Cases

Canada v. Hutchison Whampoa Luxembourg Holdings S.À R.L., 2025 FCA 176, aff'g sub nom. Husky Energy Inc. v. The King, 2023 TCC 167

Before a Canadian public corporation (“Husky”) paid a dividend on its shares, two significant shareholders of Husky resident in Barbados (the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(2) | Tax Court finding that the recipient of a dividend for s. 212(2) purposes was other than the dividend’s beneficial owner was potentially troubling | 222 |

| Tax Topics - General Concepts - Substance | agreements styled as securities lending agreements were not such in their legal substance | 202 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(1) | CRA assessments of dividend payer under s. 215(6) and “protective assessments” of dividend recipients under s. 212(2) were “troubling” in light of Galway principle | 239 |

| Tax Topics - Income Tax Act - Section 215 - Subsection 215(6) | CRA decisions to make “protective assessments” of the dividend recipients under s. 212(2) in addition to assessing the dividend payers under s. 215(6) was troubling under Galway | 98 |

Canada v. Prévost Car Inc., 2009 DTC 5721, 2009 FCA 57

The taxpayer paid dividends to its shareholder, ("Prévost Holding"), a Netherlands holding company which, in turn, paid dividends in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions | 76 |

Hunter Douglas Ltd. v. The Queen, 79 DTC 5340, [1979] CTC 424 (FCTD)

A Canadian company shifted its central management and control to the Netherlands, thereby becoming a resident of the Netherlands for purposes of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions | 49 |

See Also

Methanex Trinidad (Titan) Unlimited v The Board of Inland Revenue (Trinidad and Tobago), [2025] UKPC 20

The appellant (Methanex Trinidad) paid U.S.$85.4 million in dividends to its Barbados parent (Methanex Barbados), which promptly paid dividends to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 4 | a Barbados IBC was a resident of Barbados for general treaty purposes | 295 |

Husky Energy Inc. v. The King, 2023 TCC 167, aff'd sub nomine Hutchison Whampoa Luxembourg Holdings S.À R.L. 2025 FCA 176

Before a Canadian public corporation (“Husky”) paid a dividend on its shares, two significant shareholders of Husky resident in Barbados (the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(2) | tax under s. 212(2) imposed on the basis of payment of dividend to a non-resident rather than on the basis of who is the beneficial owner | 405 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Tax Benefit | no tax benefit under s. 215(6) from targeted reduced rate of dividend withholding if in base transaction, the Canadian dividend payer would have withheld at the higher rate | 347 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | the residence, beneficial owner, and voting requirements in the Canada-Luxembourg Treaty fully expressed the rationale for the 5% Treaty-reduced rate on dividends | 413 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | transactions were carried out to reduce Part XIII tax rather than avoid Barbados income tax | 131 |

RMM Canadian Enterprises Inc. v. R., 97 DTC 302, [1998] 1 C.T.C. 2300 (TCC)

After finding that sale proceeds was deemed to be a dividend by s. 84(2), Bowman TCJ. went on to find that this deemed dividend was a dividend for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 159 - Subsection 159(3) | 167 | |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | 188 | |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 235 | |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | purchaser of cash-rich company without any signifcant separate role did not deal at arm's length | 177 |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | application of s. 84(2) to sale of cash-rich company to accommodation party who quickly paid cash proceeds therefor | 222 |

| Tax Topics - Treaties - Income Tax Conventions | 96 |

Specialty Manufacturing Ltd. v. R., 97 DTC 1511, [1998] 1 CTC 2095 (TCC)

Article IX of the 1980 Canada-U.S. Convention and Article IV of the 1942 Canada-U.S. Convention did not prevent the application of s. 18(4) of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(4) | 54 |

Administrative Policy

6 September 2024 External T.I. 2019-0796831E5 - Part XIII Tax on Dividend Paid to a Partnership

Canco was wholly owned by a general partnership governed by US laws (USP) between a U.S. corporation owned by U.S. residents (Partner1) and a...

15 May 2024 IFA Roundtable Q. 7, 2024-1007641C6 - Principal Purpose Test in the Multilateral Instrument

CRA was asked how the principal purpose test (PPT) in Art. 7(1) of the MLI) would apply in the situation where:

Canco is wholly-owned by a Foreign...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Multilateral Instrument - Article 7 - Article 7(1) | PPT application to a treaty-reduced dividends of Canco paid to a pure Holdco with an ultimate Treaty-resident parent | 457 |

15 May 2024 IFA Roundtable Q. 1, 2024-1007651C6 - Principal purpose test and the UK-Canada Tax Treaty

A UK-resident corporation increased its voting shareholding of Canco the day before a dividend was paid so as to hold 10% of the shares. How would...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Multilateral Instrument - Article 7 - Article 7(1) | a non-resident’s increasing its voting shareholding in Canco to access the Treaty-reduced dividend withholding rate likely does not engage the PPT | 233 |

21 October 2021 Internal T.I. 2020-0872281I7 - S.219 and Article X(6) of the Canada-US Treaty

The Directorate confirmed the position in 9408985 that in light of the branch profits limitation under Ar. X(6) of the Canada-US Treaty of 10% of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 219 - Subsection 219(1) | effect on Pt. XIV tax computation of Art. X(6) branch profits limitation | 305 |

14 December 2023 External T.I. 2019-0820291E5 - Meaning of "Capital"

The 1,000 common shares of Canco (a Canadian-resident corporation), which had an aggregate fair market value (FMV) and stated capital of $1,000...

16 June 2020 Internal T.I. 2019-0792651I7 - 10(8) of the Canada-UK Tax Treaty

Art, 10(8) of the Canada-U.K. Convention provides:

The provisions of this Article shall not apply if it was the main purpose or one of the main...

2024 Ruling 2019-0817961R3 - Swiss Collective Investment Scheme

Background/ structure

A collective investment scheme (the “Fund”) established under Swiss law is an arrangement by which investors pool their...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(1) | Swiss collective investment entity treated as a flow-through for Canadian withholding tax purposes | 175 |

17 May 2023 IFA Roundtable Q. 7, 2023-0964521C6 - Application of Article 10, Canada-Hong Kong

Two individuals (Mr. and Mrs. A), who had been resident in Hong Kong from before 2013, each transferred 50% of the shares of a Canadian-resident...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Multilateral Instrument - Article 7 - Article 7(1) | the PPT object and purpose test is met where individuals in a Treaty country transfer their Canco shares to a Treaty-resident Holdco to reduce dividend withholding | 301 |

27 October 2020 CTF Roundtable Q. 5, 2020-0864281C6 - Article IV:6 of the Canada-US Treaty

A partnership whose partners are resident in the U.S. and in other countries with which Canada does and does not have a treaty owns a French...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 4 | where Canco is held by fiscally transparent Franceco, which is held by LP with only some US partners, there is a choice as to which Treaty to apply | 374 |

18 April 2019 Internal T.I. 2018-0753621I7 - Subsection 247(12)

Parentco, a U.S.-resident, is the only member of Parentco LLC, which is the only member of Sisterco LLC, and also wholly-owns Canco. Canco resides...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(12) | transfer pricing income adjustment re sale to NR sister gave rise to taxable dividend | 110 |

| Tax Topics - Treaties - Income Tax Conventions - Article 4 | a s. 247(12) secondary-adjustment deemed dividend paid by Canco to an LLC sister qualified under Art. IV(6) for the 5% Treaty-reduced rate on dividends to its U.S. parent | 498 |

4 April 2019 Internal T.I. 2017-0736531I7 - Articles IV(6) and X(6) of the Canada-US Treaty

Two U.S. corporations that were “qualifying persons” for purposes of the Canada-U.S. Treaty (USCo1 and USCo2) held 58% and 42%, respectively,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 4 | Art. IV(6) of Cda-US Treaty can be satisfied where Canadian branch profits are earned at bottom of stacked LLCs held by qualifying persons | 247 |

7 September 2016 External T.I. 2014-0563781E5 - Articles 10 and 11 of Canada-UK Treaty

A UK corporation (“GP Co”) is the general partner (with a 1% interest) of a UK limited partnership which is fiscally transparent for UK...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 11 | limited partners of an LP can deal at arm’s length with a Canadian subsidiary of the LP | 452 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | limited partners of an LP could deal at arm’s length with a Canadian sub of the LP | 222 |

28 May 2015 IFA Roundtable Q. 12, 2015-0581521C6 - IFA 2015 Q.12: Canada-Switzerland Treaty

A corporation resident in Switzerland ("Swissco") wholly-owns "Holdco," which wholly-owns "Canco"). S. 214(3)(a) deems Canco to pay a dividend to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions | resolution of conflicting French and English Treaty versions of Swiss Treaty in taxpayer's favour | 89 |

28 May 2015 IFA Roundtable Q. 2, 2015-0581551C6 - IFA 2015 Q.2: GAAR and treaty shopping

What is CRA's position on the application of the GAAR to treaty shopping arrangements? CRA stated:

The…comments on treaty shopping… made in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | treaty shopping | 99 |

11 July 2014 External T.I. 2013-0497381E5 - REIT investment in a US IRA.

An IRA account of Mr. X (who is a citizen and a resident of the US) receives a distribution on units held in a REIT as defined in s. 122.1(1). ...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 22 | REIT income distributions to IRA at 15% | 222 |

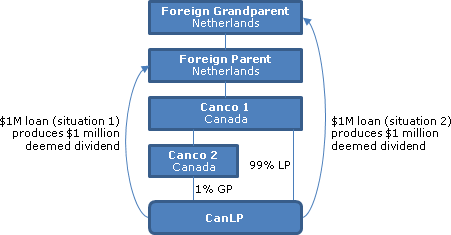

31 May 2013 External T.I. 2013-0486011E5 - Loan to non-resident - Part XIII tax

{kind=link}

A Canadian-resident corporation (CanCo1) and its wholly-owned Canadian-resident subsidiary (CanCo2) are the 99% limited partner and 1% general...

23 October 2012 External T.I. 2012-0440101E5 - Article X(6) Canada-US Treaty

A US LLC, which has two US-resident members (either two corporations or an individual and a corporation) who qualify for Treaty benefits, carries...

17 May 2012 IFA Roundtable, 2012-0444151C6 - Hybrid Partnerships and Branch Tax Liability

The two partners of a partnership which has elected to be a domestic corporation for Code purposes are: a corporation which is resident in the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 29A | 170 |

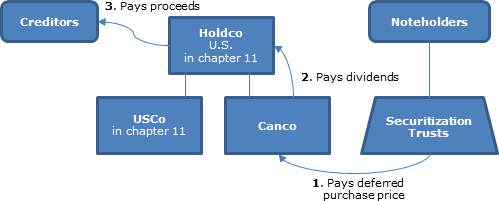

2012 Ruling 2012-0435211R3 - Article XXIX-A(3) of the Canada-US Tax Convention

{kind=link}

Holdco, which had been a listed U.S. company, was taken private by L5, which was a fund whose members are not known. Holdco and its subsidiary,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 29A | US Holdco in Chap. 11 receives dividend | 235 |

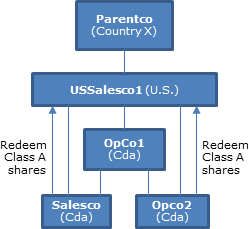

2012 Ruling 2011-0424211R3 - Article X(2) and 84(3) deemed dividends

{kind=link}

All of the Class A shares of two taxable Canadian corporations ("OpCo2" and "Salesco") are owned by a corporation ("USSalesco1") which is not...

Income Tax Technical News No. 44 13 April 2011 [archived]

After commenting on a transaction in which a ULC held by a US C corporation (USco) increases its paid-up capital (giving rise to a deemed...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(1) - Paragraph 111(1)(a) | inter-provincial loss shifting | 69 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(e) | exchangeable debenture appreciation not recognized | 102 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(f) | exchangeable debenture appreciation not recognized | 120 |

| Tax Topics - Income Tax Act - Section 49 - Subsection 49(1) | exchangeable debenture exercise | 90 |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(c) | FMV basis in contributed property | 72 |

30 November 2010 Annual CTF Roundtable, 2010-0386391C6 - Branch Tax

In response to a query as to whether the branch tax reduction in Art. X(6) of the Canada-US Tax Convention is available to a fiscally transparent...

13 July 2009 External T.I. 2009-0318701E5 - Article X(2) and Tiered Partnerships

Where a US corporation that is a qualifying person is a 99.99% limited partner of a Delaware limited partnership which, in turn, is a 99.99%...

21 May 2009 IFA Roundtable Q. 1, 2009-0321451C6 - Meaning of beneficial owner in Article 10, 11 & 12

In the Prévost Car case, "the Court implied that where an intermediary acts as a mere conduit or funnel in respect of an item of income, the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 11 | 84 |

2007 Ruling 2007-0248021R3 - Cdn Japan Convention: withholding rate deemed div.

a dividend deemed to be received by significant Japanese corporate shareholder of a Canadian corporation under s. 84(3) on the purchase for...

2004 IFA Roundtable Q. 3, 2004-007223

Although a partner is not considered to own a specified percentage of the shares of a corporation held by a partnership, a favourable ruling was...

12 March 2003 External T.I. 2002-0176955 F - Retenu dividende français

CCRA indicated, regarding whether a dividend paid by a French corporation to a Canadian mutual fund trust or Canadian pension fund would be...

17 December 2002 External T.I. 2002-0155005 - FTC for U.K. Dividends

Following the repeal of U.K. ACT in 1999, paragraph 3 of the Canada-U.K. Convention continues to apply since individuals in the United Kingdom are...

18 March 2002 External T.I. 2002-0120065 F - Avoir fiscal français - 20(11)

A Canadian-resident received a $10,000 dividend from a French company as reduced by French withholding tax of 15% ($1,500) and by the 50% avoir...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(1) | French avoir fiscal did not reduce the dividend from a French company required to be included in the resident individual shareholder’s income | 92 |

30 January 2002 External T.I. 2001-0106695 - Subs. 219(5.3);Article X of Canada-US Treaty

A deemed dividend under s. 219(5.3) of the Act will be treated as a dividend governed by Article X, paragraph 2 of the Canada-U.S. Convention,...

8 January 1996 External T.I. 9428025 - RETURN OF CAPITAL FROM A DELAWARE CORPORATION

Because the purpose of the "source country deemed dividend rule" in the definition of "dividend" in paragraph 3 of Article X of the Canada-U.S....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(1) | all distributions from Delaware corps are dividends | 92 |

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(3) | all distributions from Delaware corps are dividends | 92 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Dividend | 92 |

4 March 1993 Memorandum (Tax Window, No. 30, p. 18, ¶2472)

A Canadian resident will not be entitled to a foreign tax credit or to a refund of ACT from the U.K. authorities with respect to a stock dividend...

October 1992 T.I. 921009 "Loans to Non-Residents"

Where a Canadian subsidiary issues a demand note to its U.S. parent, the deemed dividend arising under s. 214(3)(a) will be eligible for the...

3 September 1992 T.I. 920333 "Interest-Free Loans - Reason for Withholding"

The word dividend in the Canada U.S.-Convention includes deemed dividends arising under s. 214(3)(a) of the Act.

8 April 1992 T.I. (913412 (March 1993 Access Letter, p. 83, ¶C180-135; Tax Window, No. 18, p. 10, ¶1847)

Where s. 214(3)(a) imputes a shareholder benefit to U.S. resident shareholders of a U.S. corporation which allows them to use a Canadian vacation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | 28 |

91 C.R. - Q.1

A U.S. corporation holding shares through a U.S. partnership will not be eligible for the 10% rate.

Articles

Peter Lee, Paul Stepak, "PE Investments in Canadian Companies", draft 2017 CTF Annual Conference paper

Application of 10%-of-voting power test where sister companies held through holding “Aggregator” LP (pp. 5, 9)

[A] PE fund limited partnership...

Elio Andrea Palmitessa, "Italian Supreme Court Applies the Beneficial Ownership Clause to Pure Holding Companies", Tax Notes International, April 17, 2017, p. 259

Dividend withholding avoidance (p. 259)

[A] U.S. corporation owned a holding company in France, which in turn owned an Italian subsidiary. In 2002...

Timothy Hughes, Matias Milet, Marc Richardson-Arnould, "Private Equity Funds – Selected Canadian Tax Issues", Tax Management International Journal, 2016, p.84

Advantages of separate fund for Canadian investors (p. 87)

A non-Canadian private equity fund that expects to have significant investor capital...

Jack Bernstein, "Canada-US Tax Traps for LLCs", Canadian Tax Highlights, Volume 22, Number 2, February 2014, p. 11

High US branch tax if use LLC (p.11)

Assume that a Canco expands into the United States and forms an LLC to be the US opco. For Canadian tax...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 126 - Subsection 126(1) | 149 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 4 | 150 |