Subsection 87(1) - Amalgamations

Cases

Envision Credit Union v. Canada, 2013 DTC 5144 [at at 6275], 2013 SCC 48, [2013] 3 S.C.R. 191

The taxpayer ("Envision") was formed on the amalgamation under the Credit Union Incorporation Act (B.C.) (the "CUIA") of two credit unions. S....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Illegality | lawful interpretation preferred | 282 |

| Tax Topics - General Concepts - Separate Existence | shareholders do not own the corporation's assets | 135 |

Guaranty Properties Ltd. v. The Queen, 87 DTC 5124, [1987] 1 CTC 242 (FCTD), rev'd 90 DTC 6363 (FCA)

A corporation ("Dixie") amalgamated in 1978 to form Forest Glenn, and Forest Glenn amalgamated in 1980 to form Guaranty Properties. A notice of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(8) | curative provisions cannot correct a fundamental substantive error | 58 |

Allendale Mutual Insurance Co. v. The Queen, 73 DTC 5382, [1973] CTC 494 (FCTD)

Three insurance corporations were merged pursuant to a special Rhode Island statute, which provided that the three predecessors were "made and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Shareholder | 23 |

See Also

University Health Network v. The Queen, [2000] PTR 4181 (Ont S Ct J)

The amalgamation of two incorporated hospitals did not cause them to lose their tax-exempt status under the Retail Sales Tax Act notwithstanding...

National Bank of Canada v. B.C. (1990), 48 BCLR (2d) 485 (BCSC)

The Bank Act was found to contemplate that the amalgamation of two banks gave rise to the emergence or creation of a new entity in light inter...

Loeb Inc. v. Cooper, Cooper and Cooper (1991), 5 OR (3d) 259 (Ont. Ct. G.D.)

The amalgamation under the provisions of the Canada Business Corporations Act of a tenant did not result in an assignment of the lease. Henry J....

The Great Western Railway Co. v. Commissioners of Inland Revenue, [1894] 1 Q.B. 507 (C.A.)

The Great Western Railway Act, 1892 (U.K.) provided that the undertakings of two other railway companies should be amalgamated with and form part...

Administrative Policy

25 November 2021 CTF Roundtable Q. 1, 2021-0911841C6 - Indemnities and subsection 87(4)

There has been a triangular amalgamation under which a subsidiary of Parent amalgamated with Target and the Target shareholders received shares of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(4) | payment of damages, for breach of reps, by the parent following a triangular amalgamation would not preclude satisfaction of s. 87(4) | 242 |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(3) | when escrowed shares are cancelled as compensation for breach of representations of the shareholders, the payment for s. 84(3) purpose is those shares’ FMV | 136 |

2017 Ruling 2016-0643931R3 - PUC reinstatement on emigration

A non-resident partnership (Partnership 1) and its non-resident co-investors wished to acquire a Canadian public-company target (Target), whose...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5905 - Subsection 5905(5.4) | bump of non-resident subsidiaries reduced by applicable surplus balances | 635 |

| Tax Topics - Income Tax Act - Section 219.1 - Subsection 219.1(4) | post-acquisition sandwich structure exited through using the s. 88(1)(d) bump in combination with a continuance outside Canada | 372 |

2015 Ruling 2015-0564981R3 - "cross-statute" amalgamation

As part of a Plan of Arrangement for the spin-off by an agricultural cooperative corporation (“ACC”) of one of its two businesses under a Plan...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 135.1 - Subsection 135.1(1) - Allowable Disposition | deemeed withdrawal from predecessor of Amalco under Plan of Arrangement | 618 |

S4-F7-C1 - Amalgamations of Canadian Corporations

1.4 In Envision Credit Union v. R., 2013 SCC 48, 2013 DTC 5144 (SCC), the Supreme Court of Canada held that it was not possible for the...

2012 Ruling 2010-0355941R3 - reverse subsidiary merger - 87(1) & 87(11)

Under a BC plan of arrangement, a BC corporation ("SubcoTarget") is merged with its wholly-owned BC subsidiary ("Target") to form "Amalco" with...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(11) | survivor style amalgamation on Code reverse triangular merger | 209 |

2006 Ruling 2006-0178571R3 - Purchase of Target and Bump

{kind=link}

Parent-group losses

/FIRPTA. Parent (a.k.a, Target and, following the merger below, Mergeco) is a CBCA public company. It and various direct...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(d) | 64 |

3 December 2003 External T.I. 2003-0046015 - Amalgamation and Sub. 97(2) Election

Where a predecessor corporation made a transfer to a partnership described in s. 97(2), the amalgamated corporation can file the s. 97(2) election...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 97 - Subsection 97(2) | election filed by Amalco | 28 |

10 April 2003 External T.I. 2002-0169775 - Foreign Merger

Where a Japanese parent merges with his Japanese subsidiary which, in turn, holds shares of a Canadian company, the Japanese subsidiary will not...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | 95 |

2 February 2000 External T.I. 2000-0003385 - NON-QUALIFYING AMALGAMATIONS

The tax accounts of predecessor corporations do not flow through to the merged corporation in a non-qualifying amalgamation.

30 November 1996 Ruling 9724053 - AMALGAMATION, DISSENT

An amalgamation under which a shareholder of one of the predecessors would be entitled to receive redeemable preferred shares which would be...

12 August 1994 External T.I. 9415495 - AMALGAMATION/WIND-UP

Although, on the amalgamation of a wholly-owned subsidiary with its parent where the subsidiary also owns shares of the parent, s. 69(1)(b) would...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(3) | 42 | |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) | 68 |

92 C.R. - Q.26

Where an amalgamation does not qualify under s. 87 and, under the governing corporate law, the amalgamated corporation is considered to be a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | 66 |

91 C.R. - Q.22

Where a shareholder of a predecessor corporation, who is entitled to only a fraction of a share of the amalgamated corporation, or who dissents to...

89 C.P.T.J. - Q. 14

Because there is no provision like s. 87(1.2) deeming an amalgamated corporation to be a continuation of each predecessor, where a corporation has...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 66.3 - Subsection 66.3(1) | 41 |

89 C.P.T.J. - Q15

Because Deltona indicates that an amalgamated corporation is incorporated on the amalgamation, a corporation that currently is disqualified as a...

IT-474R "Amalgamations of Canadian Corporations" under "Rules Respecting Shareholders, Option Holders and Creditors" under "Non-Resident Shareholders"

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) | 46 |

Articles

Henry Chong, "Surviving North of the Border: Structuring a Statutory Merger in Canada to Qualify as a U.S. Tax-Free Reorganization", Tax Management International Journal, 2012, p. 611

Respecting 2006-0178571R3, he states that the CRA position

appears to be based on the view that the reference in s. 87(2)(a) to "new corporation"...

Stephen S. Ruby, "Recent Transactions of Interest", 2007 Conference Report (Toronto: Canadian Tax Foundation, 2008), 3:1-41, at 3:13-17

Discussion of the Chesapeake Gold Corporation acquisition of American Gold Capital entailing a "survivor style" merger.

Firoz Ahmad, "Amalgamation Versus Winding-Up Revisited", Canadian Current Tax, Vol. 15, No. 4, January 2005, p. 33.

Richards, "Amalgamations", The Taxation of Corporate Reorganizations, 1996 Canadian Tax Journal, Vol. 44, No. 1, p. 241.

Vesely, "Takeover Bids: Selected Tax, Corporate and Securities Law Considerations", 1991 Conference Report, c. 11.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1.1) | 0 |

Schwartz, "Statutory Amalgamations, Arrangements and Continuations: Tax and Corporate Law Considerations", 1991 Conference Report, c. 9.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(9) | 0 |

Williamson, "Checklists: Corporate Reorganizations, Amalgamations (Section 87), and Wind-ups (Subsection 88(1))", 1987 Conference Report, c. 29.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) | 0 |

Paragraph 87(1)(a)

Administrative Policy

14 April 2021 External T.I. 2018-0785921E5 F - alinéa 87(1)a)

2017-0696821E5 F described two individuals, Mr. A and Mr. B, who wholly-owned two corporations of equal value (A Inc. and B Inc.) and who, on the...

15 September 2017 External T.I. 2017-0696821E5 F - Amalgamation

Two individuals, Mr. A and Mr. B wholly-own two corporations of equal value (A Inc. and B Inc.), which amalgamate. On the amalgamation, the two...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(4) | receipt of cash on amalgamation precluded rollover | 206 |

Subsection 87(1.1) - Shares deemed to have been received by virtue of merger

Administrative Policy

S4-F7-C1 - Amalgamations of Canadian Corporations

1.9 … Subsection 87(1.1) deems the shares that are not cancelled on a short-form vertical or horizontal amalgamation to be shares of the new...

Subsection 87(1.2) - New corporation continuation of a predecessor

Administrative Policy

S4-F7-C1 - Amalgamations of Canadian Corporations

1.56 In the case of an amalgamation to which subsection 87(1.2) does not apply, any undeducted balance in a predecessor corporation's resource...

Subsection 87(2) - Rules applicable

Paragraph 87(2)(a) - Taxation year

Cases

CGU Holdings Canada Ltd. v. Canada, 2009 DTC 5685, 2009 FCA 20

Noël, J.A. rejected a submission of the taxpayer that s. 87(2)(a) deemed an amalgamation of three corporations (one of which was an NRO) to be a...

The Queen v. Pan Ocean Oil Ltd., 94 DTC 6412, [1994] 2 CTC 143 (FCA)

The taxpayer was the result of a 1974 amalgamation of two Alberta corporations, one of which was a second successor corporation for purposes of s....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Application Rules - Subsection 29(29) | 145 |

The Queen v. Guaranty Properties Ltd., 90 DTC 6363, [1990] 2 CTC 94 (FCA)

Following the amalgamation of the two predecessor corporations of the taxpayer under the laws of Ontario, the Minister issued a reassessment and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(1) | amalgamation did not extinguish predecessors for assessment purposes | 50 |

See Also

CGU Holdings Canada Ltd. v. The Queen, 2008 DTC 3347, 2008 TCC 167, aff'd 2009 FCA 20

The taxpayer was formed on the amalgamation of three predecessors, only one of which was a non-resident-owned investment corporation ("NRO")....

Administrative Policy

9 October 2025 APFF Roundtable Q. 3, 2025-1071581C6 F - Fusion et actions admissibles de petite entreprise

On January 1, 202X, a resident individual (Mr. A) sold all the shares of Targetco for cash consideration to a resident arm’s-length purchase...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(9) | acquisition of CCPC for SBC purposes occurs at its actual time irrespective of s. 256(9) | 152 |

2021 Ruling 2019-0821121R3 - Multi-wing split-up gross asset butterfly

The stated purpose for the amalgamation of a corporation (DC) shortly after a butterfly distribution of its assets was to create a short taxation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | pre-butterfly amalgamation to create business property and post-butterfly amalgamation to minimize Pt. IV tax/ gross FMV multi-wing butterfly | 995 |

| Tax Topics - Income Tax Act - Section 96 | representations re properties being held in co-ownership rather than partnership | 220 |

S4-F7-C1 - Amalgamations of Canadian Corporations

New corporation

1.13 Under the corporate law in most jurisdictions, the corporate entity formed as a result of an amalgamation is a continuation...

15 April 2014 External T.I. 2014-0527231E5 F - Acquisition of control and amalgamation

A plan of arrangement provides for the following transactions to occur on 18 January 20X1 and in the indicated order but without a particular hour...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 249 - Subsection 249(4) | key corporate transactions moments before acquisition of control and amalgamation result in such transactions falling in a stub year | 261 |

26 March 2013 External T.I. 2014-0523251E5 F - Acquisition of control and amalgamation

Following a sale of assets of a corporation and a rollover of its shares on 18 January 20X1, an acquisition of control of the corporation occurs...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 249 - Subsection 249(4) | double taxation year ends where transactions occur on the closing date before acquisition and amalgamation | 366 |

17 February 2011 External T.I. 2010-0388081E5 - Clarification STEP Roundtable Q3 - Deemed Year End

On the amalgamation of public corporation ("Pubco") and a private corporation ("Holdco") to form Amalco, the three shareholders of Holdco acquire...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 249 - Subsection 249(4) | 2010 STEP Roundtable Q. 3 clarification - no double acquisition | 74 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(7) - Paragraph 256(7)(b) | double year ends where acquisition of control under s. 256(7)(b)(ii) | 162 |

8 October 2010 Roundtable, 2010-0373201C6 F - Change of Control and Amalgamation

Is the CRA's position, that a predecessor corporation whose control was acquired on the same day will have only one year end, solely limited to...

23 November 2004 External T.I. 2004-0094101E5 F - IT-474R Administrative Relief

The taxpayer referenced the statement in IT-474R, para. 10 that “[w]here the provisions of paragraph 87(2)(a) produce unintended consequences...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(24) | amalgamated corporation can make s. 20(24) election | 136 |

28 April 2004 Internal T.I. 2004-0067561I7 F - Impôt de la partie I.3

In connection with the taxpayer’s reference to the statement in IT-474, para. 10 that “[w]here the provisions of paragraph 87(2)(a) produce...

1993 Internal T.I. 7-920752

The Rulings Directorate no longer is providing relief where taxpayers suffer unpredictable and unfavourable consequences pursuant to s. 87(2)(a).

3 July 1991 T.I. (Tax Window, No. 5, p. 13, ¶1334)

RC's assessing policies with respect to amalgamations are under review because of the decision in the Guaranty Properties case.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(3) | 13 |

12 December 1989 T.I. (May 1990 Access Letter, ¶1221)

Although an amalgamated corporation is a new corporation for the purposes of computing income and tax otherwise payable, s. 87(2)(a) is not...

Articles

MacDonald, "Amalgamations Following Guaranty Properties Limited", 1991 Canadian Tax Journal, p. 1399.

Paragraph 87(2)(b) - Inventory

Administrative Policy

S4-F7-C1 - Amalgamations of Canadian Corporations

1.27 …The new corporation will generally be expected to follow the inventory valuation method adopted by its predecessor corporations for the...

5 March 1992 T.I. (Tax Window, No. 17, p. 21, ¶1785)

Where two or more corporations amalgamate, the cost amount of the inventory of a predecessor corporation is its value determined for the purpose...

27 February 1991 Memorandum (Tax Window, Prelim. No. 3, p. 24, ¶1113)

An amalgamated corporation must use the same inventory valuation method as its predecessors. Where an amalgamated corporation has two predecessors...

Paragraph 87(2)(c) - Method adopted for computing income

Administrative Policy

S4-F7-C1 - Amalgamations of Canadian Corporations

1.98 In the case of an amalgamation or merger, there may not technically be a disposition of property from a predecessor corporation to the new...

Paragraph 87(2)(d) - Depreciable property

Administrative Policy

S4-F7-C1 - Amalgamations of Canadian Corporations

1.30 …[T]he capital cost to the new corporation of depreciable property of a prescribed class acquired by it on the amalgamation will equal the...

Paragraph 87(2)(e.1) - Partnership interest

Administrative Policy

S4-F7-C1 - Amalgamations of Canadian Corporations

1.42 Where the new corporation is not related to the predecessor corporation, subsection 100(2.1)… requires the predecessor corporation to...

Paragraph 87(2)(f)

Administrative Policy

14 June 2002 External T.I. 2001-0103755 F - Cumulative Eligible Capital on Amalgamation

In Situation 1, Portfolioco and its wholly-owned subsidiary, Subco, which were both incorporated on February 1, 1993, amalgamated on July 1, 2001...

Paragraph 87(2)(g)

Administrative Policy

24 October 2017 Internal T.I. 2017-0719531I7 - Section 22 election and carrying on a business

Immediately after its formation, Amalco dropped the business of a predecessor down to a partnership under s. 97(2) – except that it used the s....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 22 - Subsection 22(1) | s. 22 election was available to an Amalco despite its receivables not being deemed to have been includible in its income | 372 |

Paragraph 87(2)(g.5)

Administrative Policy

Frequently asked questions - Canada emergency wage subsidy (CEWS) CRA Webpage 24 September 2021

6-4. Can a corporation formed on the amalgamation of two or more predecessor corporations, or where one corporation is wound up into another,...

Paragraph 87(2)(g.6)

Administrative Policy

12 April 2021 External T.I. 2020-0863701E5 - CEWS - Asset Sale Followed by Amalgamation

In January 2018, ParentCo acquired all the shares of TargetCo which, until the spin-off described below carried on a single business (the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125.7 - Subsection 125.7(4.1) | s. 87(2)(g.6) and s. 125.7(4.1) continuity rules can be read together | 302 |

Paragraph 87(2)(j.6)

Administrative Policy

11 December 2024 External T.I. 2024-1039101E5 F - Vertical amalgamation & former paragraph 84.1(2)(e)

S. 84.1(2.3)(a)(i), as part of the former (private-member bill) intergenerational business transfer rules, provided that if, otherwise than by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2) - Paragraph 84.1(2)(e) | s. 87(2)(j.6) continuity rule does not remediate the adverse consequences under the old intergenerational transfer rules of vertically amalgamating the subject corp | 155 |

Paragraph 87(2)(l.3)

Administrative Policy

S3-F3-C1 - Replacement Property

Preservation of ss. 13 and 44 replacement property rollover

1.49 Paragraph 87(2)(l.3) prevents the deferral rules in sections 13 and 44 from being...

Paragraph 87(2)(o) - Expiration of options previously granted

Administrative Policy

S4-F7-C1 - Amalgamations of Canadian Corporations

1.46 Where a corporation has granted an option (other than an option to acquire its shares, bonds or debentures), subsection 49(1) deems the...

Paragraph 87(2)(q) - Registered plans

Administrative Policy

S4-F7-C1 - Amalgamations of Canadian Corporations

1.67 Pursuant to paragraph 87(2)(q), the new corporation is deemed to be the same corporation as, and a continuation of, each predecessor...

Paragraph 87(2)(s)

Subparagraph 87(2)(s)(ii)

Administrative Policy

25 February 2019 External T.I. 2019-0793911E5 F - Triangular amalgamation and section 135.1

Respecting a query on the application of ss. 135.1(2) and (7) to a triangular amalgamation referred to in s. 87(9), CRA stated:

[T]he reference to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 135.1 - Subsection 135.1(2) | potential s. 131.1(2) income inclusion on triangular amalgamation | 118 |

Paragraph 87(2)(z.1)

Administrative Policy

18 September 2025 CLHIA Roundtable Q. 3, 2025-1067941C6 - Capital Dividend Account Anti-Avoidance Rule in Subsection 83(2.1)

Opco A used the proceeds of a recently-purchased policy on the life of it principal shareholder (now deceased) to repay a $100,000 loan from an...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 83 - Subsection 83(2.3) | s. 83(2.1) (but for subsequent amalgamation) would apply where corporate life insurance proceeds (giving rise to a CDA addition) were used for a loan repayment rather than distribution | 289 |

11 October 2019 APFF Roundtable Q. 6, 2019-0812651C6 F - CDA and wind-up of a subsidiary

Holdco, which has a calendar taxation year-end, commences the winding-up of its wholly-owned subsidiary (Opco – which has a June 30 taxation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) | IT-126R2 applied re timing of addition of the wound-up subsidiary’s CDA | 117 |

S3-F2-C1 - Capital Dividends

Calculation of Amalco's CDA

1.80 ...Corporation A:

- realized a capital gain of $100,000 in its 2005 tax year, of which the non-taxable portion,...

9 October 2015 APFF Roundtable Q. 6, 2015-0595551C6 F - Capital Dividend Account

If Holdco (a CCPC) has realized $1M in allowable capital losses on its public company portfolio, its subsidiary (Opco) has realized a $1M taxable...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Capital Dividend Account | capital loss does not eliminate positive CDA contribution of capital dividend received | 145 |

29 June 2009 External T.I. 2008-0296371E5 F - Capital dividends

An estate owns all the shares of Corporation A, which has a capital dividend account (CDA) and refundable dividend tax on hand account (RDTOH) but...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 129 - Subsection 129(1.2) | s. 87(2)(aa) would apply to eliminate RDTOH of predecessor given the absence of an s. 83(2.4) equivalent to exempt the predecessor’s notional dividend | 203 |

| Tax Topics - Income Tax Act - Section 83 - Subsection 83(2.1) | s. 83(2.1) would apply to acquisition and amalgamation with shell corp. with CDA unless s. 83(2.4) exceptions applied | 255 |

29 May 2007 Internal T.I. 2007-0223381I7 F - Capital Dividend Account

A subsidiary (Bco) that was wound-up under s. 88(1) into Aco had a positive balance in para. (c.2) of the capital dividend account definition due...

Paragraph 87(2)(ii) - Public corporation

Administrative Policy

2015 Ruling 2015-0577141R3 - Election to cease to be a public corporation

Under a Plan of Arrangement, the Canadian public target ("Pubco") was to be amalgamated with Bidco. The applicable rules did not permit the shares...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Public Corporation | closely-held Amalco can elect following the delisting of shares of a public predecessor | 276 |

Articles

Joint Committee, "Definition of 'Public Corporation'", 4 March 2019 Joint Committee Submission

- Even if a heretofore public corporation has made a good election under (c)(i) of the s. 89(1) definition of public corporation to cease to be a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Public Corporation - Paragraph (a) | shares of Target are considered to be listed up until the completion of the delisting process | 269 |

Subsection 87(2.1) - Non-capital losses, etc., of predecessor corporations

Administrative Policy

S4-F7-C1 - Amalgamations of Canadian Corporations

Amalco can use losses and RIFE of predecessors subject to loss restriction rules – but no carryback except under s. 87(2.11)

1.47 Subject to the...

10 October 2024 APFF Roundtable Q. 14, 2024-1028951C6 - Utilisation des pertes autres qu’en capital après acquisition de contrôle et fusion

Holdco, a CCPC, had accumulated non-capital losses (NCLs) arising from the management services it had rendered over the years (i.e., the services...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(5) - Paragraph 111(5)(a) | losses from a business of Holdco providing admin services to Opco likely would disappear following an acquisition of control and their amalgamation | 279 |

2020 Ruling 2019-0819871R3 - Loss Consolidation Involving Canadian Branch

Background

- Canco1, which carries on the Profitco Business in Canada is wholly-owned by Foreignco2 which, in turn, is wholly-owned by Foreignco1,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | US corp is same corporation after its continuance to Canada | 164 |

20 June 2016 External T.I. 2016-0651951E5 F - Amalgamation - non-capital loss of new corporation

The loss, sustained in the year after the amalgamation, of the corporation formed by the amalgamation of two sister corporations cannot be carried...

S4-F7-C1 - Amalgamations of Canadian Corporations

1.54 Where...where a subsidiary's losses have been carried forward to the parent under the provisions of subsections 88(1.1), (1.2) or (1.3),...

26 October 2006 External T.I. 2006-0170341E5 F - Subsections 87(2.1) and 87(2.11)

Canco, and it wholly-owned subsidiary, Subco1 amalgamated on November 1, 2003, so that their calendar taxation years terminated early on October...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(2.11) | purposes of s. 87(2.11) is to allow parent to use losses realized by the new corporation (so as to carry back) | 230 |

17 June 2003 External T.I. 2002-0178255 - FORGIVENESS OF DEBT DEBT AFTER AOC+AMALG

The non-capital losses of a subsidiary which amalgamates with its parent would be available to be applied against a forgiven amount arising on the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(3) | 92 |

Paragraph 87(2.1)(a)

Administrative Policy

S4-F7-C1 - Amalgamations of Canadian Corporations

Continuity rule re CUEC

1.54.1 Paragraph 87(2.1)(a.1) provides a continuity treatment in respect of the various amounts that are relevant in...

Paragraph 87(2.1)(a.1)

Administrative Policy

3 December 2024 CTF Roundtable Q. 6, 2024-1038251C6 - EIFEL - Pre-Regime Election and Amalgamations and Liquidations

The legislation enacting ss. 18.2 and 18.21 allows a taxpayer to elect to calculate its excess capacity for each of the three taxation years (the...

Subsection 87(2.11) - Vertical amalgamations

Administrative Policy

S4-F7-C1 - Amalgamations of Canadian Corporations

1.52 …[T]he new corporation formed on a qualifying vertical amalgamation can apply its post-amalgamation losses against the pre-amalgamation...

2011 Ruling 2011-0411821R3 - Interest deductibility and loss carry backs

a limited partnership ("BForLP") owns substantially all of the membership interests in a (presumably Netherlands) holding cooperative which owns...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | cross-border downstream loan to distribute cross-border PUC | 234 |

26 October 2006 External T.I. 2006-0170341E5 F - Subsections 87(2.1) and 87(2.11)

Canco, and it wholly-owned subsidiary, Subco1 amalgamated on November 1, 2003, so that their calendar taxation years terminated early on October...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(2.1) | s. 87(2.11) does not affect the aging of previously-incurred losses and is relevant to carry-backs by the Amalco | 309 |

22 June 1999 Income Tax Severed Letter 9833526 - VERTICAL AMALGAMATION, GOVERNMENT ASSISTANCE

Following a vertical amalgamation, the amalgamated corporation would not be able to carry back ITCs generated by it to reduce Part I tax of the...

94 C.P.T.J. - Q.14

S.87(2.11) does not permit the carry-back of non-capital losses of a predecessor subsidiary corporation for utilization by the predecessor parent...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 66.1 - Subsection 66.1(6) - Canadian exploration expense - Paragraph (d) | 83 |

Income Tax Regulation News, Release No. 3, 30 January, 1995 under "Subsection 87 (2.11)"

S.87(2.11) does not allow losses of a wholly-owned subsidiary corporation to be applied against the taxable income of its parent for taxation...

25 February 1993 T.I. (Tax Window, No. 30, p. 19, ¶2468)

S.87(2.11) permits an amalgamated corporation to carry back its non-capital losses to the predecessor parent corporation, but not to the...

1992 A.P.F.F. Annual Conference Q.3 (January - February 1993 Access Letter, p. 51)

The purpose of s. 87(2.11) is to make the consequences of a vertical amalgamation similar to those for a winding-up.

Articles

Stan Shadrin, Manu Kakkar, David Carolin, "Application of Part IV Tax to Amalgamations of Companies Owned by Trusts with Corporate Beneficiaries", Tax for the Owner-Manager, Vol. 22, No. 1, January 2022, p. 1

CRA position on year-end timing of s. 104(19) dividend (p. 1)

- Per 2012-0465131E5, 2016-0647621E5 and 2018-0757591I7, a dividend received and paid...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(2) | 270 |

Subsection 87(3) - Computation of paid-up capital

Administrative Policy

S4-F7-C1 - Amalgamations of Canadian Corporations

1.87 Although subsection 87(3) limits the aggregate paid-up capital of the issued shares of the new corporation, there is no specific provision...

80 C.R. - Q.29

RC may not object to the shifting of paid-up capital on an amalgamation if it is satisfied that the shifting is not primarily for the benefit of...

Articles

Tetreault, "The Application of Subsection 87(3) in an Amalgamation Squeeze-out", Canadian Current Tax, November 1988, p. 41

The CBCA would appear to have provided less flexibility than the OBCA in avoiding a grind under s. 87(3) on an amalgamation squeeze-out.

Subsection 87(3.1) - Election for non-application of subsection (3)

Administrative Policy

S4-F7-C1 - Amalgamations of Canadian Corporations

1.88 When a new corporation has more than one class of shares, a proportional reduction of paid-up capital under subsection 87(3) may, in certain...

Subsection 87(4) - Shares of predecessor corporation

Cases

Husky Oil Limited v. Canada, 2010 DTC 5089 [at at 6887], 2010 FCA 125

In order to accomplish a sale of a subsidiary of the taxpayer on a tax-deferred basis for a purchase price of $15.5 million payable in 25 years'...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Onus | 88 | |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(4) | 190 | |

| Tax Topics - Statutory Interpretation - Specific v. General Provisions | avoidance of two statutory deeming rules creating two different statutory fictions | 190 |

Administrative Policy

25 November 2021 CTF Roundtable Q. 1, 2021-0911841C6 - Indemnities and subsection 87(4)

There has been a triangular amalgamation under which a subsidiary of Parent amalgamated with Target and the Target shareholders received shares of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(1) | damages paid for breach of rep following an amalgamation did not breach s. 87(1)(a) | 144 |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(3) | when escrowed shares are cancelled as compensation for breach of representations of the shareholders, the payment for s. 84(3) purpose is those shares’ FMV | 136 |

15 September 2017 External T.I. 2017-0696821E5 F - Amalgamation

Two individuals, Mr. A and Mr. B wholly-own two corporations of equal value (A Inc. and B Inc.), which amalgamate. On the amalgamation, the two...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(1) - Paragraph 87(1)(a) | receipt of cash on amalgamation did not preclude qualification under s. 87(1) [per Envision, 2013 SCC 48?] | 163 |

15 August 2018 Internal T.I. 2018-0749931I7 - Subsections 87(1), (1.1) and (4)

CRA confirmed the continuing correctness of the statement in S4-F7-C1, Amalgamations of Canadian Corporations, para. 1.74 that:

Where shares of a...

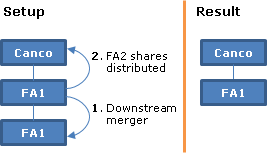

8 July 2015 External T.I. 2014-0550641E5 - Absorptive merger-exchange of shares

Canco held all the shares of FA1 with an ACB and FMV of $100, and $200, respectively, and all the shares of FA2 with an ACB and FMV of $100. FA1...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(8.2) | s. 87(8.2)(f) relief for absorptive mergers (where no shares are issued) also indirectly extends to operation of s. 87(4) | 121 |

S4-F7-C1 - Amalgamations of Canadian Corporations

1.69 For greater certainty, the rollover under subsection 87(4) is not available to shareholders whose shares of a predecessor corporation are...

Example 5

The 87(4) exception can be illustrated by the following example.

A parent owns all of the shares of Pco, which have an aggregate adjusted cost...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(t) | 102 |

2002 Ruling 2002-0177163 - Subsection 87(4) - S/H Rights Plan

Rights under a shareholder rights plan of Parent received by shareholders of Target on a triangular amalgamation of Target, a subsidiary of Parent...

7 June 2001 External T.I. 2001-0086165 F - REGLES DE ROULEMENT ET REER

CCRA confirmed that the tax treatment of a transaction subject to s. 85, 85.1, 86 or 87 will not differ where the shareholder is an RRSP (or...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) | ss. 85, 85.1, 86 and 87 apply to RRSPs and RRIFs | 26 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Taxpayer | RRSP is a taxpayer | 89 |

6 January 2000 External T.I. 9929675 F - FUSION - CAPITAL VERSÉ ET PBR

CCRA indicated that since the HopcoB stated capital was $682, and the transfer of the HopcoA Class B shares by Mr. X to HopcoB resulted in an...

23 February 1999 External T.I. 9832225 - AMALGAMATION, IT-474R

The policy in IT-474R, para. 40 (respecting the maintenance of ACB when preferred and common shares of a predecessor are converted into preferred...

Handbook on Securities Transactions, 94-110(E)

No reporting is required if, during an amalgamation, a shareholder receives cash or some other consideration totalling $200 or less, instead of a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 201 - Subsection 201(6) | 0 |

92 C.R. - Q.32

Where a corporation whose shares are owned by an individual amalgamates with a loss company whose shares are held by, and whose loan capital is...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | 74 |

25 August 1992, T.I. 921458 (April 1993 Access Letter, p. 144, C82-113)

The position in IT-474R, that s. 87(4) will not be applied where an amalgamation agreement provides that the preferred and common shares of a...

Subsection 87(4.3) - Exchanged rights

See Also

Envision Credit Union v. The Queen, 2010 DTC 1399 [at at 4585], 2010 TCC 576, aff'd 2012 DTC 5055 [at 6842], 2011 FCA 321, aff'd 2013 DTC 5144 [at 6275], 2013 SCC 48

Webb, J. found, in obiter dicta (at para. 89), that an amalgamated corporation resulting from an amalgamation that was not described in s. 87(1)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(21) - Undepreciated Capital Cost - E | 100 | |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4) - Paragraph 152(4)(a) - Subparagraph 152(4)(a)(i) | incorrect position was thoughtfully taken | 63 |

| Tax Topics - Statutory Interpretation - Redundancy/ reading in words/ speaking in vain | 50 |

Subsection 87(4.4)

Paragraph 87(4.4)(d)

Subparagraph 87(4.4)(d)(i)

Articles

Gregory M. Johnson, Wesley R. Novotny, "An Update on Flow-through Shares in the Energy Sector", 2016 Conference Report (Canadian Tax Foundation),12:1-39

Issues under s. 87(4.4)(d)(i) if further disposition by 1st purchaser or where dissent on amalgamation (pp. 12:19-20)

Subsection 87(4.4) applies...

Subsection 87(7) - Idem [Adjusted cost base]

Cases

Canada v. Dow Chemical Canada Inc., 2008 DTC 6544, 2008 FCA 231

The taxpayer ("Amalco") was formed on the amalgamation of two corporations, one of which ("UCCI") had previously incurred interest-bearing...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 78 - Subsection 78(1) | 197 |

Administrative Policy

S4-F7-C1 - Amalgamations of Canadian Corporations

1.58 Since paragraph 87(7)(d) provides that the provisions of the Act apply as if the new corporation had incurred or issued the debt at the time...

Articles

Kim Maguire, Jeffrey Shafer, "Trends in Buy/Sell Transactions", draft 2021 Conference Report

Application of s. 87(7) to earnout payments (p. 6)

- S. 87(7) (which also applies to s. 88(1) wind-ups by virtue of s. 88(1)(e.2)) has the effect...

Subsection 87(8) - Foreign merger

Administrative Policy

15 September 2017 External T.I. 2017-0709331E5 - Vertical absorptive foreign merger

Three wholly-owned stacked subsidiaries of Canco (FA1 holding FA2 holding FA3) effect a foreign merger under which FA2 and FA3 simultaneously...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition - Paragraph (n) | a simultaneous absorptive merger of FA3 (held by FA2) and FA2 (held by FA1) into FA1 would result in a disposition of the FA2 shares | 281 |

16 October 2009 Internal T.I. 2009-0337721I7 F - Perte lors de fusion étrangère

Holdco, received shares of the foreign merged corporation in replacement of its shares of a public American company. After filing a return in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(3.5) - Paragraph 40(3.5)(b) | s. 40(3.4) not applicable to foreign triangular merger to which s. 87(8) was elected not to apply | 59 |

Articles

Gordon Zittlau, "Corporate Reorganizations Involving Taxable Canadian Property – Foreign Merger Considerations", International Tax Planning (Federated Press), Vol. XX, No. 3, 2015, p. 1407

Where there is a merger of two foreign corporations whose shares are taxable Canadian property (because of an underlying Canadian real estate or...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition - Paragraph (n) | 430 |

Mark, Thon-That, "Cross-Border Reorganizations", International Tax Seminar, IFA, 19 May 1999, c. 6.

R. Ian Crosbie, "Canadian Income Tax Issues Relating to Cross-Border Share Exchange Transactions", 1997 Corporate Management Tax Conference Report, c. 12.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85.1 - Subsection 85.1(3) | 0 |

Schwartz, "Tax-Free Reorganizations of Foreign Affiliates", 1984 Canadian Tax Journal, November-December 1984, p. 1039.

Subsection 87(8.1)

Administrative Policy

2016 Ruling 2015-0617351R3 - payments under a German profit transfer agrmt “PTA"

The proposed transactions describe the merger of one German CFA (FA4) with another sister German CFA (FA3), with FA3 as the survivor. The merger...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(2) | double PTA transferring profits from German grandchild to German parent CFA | 516 |

2 June 2003 External T.I. 2003-0013315 - Foreign merger, fractional shares

The position on receipt of cash in lieu of fractional shares on an amalgamation that is intended to be governed by s. 87(1), as described in...

25 August 2000 External T.I. 2000-0026245 - Foreign Mergers - 87(8.1)

Confirmation that there was a qualifying "foreign merger" where Canco launches a share-for-share exchange takeover bid to acquire shares of Target...

2000 Ruling 2000-002395

A vertical merger between a US corporation with a Canadian branch business ("Absorbco") and its US parent ("Subco 3") under which Absorbco...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(b) | 136 |

28 February 2000 External T.I. 1999-001436

A foreign triangular merger qualified as a foreign merger notwithstanding that shareholders of the target would receive shares both of the merged...

14 December 1998 External T.I. 9811305 - FOREIGN MERGER

Where Subco A, Subco B and Parentco are all resident in the U.S. with Subco A being a wholly-owned subsidiary of Parentco, Parentco holding less...

Robert D'Aurelio, "International Issues

A Revenue Canada Perspective," 1990 C.R., p. 44: 13:

...it is the department's view, after giving consideration to the intention of subsections...

84 C.R. - Q.50

Where one or more predecessor corporations continue in the form of one corporate entity, that corporate entity is considered to be a new foreign...

Subsection 87(8.2) - Absorptive mergers

See Also

La Mancha Group International B.V. v Commissioner of Taxation, [2020] FCA 1799

It was proposed that the applicant (“LMGI”), which was a Netherlands private limited company that was wholly-owned by a Luxembourg public...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 165 - Subsection 165(1) | an absorptive merger of a Dutch into a Lux company rendered the Lux survivor as the “taxpayer” for continuing or launching objections | 582 |

Administrative Policy

2023 Ruling 2022-0958521R3 - foreign absorptive mergers

Background

Four stacked wholly-owning US corporations (Taxpayers 1 to 4, all of them qualifying persons under the Canada-US Treaty (the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 13 | disposition of shares of companies resident in third countries and which were taxable Canadian property was exempted under XIII(4) of the Canada-US Treaty | 116 |

8 July 2015 External T.I. 2014-0550641E5 - Absorptive merger-exchange of shares

In the case of an absorptive merger of FA2 into FA1 (as the survivor) where FA2 ceases to exist and its shares are cancelled, s. 87(8.2)(f) deems...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(4) | s. 87(8.2)(f) relief for absorptive mergers (where no shares are issued) also indirectly extends to operation of s. 87(4) | 219 |

4 March 2013 Internal T.I. 2012-0449371I7 - Downstream absorptive merger

{kind=link}

In 2006, a wholly-owned CFA (FA1) of Canco merged with a wholly-owned subsidiary (FA2) of FA1, with FA2 as the surviving corporation under the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition - Paragraph (n) | 132 |

Subsection 87(8.3)

Articles

Edward A. Heakes, "Another Wave of Foreign Affiliate Proposals", International Tax Planning, Volume XVIII, No. 4, 2013, p. 1275

Avoidance of s. 85.1(4) eliminated (p. 1276)

It is currently arguably possible to avoid this limitation [in s. 85.1(4) by utilizing a triangular...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Taxable Canadian Property | 84 | |

| Tax Topics - Income Tax Act - Section 91 - Subsection 91(1.2) | 90 |

Subsection 87(8.4)

Administrative Policy

4 March 2025 External T.I. 2025-1053731E5 - DOF Explanatory Notes on Subsections 87(8.4) & (8.5) – Inconsistent Statement

The Explanatory Notes to ss. 87(8.4) and (8.5) provide:

New subsections 87(8.4) and (8.5) allow taxpayers to elect for dispositions of taxable...

Articles

Joint Committee, "Technical Amendments Package of September 16, 2016", Submission letter of 15 November 2016

Only extends to shares of Cancos

Ss. 87(8.4) and (8.5) in the 16 September 2016 draft legislation provide a tax deferral only for shares of...

Subsection 87(8.5)

Administrative Policy

21 November 2017 CTF Roundtable Q. 14, 2017-0724241C6 - Section 116 procedures for tax-deferred dispositions on foreign mergers

For foreign mergers occurring after September 15, 2016, will CRA accept elections of the new corporation and disposing predecessor foreign...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 116 - Subsection 116(1) | s. 87(8.5) election with evidence of ACB will be accepted as basis for certificate | 294 |

Subsection 87(9) - Rules applicable in respect of certain mergers

Administrative Policy

S4-F7-C1 - Amalgamations of Canadian Corporations

1.12 … In general terms, this [s. 87(9)(c)(ii)] additional amount is equal to the amount by which the tax cost of the assets (less liabilities)...

5 February 1993 T.I. (Tax Window, No. 29, p.18, ¶2434)

The cost amount of Canadian resource properties for purposes of s. 87(9)(c) is nil irrespective whether or not there are undeducted resource pools.

24 June 1991 T.I. (Tax Window, No. 4, p. 7, ¶1315)

Discussion of reorganization in which the "bump" is unavailable because after the amalgamation the parent does not own all the shares of the...

Articles

Schwartz, "Statutory Amalgamations, Arrangements and Continuations: Tax and Corporate Law Considerations", 1991 Conference Report, c. 9.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(1) | 0 |

Richler, "Triangular Amalgamations", March/April 1985 Canadian Tax Journal, p. 374

RC has been willing to accommodate transactions whereby option holders and debenture holders of a predecessor corporation in effect receive...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(7) - Paragraph 256(7)(b) | 31 |

Paragraph 87(9)(a.4)

Administrative Policy

3 December 2019 CTF Roundtable Q. 13, 2019-0824491C6 - Triangular Amalgamation

In Scenario 1, Subco, which is a wholly-owned subsidiary of Parentco, amalgamates with Targetco (like Subco and Parentco, a taxable Canadian...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | GAAR may apply to the use of a “Midco” to step up the tax basis of a target investment on a triangular amalgamation | 205 |

19 February 1991 External T.I. 903669 1991-110 - Amalgamation

Corporation A owns 100% of corporation B. Corporation B and the public own 66% and 34% of corporation C, respectively. For various reasons,...

Subsection 87(10) - Share deemed listed

Administrative Policy

S4-F7-C1 - Amalgamations of Canadian Corporations

1.79 In certain amalgamations, the shares of a predecessor corporation which were listed on a designated stock exchange may be temporarily...

Subsection 87(11) - Vertical amalgamations

Administrative Policy

S4-F7-C1 - Amalgamations of Canadian Corporations

1.78 On an amalgamation described in [s. 87(11)], a capital gain may arise for the parent. Specifically,… if the paid-up capital of the...

2012 Ruling 2010-0355941R3 - reverse subsidiary merger - 87(1) & 87(11)

Under a BC plan of arrangement, a BC corporation ("SubcoTarget") is merged with its wholly-owned BC subsidiary ("Target") to form "Amalco" with...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(1) | reverse triangular "E" merger - survivor style amalgamation | 209 |

9 December 2011 External T.I. 2011-0428071E5 - Clarifications of Application of 87(11)

general discussion of application of s 88(1)(d) to situation in which Parent has two successive vertical amalgamations with its wholly-owned...

21 March 1997 External T.I. 9706705 - VERTICAL AMALGAMATION - COST BUMP

Confirmation that the rules in s. 88(1)(c.3) apply on a vertical amalgamation.

6 February 1997 External T.I. 9701005 - 87(11) BUMP WHERE ASSETS ALREADY DISTRIBUTED?

Where in connection with the winding-up of a subsidiary, the subsidiary has already distributed its property to its parent and it is then decided...