See Also

Commissioner of Taxation v. Resource Capital Fund III LP, [2014] FCAFC 37 (Fed. Ct. of Austr.)

The appellant ("RCF") was a non-Australian partnership which was assessed on the basis that its gain from the sale of a "member ship interest" in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Other | mining information not to be valued separately at reproduction cost | 296 |

| Tax Topics - Treaties - Income Tax Conventions - Article 13 | mining information not to be valued separately at reproduction cost | 296 |

| Tax Topics - Treaties - Income Tax Conventions - Article 4 | reverse hybrid partnership | 431 |

Lipson v. The Queen, 2012 DTC 1064 [at at 2796], 2012 TCC 20

The taxpayers received a number of capital distributions from the liquidator of their mother's "succession" (a Quebec estate), but only filed a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(1) | Quebec succession not a trust | 271 |

| Tax Topics - Income Tax Act - Section 116 - Subsection 116(3) | 184 |

Administrative Policy

1 May 1990 Memorandum AC70442

"With respect to the application of the provisions of section 116 of the Act to the disposition of partnership property, (i) the assumptions in...

84 C.R. - Q.36

S.116 has no application to dispositions of Canadian real estate that constitutes inventory to the non-resident investor.

Articles

Edward A. Heakes, "Another Wave of Foreign Affiliate Proposals", International Tax Planning, Volume XVIII, No. 4, 2013, p. 1275

De minimis partnership interests are included in test (p. 1276

[I]f a taxpayer holds 5% of the shares of a listed company and is a partner in a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(8.3) | 110 | |

| Tax Topics - Income Tax Act - Section 91 - Subsection 91(1.2) | 90 |

Steve Suarez, Maire-Eve Gosselin, "Canada's Section 116 System for Nonresident Vendors of Taxable Canadian Property", Tax Notes International,9 April 2012, p. 175

Includes discussion of change in CRA policy (net to gross asset value) re determination of whether shares derive their value primarily from real...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 116 - Subsection 116(1) | 9 | |

| Tax Topics - Income Tax Act - Section 116 - Subsection 116(5.01) | 9 |

Michael N. Kandev, Fred Purkey, "Practical Troubles With the Disposition of Canadian-Situs Property by Nonresidents of Canada", Practitioner's Corner, Tax Notes International, 12 September 2011, p. 807.

David W. Ross, "Non-Resident Unitholders - Impact on Status", Resource Sector Taxation, 2004, p. 76: Discussion whether net profit interests are interests in respect of real property.

Paragraph (a)

Administrative Policy

26 May 2022 External T.I. 2019-0813761E5 - Taxable Canadian property-solar and wind projects

Canadian-managed funds purchased from time to time, from non-residents, Canadian-situs solar electric power generating projects (consisting of a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Real Property - Paragraph (a) | solar equipment assembly was a fixture under the common law tests | 551 |

22 June 2001 Internal T.I. 2001-0078457 F - Décret remise d'impôt revenu gagné au Québec

A non-resident inherited a royalty entitlement to a percentage of the net proceeds of sales from a Quebec gold mine, and then sold the royalty to...

Articles

Michel Ranger, Rhonda Rudick, "Federal and Provincial Tax Considerations Relating to Non-Resident Investment in Canadian Real Estate", 2019 Conference Report (Canadian Tax Foundation), 32:1 – 39

Quebec taxation of income from specified immovable property

[N[on-resident inter vivos trusts that own immovable property in Quebec and that earn...

Paragraph (b)

Administrative Policy

19 June 2015 STEP Roundtable, Q. 10

A testator dies leaving an estate comprised mostly of real property situated in Canada (a principal residence). Upon completion of the estate...

27 June 2013 External T.I. 2012-0459481E5 - Taxation of a Non-Resident

In response to a query as to whether precious metal coins stored in Canada on behalf of a non-resident individual would be taxable Canadian...

7 July 2011 External T.I. 2011-0403271E5 - Non-resident's taxable income in Canada

Gold bullion situated in Canada owned by a non-resident is not taxable Canadian property provided that it is not part of the inventory of a...

92 C.M.TC - Q.6

It is essentially a question of fact whether a ship used in international shipping constitutes taxable Canadian property.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 81 - Subsection 81(1) - Paragraph 81(1)(c) | 21 |

Paragraph (c)

Articles

Michel Ranger, Rhonda Rudick, "Federal and Provincial Tax Considerations Relating to Non-Resident Investment in Canadian Real Estate", 2019 Conference Report (Canadian Tax Foundation), 32:1 – 39

ARQ position that shares with no connection to Quebec can be taxable Quebec property (pp. 32:20-21)

[I]n certain circumstances shares of a...

Paragraph (d)

See Also

Commissioner of Taxation v Resource Capital Fund IV LP Commissioner of Taxation v Resource Capital Fund IV LP, [2019] FCAFC 51

Two Caymans investment LPs (“RCF IV” and RCF V”) whose limited partners were mostly U.S. residents, realized gains from the disposal of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(1) | assessment must bring to the attention of the assessed person that it has been assessed to tax | 258 |

| Tax Topics - Income Tax Act - Section 115 - Subsection 115(1) - Paragraph 115(1)(a) - Subparagraph 115(1)(a)(ii) | source of gain was in Australia because the sale occurred pursuant to an Australian Scheme of Arrangement | 320 |

Resource Capital Fund IV LP v Commissioner of Taxation, [2018] FCA 41 (Federal Court of Australia), rev'd on various grounds [2019] FCAFC 51

Two Caymans investment LPs (“RCF IV” and RCF V”) whose limited partners were mostly U.S. residents, realized gains from the disposal of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Shares | private equity fund LP with 5-year holding objective realized share gain on income account | 175 |

| Tax Topics - Income Tax Act - Section 115 - Subsection 115(1) - Paragraph 115(1)(a) - Subparagraph 115(1)(a)(ii) | gains of a NR PE fund from disposals of Australian share investments that were managed in part in Australia were derived from Australia | 427 |

| Tax Topics - Treaties - Income Tax Conventions - Article 3 | each U.S.-resident partner of a Caymans PE LP carried on a U.S. “enterprise” | 234 |

| Tax Topics - Treaties - Income Tax Conventions - Article 13 | exclusion in Art. 13 of Aust.-U.S. Treaty for real property dispositions extended to shares of Australian holding company holding mining leases through grandchild | 420 |

| Tax Topics - General Concepts - Stare Decisis | lower court not bound by a point of law that was assumed rather than examined by a higher court | 292 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(1) | assessment of partnership was assessment of partners | 89 |

| Tax Topics - Treaties - Income Tax Conventions - Article 6 | Art. 6 extends common law meaning of real property | 198 |

| Tax Topics - Income Tax Act - Section 218.3 - Subsection 218.3(1) - Canadian Property Mutual Fund Investment | shares of Australian mining company were primarily attributable to the processing rather than mining operations | 142 |

| Tax Topics - General Concepts - Fair Market Value - Other | processing assets of mining company were more valuable than its mining assets | 238 |

Administrative Policy

22 September 2017 External T.I. 2016-0668041E5 - TCP and Article 13(5) of Canada-UK Treaty

A Netherlands company (“BVCo”) wholly-owns:

- All the shares, with a fair market value (“FMV”) of $1M, of a Canadian subsidiary...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 13 | proportionate value approach to determining whether shares of a foreign holding company are derived more than 50% from Canadian immovable property for Treaty purposes | 298 |

1 May 2017 Internal T.I. 2015-0624511I7 - 248(1)(e)(ii) of the definition of TCP

A non-resident trust (the “Trust”) took the position that its shares of various private non-resident corporations (“NRCos”) were not...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 94 - Subsection 94(3) - Paaragraph 94(3)(c) | methodology for determining whether shares of NR corps indirectly holding some Cdn real property and resource properties through Opcos with interco loans were taxable Cdn property | 319 |

1 March 2017 External T.I. 2016-0658431E5 - Article XIII of Canada-U.S. Convention

The question of whether a share or trust interest derives its value from Canadian real property for purposes of the Canada-U.S. Treaty is a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 13 | test of a real property security under the Canada-U.S. Treaty is a point-in-time test | 276 |

6 December 2016 External T.I. 2014-0542551E5 - Taxable Canadian Property

A Canadian resident individual (the “Taxpayer”) sold a principal residence and invested the proceeds in shares of publicly traded corporations...

2012 IFA Roundtable, Q.5 [preliminary -final above]

In determining whether the shares of of a Canadian corporation (Canco 1) are taxable Canadian property, CRA will apply a proportionate value...

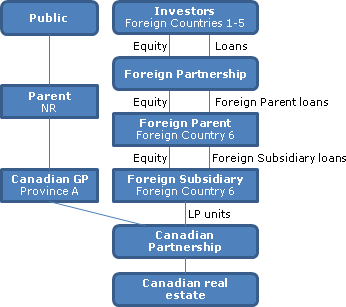

2013 Ruling 2012-0444431R3 - Taxable Canadian Property

{kind=link}

A partnership (Foreign Partnership), whose non-resident members (Investors) are resident in Foreign Countries 1 through 5, uses a portion of its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 13 | NR partnership holding real property interests through debt | 301 |

13 September 2012 CICA Compliance Roundtable, 2012-0453021C6 - Taxable Canadian Property

Respecting a question as to whether shares of an unlisted corporation would be taxable Canadian property if during the preceding 60 months "most...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(4) | non-defaulted mortgage is not an interest in real property | 222 |

17 May 2012 IFA Conference Roundtable, 2012-0444091C6 - Definition of taxable Canadian property

In determining (when a non-resident disposes of shares of Parent) what portion of the shares of the Subsidiary of Parent represent real or...

28 November 2011 CTF Roundtable, 2011-0425901C6 - Does share derive value principally from real prop

In response to a question as to how the 50%-derived-from-real-property test should be applied where the non-resident disposes of shares of Parent...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 13 | whether shares derive their value from real property is determined irrespective of debt allocation | 135 |

Articles

Jin Wen, "TCP and Intercompany Loans", Tax for the Owner-Manager, Vol. 20, No. 2, p. 9

- 2015-0624511I7 and 2012-0444091C6 indicate that that indebtedness between a parent and a wholly owned subsidiary has no impact on the...

John Tobin, "Infrastructure and P3 Projects", 2017 Conference Report (Canadian Tax Foundation), 10:1-31

TCP status on loans to P3 Projecto LP potentially avoided if partners of non-resident collective investment vehicle partnership lend directly to...

Jared A. Mackey, "Canada Revenue Agency Views on Taxable Canadian Property Determinations Involving Subsidiaries", Tax Topics (Wolters Kluwer), No. 2315, July 21, 2016 p. 1

Proportionate value approach to determining what portion of equity is Canadian real/resource property (“CRP”) (p. 2)

If a subsidiary's shares...

Timothy Hughes, Matias Milet, Marc Richardson-Arnould, "Private Equity Funds – Selected Canadian Tax Issues", Tax Management International Journal, 2016, p.84

Goodwill fluctuations relative to real estate may potentially taint private equity investments (p. 86)

Private equity funds currently invest...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 115.2 - Subsection 115.2(2) - Paragraph 115.2(2)(b) | 201 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 10 | 389 |

Sheryl Troup, "Purchasing Private Corporation Shares: Hazards if the Vendor is Non-Resident", Canadian Tax Focus, Volume 3, No. 4, November 2013, p. 5.

Gross v. net asset method (p.5)

At a CRA and Revenue Québec round table published in the Canadian Tax Foundation's 2011 Conference Report, the...

Paragraph (e)

Administrative Policy

19 March 2013 Internal T.I. 2010-0385931I7 - Taxable Canadian property and Partnerships

A partnership is disposing of its 25% shareholding of a listed public corporation ("Pubco"). Those shares derived more than 50% of their fair...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 116 - Subsection 116(1) | partnership look-through | 278 |

| Tax Topics - Income Tax Act - Section 96 - Subsection 96(1) - Paragraph 96(1)(f) | partnership TCP gain but not TCP status attributed to partners | 88 |

29 November 2011 November CTF Roundtable, 2011-0425931C6 - 2011 CTF - Question 20

CRA confirmed that:

when determining whether a share listed on a designated stock exchange is TCP at "any particular time" during a 60 month...

Articles

Jack Bernstein, Francesco Gucciardo, "TCP Proposal Overshoots Objective?", Canadian Tax Highlights, Vol. 21, No. 8, p. 4

The authors provided the following example showing that a small direct holding of shares of a Canco could become taxable Canadian property under...

Paragraph (f)

Administrative Policy

7 March 2016 External T.I. 2015-0608211E5 - Assignment of right to purchase

Would an assignment to a trust by a non-resident person of a right to purchase a Canadian apartment unit be considered a disposition of taxable...

18 December 2002 External T.I. 2002-0151795 - Options and Taxable Canadian Property

In light of the repeal of s. 115(3), a taxpayer who owns directly 20% of the shares of a listed corporation and has an option to acquire an...

91 C.R. - Q.49

RC treats options to acquire property as described in s. 115(1)(b)(iv) held by non-resident persons, or persons with whom they did not deal at...