Subsection 112(1) - Deduction of taxable dividends received by corporation resident in Canada

Cases

Fiducie financière Satoma v. Canada, 2018 FCA 74

A tax plan turned upon dividends that in fact were paid to a family trust (Satoma Trust) being attributed under s. 75(2) to a corporation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Tax Benefit | tax benefit to trust from tax-free dividend even though not distributed to a beneficiary | 277 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | using ss. 75(2) and 112(1) for tax-free dividends to trust thwarted s. 112(1) object to tax earnings when ultimately distributed | 319 |

| Tax Topics - Income Tax Act - Section 3 | pervasive rule that the same income is not to be taxed in 2 persons’ hands | 148 |

| Tax Topics - Statutory Interpretation - Double Taxation/Deduction (Presumption Against) | inclusion of income in more than one taxpayer’s hands is contrary to s. 3 | 294 |

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | use of s. 75(2) to access s. 112(1) deduction for dividend in fact received by family trust, was abusive | 286 |

| Tax Topics - Income Tax Act - Section 82 - Subsection 82(2) | s. 82(2) supports the primacy of s. 75(2) over the actual dividend recipient | 60 |

Minister of National Revenue v. Trans-Canada Investment Corporation Ltd., 55 DTC 1191, [1955] CTC 275, [1956] S.C.R. 49

The respondent bought shares in Canadian corporations and endorsed them to a trustee who in turn issued investment certificates to the respondent,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | double (or triple) taxation may be intended | 163 |

| Tax Topics - Statutory Interpretation - Expressio Unius est Exclusio Alterius | 39 |

Administrative Policy

2022 Ruling 2021-0910431R3 - Loss consolidation arrangement

CRA ruled on loss consolidation transactions involving a parent with losses and three indirect “Profitco” subsidiaries. The transactions did...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(1) - Paragraph 111(1)(a) | loss-consolidation transaction which avoided loans to the regulated Profitcos through the use of a partnership | 324 |

13 December 1989 T.I. (May 1990 Access Letter, ¶1228)

The deduction under s. 112(1) is applicable to dividends received by a corporation on shares included in its inventory insofar as ss.112(2.1),...

84 C.R. - Q.80

RC will scrutinize whether payments made under dividend rentals purporting to be dividends are in fact such.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | 19 |

Subsection 112(2.1) - No deduction permitted

See Also

Heron Bay Investments Ltd. v. The Queen, 2009 DTC 1606, 2009 DTC 1288

In obiter dicta, Hogan, J. noted (at para. 66) that the prohibition against an inter-corporate dividend deduction in s. 112(2.1) would apply where...

Société d’Investissement Desjardins v. Minister of National Revenue, 91 DTC 393, [1991] 1 CTC 2214 (TCC)

The taxpayer, which was a venture capital corporation, was found not to have received a deemed dividend on a term preferred share in the ordinary...

Reed v. Nova Securities Ltd., [1985] BTC 121 (HL)

As interpreted in General Motors Acceptance Corporation (U.K.) Ltd. v. IRC, [1987] BTC 71 (C.A.).

Shares acquired by the taxpayer did not...

Blok-Andersen v. MNR, 72 DTC 6309, [1972] CTC 338 (FCTD)

In the course of considering a submission that s. 85B(1)(B) of the pre-1972 Act (now s. 12(1)(b)) did not apply to an adventure in the nature of...

Administrative Policy

19 October 2023 Internal T.I. 2020-0856851I7 - Ordinary Course of Business

Indirect US operating subsidiaries of a Canadian insurance company were funded (or their acquisition was funded) in part through an indirect...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 258 - Subsection 258(4) - Paragraph 258(4)(a) | MRPS acquired by a Canadian insurance company subsidiary in order for the Luxco to loan-finance US operations were not acquired in the ordinary course | 584 |

3 May 2006 Internal T.I. 2005-0133341I7 F - Cours normal des activités de l'entreprise

As part of a reorganization relating to the sale of a share investment in Bco by Aco (a specified financial institution), a partnership of which...

92 C.M.TC - Q.12

The position at 84 C.R. - Q.62 is affirmed. Whether the corporation is an SFI only by virtue of being related to a financial institution is not...

19 March 1992 T.I. (Tax Window, No. 18, p. 11, ¶1819)

Generally, shares issued on the incorporation of a wholly-owned subsidiary where the proceeds are used to constitute permanent capital of the...

20 December 1990 Memorandum (Tax Window, Prelim. No. 3, p. 25, ¶1122)

The courts have rejected arguments to the effect that all securities acquired by certain types of corporation such as banks or life insurers have...

86 C.R. - Q.15

(1) shares acquired from a related corporation in the course of its reorganization that are quickly redeemed generally will not be considered to...

ATR-10 (31 July 86)

S.112(2.1) would not apply to the issuance of term preferred shares (which are retractable and have a participating dividend) by a subsidiary to...

84 C.R. - Q.62

Factors considered in determining whether shares were acquired in the ordinary course, including whether the funds raised on issuance provided...

80 C.R. - Q.23

Shares issued on the incorporation of a wholly-owned subsidiary would not as a rule be issued "in the ordinary course of business".

Articles

Elizabeth J. Johnson, James R. Wilson, "Financing Foreign Affiliates: The Term Preferred Share Rules and Tower Structures", (2006), vol. 54, no. 3 Canadian Tax Journal, 726-761.

Fien, "A Directors' Liability and Indemnifications, Section 160 Assessments and Ordinary Course of Business Provisions", 1992 Conference Report , pp.53:32-53:35.

Subsection 112(2.2) - Guaranteed shares

Administrative Policy

86 C.R. - Q. 14

The conditions respecting whether the guarantor is an SFI or associated with the issuer are relevant at the time a dividend is paid and not simply...

Articles

Webb, "Structuring International Joint Ventures: Canadian Tax Issues to Consider", Bulletin for International Fiscal Documentation , Vol. 48, No. 8/9, August/September 1994, Special IFA issue, p. 448

Discussion of "Unilever" and "Xerox" models.

Dyer, "Preferred Share Financing", 1986 Corporate Management Tax Conference, p. 20.

Discussion of background behind repeal of s. 112(2.2)(f) effective May 23, 1985.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Term Preferred Share | 0 |

Subsection 112(3) - Loss on share that is capital property

Cases

Toronto-Dominion Bank v. Canada, 2011 DTC 5125 [at at 6061], 2011 FCA 221, [2011] 6 CTC 19

The taxpayer ("TD") held common and preferred shares in a Canadian real estate company ("Oxford"). TD received dividends from Oxford over a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Transitional Provisions and Policies | 163 | |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(9) | 117 | |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | "series of transactions" must be pre-ordained absent s. 248(10) | 123 |

| Tax Topics - Statutory Interpretation - Ordinary Meaning | clear wording | 80 |

Administrative Policy

24 November 2013 CTF Roundtable, 2013-0508161C6 - Loss on disposition of shares

{kind=link}

A shareholder having an accrued foreign exchange loss on common shares of an FA and an accrued foreign exchange gain on a related party debt used...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | loss preservation transactions which did not satisfy the s. 93(2.01) requirements | 205 |

| Tax Topics - Income Tax Act - Section 93 - Subsection 93(2.01) | loss preservation transactions which did not satisfy the s. 93(2.01) requirements | 227 |

7 October 2011 APFF Roundtable Q. 17, 2011-0412171C6 F - 112(7) - Share-for-Share Exchange - 85(1)

Where there is an exchange of 100 common shares in the capital of a corporation for 100 "new" common shares in its capital, there could be...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | purported dirty s. 85 exchange of old common shares for new common shares does "not necessarily" entail a disposition | 49 |

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) | potentially no disposition if "new" share rights identical | 50 |

| Tax Topics - Income Tax Act - Section 112 - Subsection 112(7) | s. 112(7) does not “technically” apply to a dirty s. 85 exchange of old shares for new shares | 257 |

10 July 2007 External T.I. 2006-0177881E5 F - Allégement transitoire

The 1995 transitional relief was available for preferred shares that were acquired after April 27, 1995 in a s. 85(1) exchange for grandfathered...

7 January 2004 External T.I. 2003-0032501E5 F - Transitional Rules/Allègement transitoire

Mr. A, who had held all the shares of HoldcoA on April 26, 1995 at which time HoldcoA held a policy on the life of A whose purpose was to fund the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Transitional Provisions and Policies | taxpayer could choose whether a disposition came out of a pool of grandfathered or non-grandfathered shares | 101 |

21 June 2001 External T.I. 2001-0086285 F - Disposition transitoire à 112(3)

Prior to April 26, 1995, Opco purchased a life insurance policy on the life of Mr. X with coverage of $100,000. On April 26, 1995, Mr. X held...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Share | condition re financing the redemption of a preferred share included part of a preferred share | 37 |

| Tax Topics - General Concepts - Transitional Provisions and Policies | transitional provision re “share” to be applied on a share-by-share basis | 29 |

16 June 2000 External T.I. 1999-0009945 F - Pertes droits acquis et actionnaire uniq

An individual held on April 26th, 1965, and continues to hold, all the outstanding shares of Holdco. One of the subsidiaries (Subco) of Holdco, is...

5 November 1999 External T.I. 9828125 F - RÈGLE TRANSITOIRE - 112(3)

An individual, Mr. X, owned the preferred shares of HoldcoA, whose common shares were held by a trust for the benefit of his children. HoldcoA...

11 October 1996 APFF Roundtable, 7M12910 - APFF ROUND TABLE

Because most transactions contemplated in s. 85.1 (unlike those contemplated in s. 85) significantly change the taxpayer's participation in...

Articles

Didier Fréchette, Ryan Rabinovitch, "Current Issues Involving Foreign Exchange", 2015 CTF Annual Conference paper

Streaming of dividends on preferred shares for loss-shifting rather than 112(3) avoidance reasons (p. 26:50)

A similar issue [to the avoidance of...

Paragraph 112(3)(b)

Subparagraph 112(3)(b)(i)

Administrative Policy

27 November 2018 CTF Roundtable Q. 2, 2018-0780071C6 - Impact of 55(2) deeming rules

After describing the stop-loss rule in s. 112(3), CRA stated:

Denying a loss on a share that is caused by a dividend that has been subject to tax...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 52 - Subsection 52(2) | property dividended has cost equal to FMV where subject to s. 55(2) | 104 |

| Tax Topics - Income Tax Act - Section 52 - Subsection 52(3) | cost under s. 52(3) for stock dividend amount to which s. 55(2) applied | 69 |

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(1) - Paragraph 53(1)(b) - Subparagraph 53(1)(b)(ii) | no basis reduction for s. 84(1) dividend to which s. 55(2) applied | 161 |

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Capital Dividend Account - Paragraph (a) - Subparagraph (a)(i) | 53(1)(b)(ii) and 52(3)(a) exclusion limited to where 55(2) did not apply to the stock dividend or PUC increase | 70 |

Subsection 112(3.1)

Cases

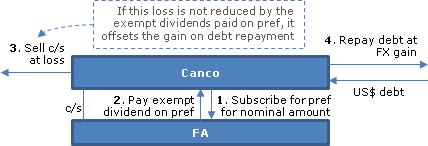

Canada v. Bank of Montreal, 2020 FCA 82

On unwinding a tower structure, a Nevada subsidiary LP of BMO realized FX gains on repaying U.S.-dollar borrowings, but completely offset that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(2) | former s. 39(2) extended to FX gains on s. 39(1) dispositions | 495 |

| Tax Topics - Statutory Interpretation - Interpretation/Definition Provisions | deeming provision applied to all provisions of the Act where it was not explicitly limited | 396 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Tax Benefit | no tax benefit as structuring was unnecessary | 144 |

Subsection 112(3.2) - Loss on share held by trust

Administrative Policy

16 June 2014 STEP Roundtable, 2014-0523061C6 - Trust audit issues

2009-031060117 concerned the redemption of common shares held by an estate in its first year, with the aggregate capital loss realized carried...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(21) | capital gain distributed to different beneficiary | 137 |

| Tax Topics - Income Tax Act - Section 105 - Subsection 105(1) | benefit conferred when trust shares redeemed at undervalue | 196 |

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(1) - Total Charitable Gifts | executors lacked power to make gift | 92 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Legal and other Professional Fees | legal and accounting expenses | 45 |

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | settlor taking back undervalued freeze shares | 76 |

23 September 2004 External T.I. 2004-0088801E5 F - Stop-Loss Provisions -- Grandfathering

Common shares of a corporation had been held by an individual continuously from April 26, 1995 onwards, and satisfied all the conditions for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(5) - Paragraph 248(5)(b) | s. 248(5)(b) does not deem the substituted shares to have been owned for so long as were the underlying shares | 62 |

4 August 1999 External T.I. 9908235 F - PARAGRAPHE 112(3.2) - REGLE TRANSITOIRE

Did correspondence between the insurance company and the beneficiary of the life insurance policy specifying that the policy was taken out to fund...

1996 Ontario Tax Conference Round Table under "S.112 Stop-Loss Amendments, Q. 1 to 4", 1997 Canadian Tax Journal , at pp. 215-218

Discussion of anomaly in s. 112(3.2) and of grandfathering rules.

Articles

Elie Roth, Tim Youdan, Chris Anderson, Kim Brown, "Taxation of Trusts Resident in Canada", Chapter 3 of Canadian Taxation of Trusts, (Canadian Tax Foundation), 2016.

No s. 112(3.2) stop loss for s. 84.1 capital dividend (p. 140)

[T]he CRA has indicated in other contexts that a dividend deemed to be paid under...

Kevin Wark, "Corporate-Owned Insurance: Revisiting Share Redemption Arrangements", CALU Report, August 2004.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(3.6) | 0 |

Joel Cuperfain, "Got Me Those 'Low Capital Gain, High Dividend Tax, Stop-Loss Rules, Estate Planning' Blues", Personal Tax Planning, 2002 Canadian Tax Journal, Vol. 49, No. 3, p. 764.

Jack Bernstein, "Don't Waste Capital Dividends", Canadian Tax Highlights, Vol. 8, No. 9, 26 September 2000, p.71.

Paragraph 112(3.2)(a)

Administrative Policy

5 March 2010 Internal T.I. 2009-0346261I7 F - Minimisation des pertes

When asked for an overview of the distinctions between ss. 112(3.2)(a)(ii)(A), (B) and (C), the Directorate stated:

[F]or the purposes of clause...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 112 - Subsection 112(3.2) - Paragraph 112(3.2)(b) | a testamentary trust can qualify as an estate beneficiary for s. 112(3.2)(b) purposes | 208 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(2) | the trust and trustees both considered to be an individual respecting the corpus and thus to own it | 249 |

Subparagraph 112(3.2)(a)(iii)

Articles

Henry Shew, "Illustrating the Effects of the One-Third Solution on a Subsection 164(6) Redemption", Tax for the Owner-Manager, Vol 24, No. 4, October 2024, p. 1

Discussion of the impact of changing the s. 112(3.2)(a)(iii) limit for the deemed dividend elected as a capital dividend from 50% to 33 1.3% of...

Paragraph 112(3.2)(b)

Administrative Policy

5 March 2010 Internal T.I. 2009-0346261I7 F - Minimisation des pertes

The residue of the estate of Mr. X, which was left in equal parts to four trusts for each of his four children, included Class D preferred shares...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 112 - Subsection 112(3.2) - Paragraph 112(3.2)(a) | respective purviews of ss. 112(3.2)(a)(ii)(A), (B) or (C) | 118 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(2) | the trust and trustees both considered to be an individual respecting the corpus and thus to own it | 249 |

Subsectiom 112(3.32)

Administrative Policy

29 May 2018 STEP Roundtable Q. 15, 2018-0744151C6 - 164(6) and 112(3.2)(b)

The will of the deceased created an estate under which amounts are to be paid to a spousal trust. That trust may, in turn, pay amounts to...

9 August 1999 External T.I. 9915645 F - PARAGRAPHES 104(13.1) ET 112(3.2)

The Directorate concluded inter alia that:

[I]f [a] trust has designated a dividend under subsection 104(13.1), the provisions of subsection...

Subsection 112(4) - Loss on share that is not capital property

Administrative Policy

7 April 1993 Memorandum (Tax Window, No. 31, p. 6, ¶2513)

A standard distress preferred share ruling is that s. 112(4) will not apply in respect of any dividends received by the specified financial...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | 45 | |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(p) - Subparagraph 20(1)(p)(ii) | 65 |

91 C.R. - Q.34

Re interaction between ss.112(4) and (4.1).

19 November 1990 Memorandum (Tax Window, Prelim. No. 2, p. 18, ¶1041)

Discussion of a situation which s. 112(4)(e) was intended to cure.

Subsection 112(4.1) - Fair market value of shares held as inventory

Administrative Policy

1995 T.E.I. Round Table, Q. 18, 953112 (C.T.O. "Dividends on Shares Held as Inventory")

A taxpayer who has chosen pursuant to Regulation 1801 to value all its inventory at fair market value will recognize a gain where the deemed fair...

Subsection 112(5.2)

Articles

Kevin Kelly, Sona Dhawan, "Share Repurchase Programs", Canadian Tax Highlights, Vol. 26, No. 6, June 2018, p. 9

Share repurchase programs under private agreements (SRPs) for shares eligible under a normal-course issuer bid (p. 9)

[I]n January 2018, six...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | reliance on exclusion of deemed dividend from proceeds of mark-to-market shares to generate artificial loss | 185 |

Variable B

Administrative Policy

21 May 2003 Internal T.I. 2003-0009897 F - COUT DES ACTIONS

The Directorate confirmed that “the amount for Variable B in subsection 112(5.2) represents the loss on the disposition of the share that is...

21 May 2002 External T.I. 2002-0133105 F - COUT DES ACTIONS

In finding that s. 47(1) does not apply to determine the loss on shares that are mark-to-market property for the purposes of the description of B...

Subsection 112(7)

Administrative Policy

7 October 2011 APFF Roundtable Q. 17, 2011-0412171C6 F - 112(7) - Share-for-Share Exchange - 85(1)

Holdco received $500,000 in dividends on its common shares of Opco (generating s. 112(1) deductions and then some years later, transferred those...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 112 - Subsection 112(3) | s. 112(3) could still apply if "old" dividend-bearing shares "exchanged" under purported s. 85(1) exchange for "new" but identical shares | 98 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | purported dirty s. 85 exchange of old common shares for new common shares does "not necessarily" entail a disposition | 49 |

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) | potentially no disposition if "new" share rights identical | 50 |

Subsection 112(8)

Subsection 112(9)

Administrative Policy

Edward Miller and Matias Milet, "Derivative Forward Agreements and Synthetic Disposition Arrangements", 2013 Conference Report, (Canadian Tax Foundation), pp.10:1-50

Example of interaction between ss. 112(9) and (8) (p.10:42)

[S]ubsection 112(9) expressly provides that the 365 day period is determined without...

Articles

Raj Juneja, "Taxation of equity derivatives", 2015 CTF Annual Conference paper

Deemed non-ownership under SDA for stop-loss purposes (p. 17:14)

An additional rule in subsections 112(8) and (9) also applies where the...

Subsection 112(10)

Articles

Raj Juneja, "Taxation of equity derivatives", 2015 CTF Annual Conference paper

Ordering rule limiting access to 365-day stop-loss exception (p.17:14)

[A] specific ordering rule will be included in subsection 112(10), which...