.2) prevents the loss of a section 13 or section 44...

9 January 2002 External T.I. 2001-0075825 F - CII-LIQUIDATION

A subsidiary sells all of its depreciable property to a third party and, during the same taxation year, commences to be wound up into its parent,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(t) | application of s. 12(1)(t) to parent in the year following the s. 88(1) wind-up of sub | 161 |

30 November 1995 Ruling 9611983 - APPLICABILITY OF WITHOLDING EXEMPTION UPON WINDING UP

Favourable ruling that the exemption in s. 212(1)(b)(vii) continued following a wind-up of the debtor corporation under s. 88(1).

Paragraph 88(1)(e.3)

Administrative Policy

2018 Ruling 2017-0711071R3 - Use of subsidiary losses & ITCs after wind-up

A foreign-owned Canadian-resident corporation (“Taxpayer”) used a subsidiary LP to acquire the sole business of a “Lossco” that was in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1.1) - Paragraph 88(1.1)(b) | streamed losses of empty-shell Lossco flowed through on its dissolution as Lossco LP business had been acquired years earlier through sub LP | 352 |

1 June 2004 Internal T.I. 2004-0078161I7 F - ITCs - Winding-up

The Directorate indicated that where a subsidiary was wound up into its parent, the parent could not claim unused investment tax credits ("ITCs")...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) | to be “wound up” there must generally be evidence that the sub will soon be dissolved | 203 |

Subsection 88(1.1) - Non-capital losses, etc., of subsidiary

See Also

S.T.B. Holdings Ltd. v. The Queen, 2011 DTC 1118 [at at 650], 2011 TCC 144, aff'd 2002 DTC 7450, 2002 FCA 386

The taxpayer purchased the shares of an unrelated corporation ("Newport") with substantial non-capital losses and wound up Newport into itself,...

Administrative Policy

2021 Ruling 2020-0869161R3 - Loss Carryforwards and 88(1.1)

Background

Lossco and its parent (Parentco, also a taxable Canadian corporation) filed for insolvency protection under the CCAA. After receiving...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(b) | pre-wind-up PUC reduction to no less than the subsidiary's asset cost amount | 184 |

2017 Ruling 2017-0711911R3 - loss consolidation ruling

A parent company (Aco), whose only source of taxable income was foreign accrual property income from a non-resident subsidiary but which had...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(1) - Paragraph 111(1)(a) | transfer of losses from parent with losses after FAPI to successive new losscos, which then are wound-up into profitco | 402 |

17 February 2016 External T.I. 2015-0618211E5 - Subsections 88(1.1) and 88(1.2)

Can losses be used by a parent corporation in the year commencing after the commencement of the winding-up of its subsidiary, where the legal...

S4-F7-C1 - Amalgamations of Canadian Corporations

1.54 Where a predecessor corporation's losses have been carried forward to the new corporation under the provisions of subsection 87(2.1), it is...

2014 Ruling 2013-0511991R3 - Loss consolidation

Lossco, which is a specified financial institution with non-capital losses, is a subsidiary of non-resident parent, and serves as the holding...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(1) - Paragraph 111(1)(a) | losses transferred to Newco which is wound-up into profitco, s. 88(1.1) loss transfer not effective until articles of dissolution, provincial GAAR ruling, cashless un-wind | 418 |

2013 Ruling 2013-0496351R3 - Loss Consolidation

{kind=link}

Opco, which has non-capital losses, wishes to transfer its non-capital losses to Profitco, a sister. Accordingly, Opco will effectively transfer...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(1) - Paragraph 111(1)(a) | value of losses transferred to new Lossco reflected in Lossco sale price | 553 |

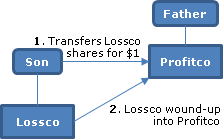

5 October 2012 APFF Roundtable, 2012-0454061C6 F - Transfer of a Lossco to a related corporation

Example 1

{kind=link}

Son claims an ABIL under s. 50(1) with respect to his share investment in a wholly-owned corporation (Lossco), which had ceased active...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Shares | non-capital losses of corporation taken into account in valuing its shares | 162 |

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(1) - Paragraph 111(1)(a) | related but not affiliated transfer of Lossco shares to father's or brother's company | 267 |

| Tax Topics - Income Tax Act - Section 50 - Subsection 50(1) | lossco with no assets or liabilities cannot be insolvent | 417 |

30 May 2012 External T.I. 2012-0447961E5 - Winding-up-Carryover of Non-Capital Losses

Parentco winds up its wholly-owned subsidiary (Subco) on May 1, 2012, with the certificate of dissolution of Subco being issued on October 31,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1.1) - Paragraph 88(1.1)(f) | s. 88(1)(f) election to use loss incurred by sub in its year beginning after the start of its winding-up in parent’s taxation year ending immediately after such start | 203 |

19 March 2001 External T.I. 2001-0067105 - Meaning of winding-up

The policy of the CCRA that a corporation is considered to have been wound up when there is substantial evidence that it will be dissolved within...

11 October 1996 APFF Roundtable, 7M12910 - APFF ROUND TABLE

Where the acquisition of control of a corporation that holds land as an adventure in the nature of trade results in the realization of a...

22 November 1996 External T.I. 9628845 - REVIVAL OF A DISSOLVED CORPORATION-IMPACT ON LOSSES

Because a revival under s. 241(5) of the Business Corporations Act (Ontario) has retroactive effect, the non-capital losses will be restored upon...

31 October 1994 External T.I. 9420595 - NON-CAPITAL LOSSES

Where two wholly-owned subsidiaries are amalgamated with each other and then wound-up into the parent, the non-capital losses of the subsidiaries...

Halifax Round Table, February 1994, Q. 2

If the parent commences to carry on the business of the subsidiary, and the subsidiary ceases to carry on that business, prior to the time that...

92 C.R. - Q.18

RC implicitly assumed that s. 88(1.1) was available where the subsidiary had abandoned its business, and used all remaining assets to pay down...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 29 | |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 29 |

30 July 1992 T.I. 921653 (March 1993 Access Letter, p. 72, ¶C82-110)

The application of s. 80 to the parent in its second taxation year ending after the commencement of the winding-up will reduce the non-capital...

6 February 1992 T.I. (Tax Window, No. 16, p. 20, ¶1736)

The fact that a corporation has been dissolved by the order of the Director under s. 241(4) of the Business Corporations Act (Ontario) does not...

23 September 1991 Memorandum (Tax Window, No. 9, p. 5, ¶1469)

The phrase "that business" in s. 88(1.1)(e) refers to the particular business of the subsidiary in which the loss was incurred and not other...

IT-302R3 "Losses of a Corporation - The Effect on Their Deductibility of Changes in Control, Amalgamation and Winding-up" 1 January 1995.

Commencement of winding-up

29. ...[G]enerally, the commencement of winding-up is evidenced by a resolution of shareholders authorizing or...

Paragraph 88(1.1)(b)

Administrative Policy

2018 Ruling 2017-0711071R3 - Use of subsidiary losses & ITCs after wind-up

Acquisition of Lossco business

Subsequently to a CCAA filing by Lossco and members of its group, Taxpayer (a wholly-owned subsidiary of a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(e.3) | purchaser could acquire Lossco’s business through a sub LP and then acquire Lossco, accessing s. 88(1)(e.3) | 152 |

Paragraph 88(1.1)(e)

See Also

Gaz Métropolitain Inc. v. R., [1999] 2 CTC 2116, 98 DTC 1751, 1998 CanLII 227

The taxpayer (GMI), which carried on a business of selling natural gas to residential, commercial and industrial customers, had a minority...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(5) - Paragraph 111(5)(a) | activity of converting cars to natural gas was ancillary to the business’ primary purpose of natural gas sales | 163 |

Administrative Policy

7 October 2011 APFF Roundtable, 2010-0371941C6 F - Application de l'article 80 - fusion/liquidation

A subsidiary that sustained losses and then was subject to an acquisition of control, is then wound up into the parent corporation following which...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) - Relevant loss balance | NCL of acquired subsidiary preserved for debt forgiveness purposes on amalgamation but lost (if business ceased) on wind-up | 138 |

16 August 2011 Internal T.I. 2011-0401721I7 F - Loss Utilization

Before finding that the non-capital losses of an acquired corporation (whose only sources of income were inter-affiliate loan and subsidiary...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(5) - Paragraph 111(5)(a) | holding company whose only sources of income were inter-affiliate loan and subsidiary shares had losses from property rather than business | 117 |

Paragraph 88(1.1)(f)

Administrative Policy

30 May 2012 External T.I. 2012-0447961E5 - Winding-up-Carryover of Non-Capital Losses

Parentco winds up its wholly-owned subsidiary (Subco) on May 1, 2012, with the certificate of dissolution of Subco being issued on March 31, 2013....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1.1) | parent can use loss deemed to be incurred in the sub’s 2012 year (ending after the commencement of the wind-up) in parent’s 2013 year, where dissolution is late in 2013 | 586 |

17 February 1993 Income Tax Severed Letter 9226895 F - Pertes-liquidation

A subsidiary realized losses in its two taxation years preceding its winding-up. Its winding-up commenced in a taxation year of its parent...

Subsection 88(1.5) - Parent continuation of subsidiary

Articles

Gregory M. Johnson, Wesley R. Novotny, "An Update on Flow-through Shares in the Energy Sector", 2016 Conference Report (Canadian Tax Foundation),12:1-39

Possibility that s. 88(1.5) does not apply following the winding-up distribution and before the dissolution (p. 12:19)

...[N]o subsequent issues...

Mike J. Hegedus, Andrew Bateman, "A Closer Look at Subsection 88(1.5) of the Income Tax Act", Resource Sector Taxation, Vol. VIII, No. 3, 2011, p. 591.

Subsection 88(1.7) - Interpretation

Administrative Policy

21 November 2011 External T.I. 2011-0418971E5 - subsection 88(1.7)

Acquisitionco acquires all the shares of Pubco, which are widely held, at the time that a wholly-owned subsidiary of Pubco (Subco) holds the Asset...

Subsection 88(2) - Winding-up of Canadian corporation

See Also

Re Martin and F.P. Bourgault Industries Air Seeder Division Ltd. (1987), 45 DLR (4th) 296 (Sask. C.A.)

The appellant, which manufactured air seeders in one plant, and cultivators in its other plant, transferred its cultivator division, which...

85956 Holdings Ltd. v. Fayerman Bros. Ltd., [1985] 2 WWR 647 (Sask QB)

A sale by a wholesale-retail merchant of all its inventories would destroy its business, and accordingly would constitute "a sale, lease or...

Administrative Policy

26 November 2014 External T.I. 2014-0551641E5 F - Winding-up and subsection 42(1)

A corporation was to be liquidated as described in s. 88(2) and to be dissolved upon receipt of provincial and federal notices of assessment for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 42 | corporation permitted to claim litigation loss following effective time of winding-up | 104 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) | effective time of winding-up not delayed by potential litigation liability | 104 |

10 December 2013 External T.I. 2013-0480771E5 F - Winding-Up of a Corporation

The correspondent queried the accuracy of the statement in the T2 Guide that on a s. 88(2) winding-up, s. 88(2)(a)(iv) indicates that the taxation...

2013 Ruling 2012-0443081R3 - Distribution of pre-72 Capital Surplus on Hand

{kind=link}

Current situation

ACo, which is a Canadian-controlled private corporation (with an RDTOH balance) owned by cousins (an unrelated group), owns...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) | circularity issue | 673 |

| Tax Topics - Income Tax Act - Section 54 - Personal-Use Property | 118 |

Articles

O'Connor, "Revisiting Pre-1972 Capital Surplus on Hand (the More Things Change, the More They Stay the Same)", Personal Tax Planning, 1996 Canadian Tax Journal, Vol. 44, No. 2, p. 501.

Paragraph 88(2)(a)

Articles

Derek T. Dalsin, "ECP-Related CDA Dividend “In the Course of a Winding Up” Pre-2017", Canadian Tax Highlights, Vol. 27, No. 8, August 2019, p. 1

No increase to CDA balance from eligible capital amount until year end (p. 1)

[I]n order for a capital dividend account (CDA) to arise out of a...

Paragraph 88(2)(b)

Administrative Policy

2020 Ruling 2020-0840631R3 F - Purpose Test in Subsection 55(2)

Following the death of the father, his preferred shares of a CCPC (“Opco”), that held only cash as a result of having sold all its marketable...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(b) | no application of s. 55(2) because ss. 88(2)(b) and 84(2) dividends did not significantly reduce capital gains | 321 |

Subparagraph 88(2)(b)(i)

Administrative Policy

6 October 2017 APFF Roundtable Q. 4, 2017-0709021C6 F - CDA and Winding-up of a corporation

Where, at the moment of a winding-up described in s. 88(2), the corporation holds portfolio investments or other assets whose fair market value...

Subparagraph 88(2)(b)(ii)

Administrative Policy

2021 Ruling 2020-0863171R3 - Gross basis split-up Butterfly

CRA ruled on a butterfly split-up of a rental property company (which was considered to carry on an active business because it had more than five...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | CRA rules on gross asset butterfly with preliminary safe income dividend to increase ACB to exceed pre-1972 CSOH | 614 |

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) - Paragraph 186(1)(b) | request to TSO for short taxation year to avoid dividend circularity on split-up butterfly | 233 |

Subsection 88(2.1)

Administrative Policy

15 October 1991 T.I. (Tax Window, No. 11, p. 8, ¶1525)

In determining the actual cost to a corporation of land owned by it on December 31, 1971 and disposed of after 1978, damages received by it in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Adjusted Cost Base | 46 |

Subsection 88(3) - Liquidation and dissolution of foreign affiliate

See Also

Dauphin Plains Credit Union Ltd. v. Xyloid Industries Ltd., 80 DTC 6123, [1980] CTC 247, [1980] 1 S.C.R. 1182

The appellant was a secured debentureholder who, following default by the debtor (“Xyloid”), obtained a court order for the appointment of a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 153 - Subsection 153(1) - Paragraph 153(1)(a) | receiver-manager included | 25 |

| Tax Topics - Income Tax Act - Section 159 - Subsection 159(2) | 36 | |

| Tax Topics - Income Tax Act - Section 227 - Subsection 227(5) | 41 | |

| Tax Topics - Statutory Interpretation - Interpretation Act - Section 17 | 38 |

Administrative Policy

16 May 2018 IFA Roundtable Q. 5, 2018-0745501C6 - Meaning of “merged or combined” in 40(3.5)(c)(i)

Canco sold all the shares of FA to Canco’s wholly-owned subsidiary (Subco) and realized a capital loss that was suspended under s. 40(3.4). In...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(3.5) - Paragraph 40(3.5)(c) - Subparagraph 40(3.5)(c)(i) | suspended loss on the sale of CFA to Subco was not de-suspended on s. 88(3) wind-up of CFA | 208 |

17 July 2014 External T.I. 2014-0536331E5 - Foreign affiliate liquidation and dissolution

Can property that is deemed to have been disposed of by paragraph 88(3)(b) be "excluded property" of the affiliate at the relevant time? In...

14 August 2008 External T.I. 2004-0104691E5 - Conversion of a LLC to a LP

where a Delaware LLC governed by the Delaware Limited Liability Company Act is converted into a limited partnership pursuant to s. 17-217 of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Corporation | Del. LP a partnership notwithstanding separate legal personality | 168 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | LLC conversion to Delaware LP | 54 |

26 October 2007 External T.I. 2005-0137641E5 - Dissolution of Foreign Affiliate

A loan is made by a controlled foreign affiliate of a taxpayer to the taxpayer immediately before the dissolution of the affiliate. Does the loan...

IT-126R2, "Meaning of 'Winding-Up' ", March 20, 1995

8. The phrase "on the winding-up", as used in subsection 88(1) for a corporation or in subsection 84(2) for a corporation's business, means that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | 235 | |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) | 148 |

Articles

Patrick Marley, "Foreign Affiliate Mergers and Liquidations - Navigating Proposed Changes", Canadian Current Tax, Vol. 16, No. 12, September 2006, p. 125.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(d.1) | 0 |

Dale S. Meister, "Foreign Affiliate Update", Canadian Petroleum Tax Journal, Vol. 19, No. 1

Includes summaries of comfort letters and CRA 2006 IFA pronouncements.

Paragraph 88(3)(d)

Administrative Policy

3 February 2016 External T.I. 2014-0548111E5 - U.S. tax paid in respect of an LLC's income