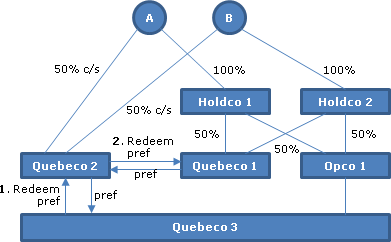

Paragraph 55(3)(a)

Administrative Policy

10 October 2024 APFF Roundtable Q. 6, 2024-1028881C6 F - Revenu protégé

CRA, when asked to comment on the application of s. 55(3)(a) to the redemption in Example 12 of the “CRA Update on Subsection 55(2) and Safe...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(c) | safe income was not allocable to preferred share issued on s. 85(1) roll-in of goodwill | 336 |

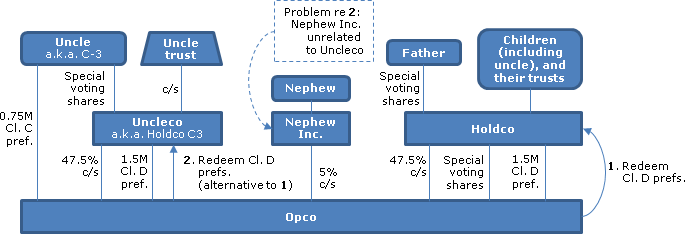

2023 Ruling 2022-0923451R3 F - 55(3)(a) internal reorganization

Background

Mr. X and Ms. X are the parents of Messrs. A, B, C and D. Mr. X has direct or indirect voting control of most of the corporations...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(c) | proration of DSI on s. 55(3)(a) spin-offs based on the net cost amount of the property spun off | 447 |

23 March 2022 External T.I. 2021-0921261E5 - Bill C-208 - 55(5)(e)(i)

S. 55(5)(e)(i) deems siblings to deal with each other at arm’s length for s. 55 purposes. Bill C-208 (a Private Member’s bill) amended s....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(5) - Paragraph 55(5)(e) - Subparagraph 55(5)(e)(i) | under the s. 55(5)(e)(i) exception (which cannot be used to multiply ACB), only one of dividend recipient and payer is required to be a QSBC | 207 |

2021 Ruling 2020-0874961R3 - 55(3)(a) Internal Reorganization

A family company (DC) controlled by father and that engaged in leveraged investing will spin off a portion of its share portfolio to respective...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(4) | spinoff of a portion of portfolio of DC (controlled by father) to father-controlled TCs for the children | 623 |

2020 Ruling 2020-0854401R3 - Internal Reorganization 55(3)(a)

Background

Three resident siblings hold the shares of DC directly (in the case of Siblings 1 and 2) and, in the case of all three, through their...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 86 - Subsection 86(1) | s. 55(3)(a) spin-off that includes a s. 86 exchange of identical shares | 123 |

2020 Ruling 2019-0834901R3 - Loss Utilization - Depreciable Property

CRA ruled on transactions for Profitco, which is an indirect wholly-owned Canadian subsidiary of a non-resident parent to utilize the non-capital...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Machinery and Equipment | depreciable property retained its character in superficial gain transaction | 216 |

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(1) - Paragraph 111(1)(a) | superficial gain transaction to transfer losses to a Profitco that is related through a non-resident parent | 195 |

16 February 2009 External T.I. 2008-0293911E5 F - Application of subsection 55(2).

A and B each hold 50% of the voting common shares of XYZ Inc. (whose assets consist of excess cash of $25 and active business assets of $75, such...

10 September 2018 External T.I. 2018-0772501E5 - Internal spin-off

Holdco A has wholly-owned Opco spin off Opco’s real estate to a newly-formed subsidiary of Holdco A (and sister of Opco), namely, to Realco. The...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) - Subparagraph 55(3)(a)(iii) - Clause 55(3)(a)(iii)(B) | s. 55(3)(a)(iii)(B) exclusion applied to lower tier internal spin-off transaction accompanied by an upper-tier sale by an arm’s length shareholder with a direct and indirect 16% shareholding | 490 |

2016 Ruling 2016-0648991R3 - Internal spinoff reorganization of XXXXXXXXXX

Current structure

ParentCo, a taxable Canadian corporation and a public corporation, owns all the common shares of CanSub1 and all the shares of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85.1 - Subsection 85.1(3) | a double transfer of shares under s. 85(1) and 85.1(3) would not affect the shares’ capital property status | 179 |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Shares | shares did not lose capital property character on internal spin-off transfer with a view to their further dorp-down | 108 |

2016 Ruling 2016-0635101R3 - 55(3)(a) Spin-Off to Use Parent Losses

Background

Subco is wholly-owned by Parent, which holds all of its common shares (“Subco Old Common Shares”) and all of its non-voting,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(21.1) - Paragraph 13(21.1)(a) | where land transferred under s. 85(1) along with terminal loss building, elect high with a view to s. 13(21.1)(a) applying to reduce the land proceeds to ACB | 189 |

| Tax Topics - Income Tax Act - Section 86 - Subsection 86(1) | s. 86(1) applied where “dirty” s. 85 exchange mechanic used, but no s. 85 election made | 93 |

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) - Paragraph 85(1)(a) | elected amount deterines proceeds before s. 13(21.1)(a) grind | 203 |

2016 Ruling 2015-0623731R3 - Subsections 55(2) and (2.1)

Background

As described in 2015-0601441R3, Sub1 and Sub2 (both taxable Canadian corporations and wholly-owned subsidiaries of Parent, a public...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) - Forgiven Amount | policy on set-off of unequal redemption notes does not extend beyond a butterfly reorg | 433 |

| Tax Topics - Income Tax Act - Section 86 - Subsection 86(1) | stated capital of old shares required to be prorated amongst new classes based on relative FMV | 136 |

2017 Ruling 2016-0675881R3 - Paragraph 55(3)(a) Internal Reorganization

Current structure

Canco is a Canadian-controlled corporation holding “Parcel One” and “Parcel Two” (consisting in each case of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(4) | s. 55(3)(a) split-up between Newcos for two siblings which were related due to multiple-voting shares held by the father’s and mother’s Holdco | 170 |

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) - Paragraph 85(1)(e) | UCC on s. 55(3)(a) spin-off prorated based on relative capital cost rather than FMV | 174 |

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) - Paragraph 186(1)(b) | where circular RDTOH calculation arises on spin-off transaction, it is for the TSOs to sort out which corporations should bear Part IV tax | 249 |

12 May 2017 External T.I. 2017-0683511E5 F - Purpose tests of a dividend or repurchase of share

The CRA position on creditor-proofing suggested that if Opco, which has no safe income and whose common shares have a nominal adjusted cost base...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(b) - Subparagraph 55(2.1)(b)(ii) | redeeming common shares otherwise than out of safe income may be GAARable | 346 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | use of s. 55(3)(a) redemption exception to circumvent safe income limitation could be offensive | 58 |

13 January 2016 External T.I. 2015-0604521E5 - ACB increase in paragraph 55(3)(a) reorganization

Parentco owns 100% of Holdco which owns 100% of Opco. There are two alternatives for spinning-off one of Opco’s existing business lines to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | objectionable for a s. 55(3)(a) spin-off to result in an increase in the aggregate outside basis | 173 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) - Forgiven Amount - Element B - Paragraph B(a) | contribution of note by creditor to debtor | 36 |

2015 Ruling 2014-0559181R3 - Internal Reorganization

{kind=link}

Current Structure

Parentco (a subsidiary wholly-owned corporation of Ultimate Parentco, which is a listed public corporation) holds all of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(1) - Paragraph 111(1)(a) | internal spinoff by "profitco" for previous loss transfer rulings will not prejudice those rulings | 171 |

14 April 2015 External T.I. 2015-0570021E5 F - Présomption de gain en capital

S. 55(3.01)(g) generally permitted two unrelated individuals to spin-off real estate from a jointly owned Opco to a newly-incorporated...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.01) - Paragraph 55(3.01)(g) | application of safe harbour where holdco interposed before spin-off transaction | 394 |

11 February 2015 External T.I. 2014-0557251E5 F - paragraph 110.1(1)(c) and clause 55(3)(a)(i)(B)

In the course of a series of transactions including the redemption of shares subject to s. 84(3), a corporation made a gift of cultural property...

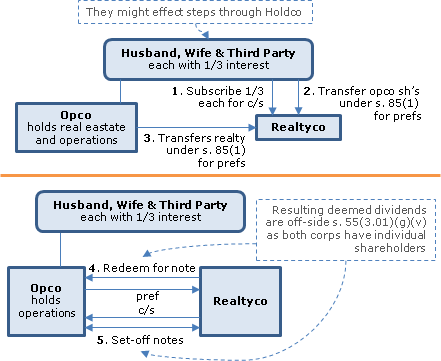

10 October 2014 APFF Roundtable Q. 16, 2014-0538031C6 - APFF 2014 Q. 16 - Capital gain

{kind=link}

Facts

The exception in s. 55(3)(a) would not be available where a new corporation was created in the series. Consider this example:

- Husband,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(2) - Paragraph 251(2)(b) - Subparagraph 251(2)(b)(i) | incorporator related to corporation | 67 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.01) - Paragraph 55(3.01)(g) | interposition of holdco to permit related-person spin-off compliant with s. 55(3)(a)(ii) and (v) | 925 |

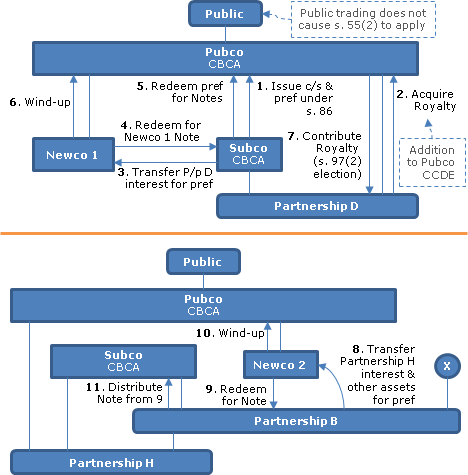

2014 Ruling 2013-0505431R3 - XXXXXXXXXX

{kind=link}

Existing structure

Pubco, a CBCA public corporation, and Subco, its wholly-owned CBCA corporation, are partners, along with GPCo (also...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 66.2 - Subsection 66.2(5) - Canadian development expense - Paragraph (e) | transfer of royalty from partly-owned partnership | 464 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) | delay in filing articles of dissolution | 55 |

| Tax Topics - Income Tax Act - Section 97 - Subsection 97(2) | s. 97(2) applicable to contribution (no equity consideration) | 61 |

25 April 2014 External T.I. 2014-0528011E5 F - Subsection 55(2) - redemption of shares

{kind=link}

A and B each is the sole shareholder of Holdco 1 and Holdco 2, respectively, which each holds 50% of the voting common share of Opco as well as...

3 January 2014 External T.I. 2013-0514021E5 F - Subsection 55(2) - redemption of shares

{kind=link}

Structure

Holdco is controlled by Father through his holding of special voting shares, and its equity is held by his three children (C-1, C-2 and...

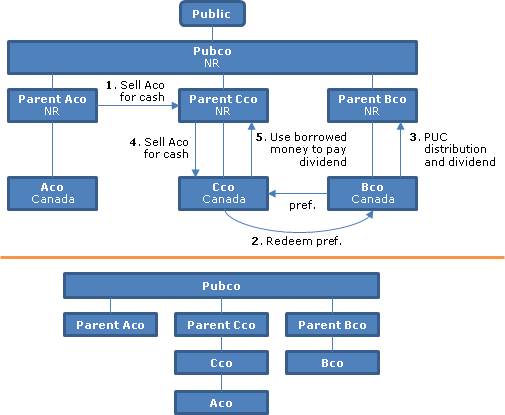

2013 Ruling 2013-0501811R3 - Internal Reorganization - 55(3)(a)

{kind=link}

Starting structure

Aco, Bco and Cco are wholly-owned Canadian subsidiaries of non-resident holding companies, namely, ParentAco, ParentBco and...

16 February 2011 External T.I. 2012-0435381E5 - Subsection 55(2) - redemption of shares

A percentage increase of 1.28% or 1.33% could be considered not to be significant for purposes of s. 55(3)(a)(ii) or (v).

10 June 2002 External T.I. 2002-0138885 F - Redemption of Preferred Shares

Opco redeems its preferred shares held by PortfoliocoX (wholly owned by Mr. X) at a time that all the common shares of Opco are owned equally by...

12 March 2002 External T.I. 2002-0125885 F - Section 55(3)(a) - Exception55(3)(a)

Holdco A and Holdco B held separate classes of shares of Opco, each with 50% of the votes. Holdco A and B were wholly-owned by a spousal trust...

27 January 2000 External T.I. 1999-0009375 - DIVIDENDS SUBJECT TO 55(2)

The exemption in s. 55(3)(a) would not apply to the payment of a dividend by a holding company that was equally owned by two brothers through...

10 December 2001 External T.I. 2001-0109195 F - Test d'objet à 55(2)

S. 55(3)(a) applied to creditor-proofing transaction in which husband and wife transferred 80% and 20% of the shares of Opco to a new Holdco...

1999 APFF Round Table, Q. 15

"The Department considers, however, that there is generally a significant increase in the total direct interest of the common shareholders of a...

3 February 1999 Ruling 971084

Ruling that a normal course issuer bid (which would result in some minority shareholders who do not sell their shares having their percentage...

1 December 1998 TEI Conference, Q. XXIII

"In determining whether an increase in interest in a corporation is 'significant' in the context of paragraph 55(3)(a), an analysis of the...

7 July 1998 External T.I. 9641165 - EXEMPTION FROM 55(2)

"The issuance of shares does not represent an event described in subparagraph 55(3)(a)(ii)."

3 November 1997 External T.I. 9725615 - INCREASE IN INTEREST

"In circumstances where no person has acquired any shares of the corporation in question, it is our view that for the purposes of determining...

30 November 1996 Ruling 9704023 - SUBSTANTIAL ISSUER BID

Ruling that a substantial issuer bid (effected by way of auction tender) in which a major shareholder of the corporation would have a...

20 April 1997 External T.I. 9711155 - 55(3)(A)(I) EXEMPTIONS

"Where a share whose fair market value exceeds its paid-up capital is redeemed for an amount of cash equal to its fair market value, the...

1996 Ontario Tax Conference Round Table, "Creditor Protection and Butterfly Transactions", 1997 Canadian Tax Journal, Vol. 45, No. 1, pp. 214-215

After it was noted that the exception in s. 55(3)(a) would apply where two individuals hold their investment in Opco through Holdco, and the...

1996 Corporate Management Tax Conference Report, Q. 15

The related-person test should be applied at the time of the relevant disposition of property or increase of interest.

27 June 1995 External T.I. 9425365 - DISPOSITION OF CASH

A payment of cash on the purchase for cancellation of common shares held by an estate would be considered to be a disposition of property by the...

16 September 1992 T.I. (Tax Window, No. 24, p. 16, ¶2196)

A beneficiary holding a contingent beneficial interest in an estate whose property includes a share of a corporation, has an "interest" in that...

10 January 1992 CGA Roundtable, Q. 19, 7-912224

Where Mr. A and Mr. B, who each own 50% of the shares of A Ltd. and B Ltd., enter into a shareholders' agreement with respect to their...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.6 - Subsection 110.6(7) | 56 | |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(a) | FMV of debt rather than amount owing | 57 |

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(1) - Paragraph 53(1)(c) | contribution of capital on conversion of debt to lower FMV shares | 204 |

10 January 1992 Memorandum (Tax Window, No. 17, p. 15, ¶1773)

Where a parent, in order to reduce its debt, instructs its subsidiary to sell properties to a third party and use the cash proceeds to pay a...

10 January 1992 Memorandum (Tax Window, No. 17, p. 14, ¶1773)

S.55(2) will apply where one wholly-owned subsidiary of a corporation transfers property to another wholly-owned subsidiary of that parent with...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(e) | 27 |

10 January 1992 Memorandum (Tax Window, No. 17, p. 12, ¶1773)

In order for the exemption in s. 55(3)(a) to apply to a transaction involving a transfer of assets from a corporation owned equally by Messrs. A...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2) | 19 | |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2) | 48 |

24 February 1992 Memorandum (Tax Window, No. 13, p. 13, ¶1627)

A participation in a phantom stock plan may represent an interest in a corporation.

19 December 1990 T.I. (Tax Window, Prelim. No. 2, p. 6, ¶1054)

The exemption in s. 55(3)(a) generally will be available in a reorganization undertaken to facilitate the division of family assets on divorce....

19 March 1990 T.I. (August 1990 Access Letter, ¶1371)

A single-wing butterfly reorganization carried out as part of a divorce settlement whereby property ends up owned by the wife's corporation will...

29 January 1990 T.I. (June 1990 Access Letter, ¶1268)

If at the time of the preliminary transaction the taxpayer has the intention of implementing subsequent transactions, the subsequent transactions...

3 November 89 T.I. (April 90 Access Letter, ¶1172)

A U.S. corporation has a wholly-owned Canadian operating subsidiary ("Subco 1") and a newly incorporated wholly-owned Canadian subsidiary ("Subco...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | 109 |

1 November 89 T.I. (April 90 Access Letter, ¶1172)

The exemption will not be available where a corporation transfers property to a related corporation under the rollover in s. 85(1), the transferee...

Articles

David Carolin, Manu Kakkar, Boris Volfovsky, "Tax Alchemy and Paragraph 55(3.01)(g): Converting a 55(3)(b) Divisive Reorganization into a 55(3)(a) Related-Party Butterfly", Tax for the Owner-Manager, Vol. 24, No. 1, January 2024, p. 7

Suppose that Opco is owned on an 85-15 basis by two arm’s-length shareholders, Aco and Bco. If Opco wishes to spin off the real property used in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.01) - Paragraph 55(3.01)(g) | 534 |

Doron Barkai, Alexander Demner, "Dealing with New Subsection 55(2): Issues and Strategies", 2016 Conference Report (Canadian Tax Foundation), 6:1–56

Avoidance of s. 55(2) through accessing related party exemption (p. 6:31)

[O]ne strategy to avoid subsection 55(2) is to restructure a dividend...

Carla Hanneman, "Reorganization Strategies for Proposed Paragraph 55(3)(a)", Canadian Tax Focus, Volume 5, Number 3, August 2015, p.8.

Accessing new s. 55(3)(a) rules by ensuring that all dividends arise under s. 84(3) (pp. 8-9)

Consider a corporate group comprising Parentco,...

Benjamin Alarie, Julia Lockhart, "The Importance of Family Resemblance: Series of Transactions After Copthorne", Canadian Tax Journal (2014) 62:1, 273-99.

Purpose of s. 55(3)(a)(ii) (pp. 96-7)

Subparagraph 55(3)(a)(ii)… seems to have been enacted for the purposes of avoiding a relatively...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | 1229 |

Michael N. Kandev, Abraham Leitner, "Through the Looking Glass: Dividing up a Family Business in a Canada-US Cross-Border Context", 2011 Canadian Tax Journal, Vol 59, No. 4, p. 899: Canada-US cross-border divisions of family operations that are structured under s. 55(3)(a) are generally constrained by the stricter rules of Code section 355.

Firoz Ahmed, "Subsection 55(3) Update", Canadian Current Tax, Vol. 15, No. 8, May 2005, p. 1: CRA's "new position is that the acquisition of shares of a corporation representing less than three percent of the fair market value of the shares of the capital stock of the corporation will not generally result in a significant increase in interest even if the shares have a very high value".

K.A. Siobhan Monaghan, "Doomed (or 'Deemed') to Fail", Corporate Structures and Groups, Vol. V, No. 1, p. 253.

Subparagraph 55(3)(a)(i)

Administrative Policy

28 January 2008 External T.I. 2007-0250831E5 F - Part IV.1 and VI.1 Taxes - Subsection 55(2)

Retractable preferred shares ("Rollover Preferred Shares") of a CCPC (“Subco”) held by a public corporation (“Pubco”) which had ceased to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 191 - Subsection 191(4) | s. 191(4) unavailable where redemption occurred subsequently to reduction in redemption amount pursuant to a price adjustment clause | 370 |

| Tax Topics - Income Tax Act - Section 191.1 - Subsection 191.1(1) - Paragraph 191.1(1)(a) | dividend subject to s. 55(2) can also be subject to Pt. VI.1 tax | 110 |

| Tax Topics - Income Tax Act - Section 187.2 | application of Pt. IV.1 tax to a deemed dividend is ousted to the extent s. 55(2) applies | 115 |

18 July 2006 External T.I. 2005-0159781E5 F - Paragraph 55(3)(a)

Mr. X wholly owns Parentco , which wholly owns Sisterco and Holdco. Holdco owns 88 of the common shares of Subco (which carries on a business),...

Subparagraph 55(3)(a)(ii)

Administrative Policy

2024 Ruling 2023-0989121R3 F - Internal reorganization - 55(3)(a) and 55(3.01)(g)

The three unrelated individuals (A, B and C) holding the shares of Opco were to engage in preliminary estate-freeze transactions as a result of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.01) - Paragraph 55(3.01)(g) | transfer of real estate to separate Realtyco beneath a newly-formed Holdco | 605 |

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | 2 unrelated individuals were the settlors for each other’s family trust | 162 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | estate freeze transactions represented to be independent of subsequent transfer | 152 |

2018 Ruling 2018-0749491R3 - 55(3)(a) Reorganization

Background

DC’s Class B and C non-voting and Class A voting preferred shares are owned by Parent (giving him control) and its voting common...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(4) | Parent reps that he will control the TCs for commercial reasons | 288 |

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) - Paragraph 186(1)(b) | circularity avoided through intervening TC year end | 113 |

2018 Ruling 2017-0683941R3 - Split-up transactions

Structure

Amalco (which resulted from a recent amalgamation of Holdco 1 and its subsidiary, Opco) carries on Business 1 in Facility 1 and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | arm's length investment in proposed purchaser of spinco assets not part of spin-off series | 229 |

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) - Paragraph 186(1)(b) | year-end established in middle of cross-redemptions to avoid circularity | 220 |

2015 Ruling 2015-0605901R3 F - Présomption de gain en capital

CRA ruled (as well as providing an opinion under the July 31, 2015 draft amendments) on the non-application of s. 55(2)(a) to transactions, which...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.01) - Paragraph 55(3.01)(g) | separation of real estate assets beneath new holdco formed by unrelated shareholders | 567 |

| Tax Topics - Income Tax Act - Section 249.1 - Subsection 249.1(7) | taxation year end changed to immediately before building spin-off | 95 |

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) - Paragraph 186(1)(b) | year end selection to avoid Pt. IV circularity | 97 |

14 August 2012 External T.I. 2012-0450041E5 F - subsection 55(4)

Child Holdco holds common and preferred shares of a related corporation (Holdco). The preferred shares and (controlling) special voting shares of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(4) | s. 55(4) not engaged where transactions eliminate shareholdings but not unrelated status of unrelated person | 336 |

7 October 2011 Roundtable, 2011-0412161C6 F - Timing of the increase in interest - stock option

Mr. X implemented an estate freeze in favour of his children and a holding corporation respecting his wholly-owned operating corporation, which he...

9 November 2010 External T.I. 2010-0380661E5 F - Internal Reorganization

Son Inc. and Daughter Inc. (wholly-owned by Son and Daughter) and Father Inc. (owned by Father, Son and Daughter and a family trust with them as...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(4) | potential application of s. 55(4) where increase of interest of siblings companies is sheltered by control of Father – unless he held his shares to protect his “economic interests” | 371 |

5 May 2010 External T.I. 2010-0359791E5 F - Significant increase - redemption of shares

An estate freeze was implemented for the benefit of X’s child under which, in the course of a capital reorganization of Opco, Holdco (held by X)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 86 - Subsection 86(1) | s. 86 reorg where exchange of common for prefs followed by subscription for (old) commons | 73 |

6 February 2007 External T.I. 2006-0170921E5 F - Capital Gain Strip

Unrelated individuals (Mr. X and Mr. Y) each holding 50% of the shares of Holdco Inc. (which wholly-owns Opco Inc.) subscribe equally for special...

13 May 2005 External T.I. 2005-0126531E5 F - Capital Gain Strip/Significant Increase

Opco is wholly-owned by Holdco except that preferred shares of Opco are held by Employeeco, a CCPC whose common shares are held by employees who...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) - Subparagraph 55(3)(a)(v) | employees’ subscription for shares of employeeco and redemption years later of employeeco preferred shares held by parentco engaged the s. 55(3)(a)(v) exclusion | 149 |

18 March 2005 External T.I. 2005-0117691E5 F - Significant increase in interest in any corp

Two brothers (X and Y) each hold half the shares of Opco which, in turn, holds 35% of the shares (being common shares) of Subco. They jointly...

Articles

David Carolin, Manu Kakkar, "Freezes and Butterflies: Who Said Freezes are Easy?", Tax for the Owner-Manager,” Vol. 25, No. 2, April 2025, p. 9

Inability to effect post-spin-off freeze in favour of TC family trust if any unrelated beneficiaries (p. 9)

- Dad and Son, who are the 50-50...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.1) - Paragraph 55(3.1)(b) - Subparagraph 55(3.1)(b)(i) - Clause 55(3.1)(b)(i)(C) | 424 |

Subparagraph 55(3)(a)(iii)

Administrative Policy

2015 Ruling 2015-0604051R3 - Internal Reorganization

Background

XXXco1, a (U.S.?) corporation which is the survivor of a merger of three corporations and apparently is an indirect subsidiary of a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(1.11) | s. 55(3)(a) rulings conditional on U.S. parents accepting GAAR assessments to reduce their outside basis | 230 |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1.1) | pro-rata highly dilutive stock dividend | 117 |

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(2) | extensive reps required re series of transactions | 47 |

Clause 55(3)(a)(iii)(B)

Administrative Policy

10 September 2018 External T.I. 2018-0772501E5 - Internal spin-off

Holdco A and its wholly-owned CCPC subsidiary, Opco own real estate that is used in Opco’s active business. Holdco C (owned equally by husband...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) | a lower tier internal spin-off transaction accompanied by an upper-tier sale by a minority shareholder was subject to s. 55(2) | 253 |

Subparagraph 55(3)(a)(v)

Administrative Policy

29 October 2013 External T.I. 2013-0489771E5 F - Internal Reorganization - 55(3)(a)

Three brothers held Corporation A as to 1/3 each and their mother’s estate held all of Corporation B. Following the distribution of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | estate distribution of corporation followed by transfer of assets from related corporation could be part of same series | 171 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.2) - Paragraph 55(3.2)(d) | s. 55(3.2)(d) application to estate distribution of corporation to 3 sibling beneficiaries does not deem them to be related to each other | 248 |

13 May 2005 External T.I. 2005-0126531E5 F - Capital Gain Strip/Significant Increase

Opco is wholly-owned by Holdco except that preferred shares of Opco are held by Employeeco, a CCPC whose common shares are held by employees who...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) - Subparagraph 55(3)(a)(ii) | subscription by employees for shares of employeeco was part of series of transactions resulting in the redemption of shares held in employeeco, so that s. 55(3)(a)(ii) exclusion applied | 148 |

Paragraph 55(3)(b)

See Also

Deuce Holdings Ltd. v. R., 97 DTC 921, [1998] 1 CTC 2550 (TCC)

With respect to a divisive reorganization which entailed the receipt by the taxpayer both of a cash dividend and a deemed dividend, Bell TCJ....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2) | safe income on hand reduced by taxes, but not by inchoate retiring allowance | 54 |

Administrative Policy

30 November 1996 Ruling 9710373 - PUBLIC COMPANY SPIN-OFF

Favourable rulings given with respect to public company spin-off transactions.

1996 Corporate Management Tax Conference Round Table, Q. 16

"The 'reorganization' referred to in section 55 would normally include only transfers of property by the distributing corporation to its...

1996 Corporate Management Tax Conference Round Table, Q. 19 (C.T.O. "Butterflies - Tolerance Levels")

"The word 'approximate' provides limited scope for discrepancies ... . In 1991 we indicated that, for purposes of advance rulings, we are...

30 November 1995 Ruling 9634883 - PUBLIC COMPANY BUTTERFLY

Favourable ruling given on public company butterfly.

93 C.R. - Q. 13

A distribution to all shareholders that does not include all the assets of a particular type owned by the distributing corporation will not comply...

11 November 1993 Memorandum (Tax Window, No. 30, p. 3, ¶2482)

Where a corporation (A) is owned equally by three shareholders who deal with one another at arm's length and do not act in concert amalgamates...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(3.1) | 76 |

8 April 1993 T.I. (Tax Window, No. 30, p. 19, ¶2502)

An acquisition of property will not normally be considered to have occurred in contemplation of a butterfly reorganization where the acquisition...

13 January 1993 T.I. 922909 (November 1993 Access Letter, p. 496, ¶C38-180)

Discussion of availability of exemption, and of meaning of "reorganization", where a corporation transfers its shares of a wholly-owned subsidiary...

25 August 1992 T.I. (Tax Window, No. 23, p. 6, ¶2133)

RC will apply the look-through approach to a general partnership interest but not to a limited partnership interest. Accordingly, where Holdco...

Tax Professionals Mini Round Table - Vancouver - Q. 3 (March 1993 Access Letter, p. 101)

Where property of a particular corporation is transferred to a wholly-owned subsidiary of a corporate shareholder, the subsidiary must be wound-up...

26 November 1992 Memorandum (Tax Window, No. 27, p. 13, ¶2351)

RC's position that property received by a corporation on a winding-up of a partnership prior to the butterfly reorganization will not nullify the...

31 August 1992 Memorandum (Tax Window, No. 24, p. 3, ¶2191)

The use of s. 55(3)(b) to effect a transfer of assets deriving their value principally from real estate in the guise of a treaty-protected share...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 39 |

92 CR - Q.30

A faulty evaluation of distributed assets for purposes of attempting to comply with the requisite proportions set out in s. 55(3)(b) will not be...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | 21 |

92 C.R. - Q25

Even if the decision in The Queen v. Guaranty Properties, 90 D.T.C 6363 stands for the proposition that an amalgamating corporation does not cease...

17 July 1992 External T.I. 5-913100

The pro rata test in s. 55(3)(b) will be met if, following the transfer of the required percentage of property by the particular corporation to...

5 July 1991 Memorandum (Tax Window, No. 5, p. 18, ¶1338)

A favourable ruling will not be given in respect of a partial butterfly unless the ACB of the shares of the particular corporation are reduced by...

11 April 1991 T.I. (Tax Window, No. 2, p. 19, ¶1199)

GIC's which are current assets capable of reasonably prompt liquidation generally will be considered to be cash or near-cash assets.

27 December 1990 T.I. (Tax Window, Prelim. No. 2, p. 6, ¶1058)

Where on the dissolution of a partnership each partner's share of the distributed property is a proportionate interest in the specific items of...

19 April 1990 T.I. (September 1990 Access Letter, ¶1416)

Where in contemplation of a transfer of property to its shareholders in a butterfly reorganization a partnership of which the particular...

Hiltz, "The Butterfly Reorganization

Revenue Canada's Approach", 1989 Conference Report, p. 20:32.

Read, "Section 55

A Review of Current Issues", 1988 Conference Report, c. 18.

89 C.M.TC - Q.16

Real estate used partially in an active business and partially in a specified investment business will generally constitute two types of property.

89 C.M.TC - Q.17

RC will not only rule on a butterfly reorganization carried out on a gross asset basis, but will also accept the net equity method if the...

87 C.R. - Q.57

The transfer of all one type of property to the shareholders may qualify where the ACB of the shares of the transferor is reduced appropriately.

87 C.R. - Q.56

Although property distributed by way of dividend in a butterfly reorganization is subject to the proportionate sharing rules, preferred shares may...

ATR-47, February 24, 1992

Description of an estate thaw butterfly entailing the transfer of real estate by the estate freeze corporation to a corporation whose common...

Hiltz, "Section 55: An Update" 1984 Corporate Management Tax Conference Report, p. 40.

Articles

Firoz Ahmed, "Return of the Somersault", Canadian Current Tax, Vol. 11, No. 1, October 2000, p. 1.

Sider, "Corporate Reorganizations: A Review of a Divestiture", 1993 Conference Report, c. 14

Review of the spin-off of certain divisions of Ocelot Energy Inc.