Paragraph 55(3.1)(a)

Administrative Policy

2023 Ruling 2022-0958241R3 - Public Spin-Off Butterfly

CRA ruled on a butterfly spin-off by a listed Canadian corporation (DC) of its indirect interest in a foreign project to a “SpinCo” to be held...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.02) | public company spin-off with s. 51 reversal of new s. 86 common shares | 948 |

| Tax Topics - Income Tax Act - Section 86 - Subsection 86(1) | new common shares created on s. 86 reorg then immediately converted under s. 51 back to old common shares | 124 |

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Public Corporation - Paragraph (b) | public spinco to elect effective before its shares were listed | 84 |

| Tax Topics - General Concepts - Fair Market Value - Shares | FMV of listed shares based on their 5-day VWAP pre-spin-off or post spin-off | 173 |

2017 Ruling 2016-0674681R3 - Sequential Split-Up Butterfly

Preliminarily to a butterfly distribution that was favourably ruled upon, DC1 sold portfolio investment units for cash, and may reinvest the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | sequential split-up butterfly with 1% tolerance, triggering of capital gains to generate CDA and RDTOH, and year end change to accommodate RDTOH division | 747 |

| Tax Topics - Income Tax Act - Section 129 - Subsection 129(1) | capital gain deliberately triggered to generate CDA and RDTOH addition and year end change granted to isolate dividend refund | 543 |

| Tax Topics - Income Tax Act - Section 249.1 - Subsection 249.1(7) | CRA accommodates year end change so that dividend refund of full RDTOH balance is generated in Year 1 | 210 |

2014 Ruling 2014-0528291R3 - Butterfly Reorganization

DC was not controlled by either of its two shareholders (WCo and SCo). Prior to a butterfly transfer to Newco, formed by SCo, DC will proceed with...

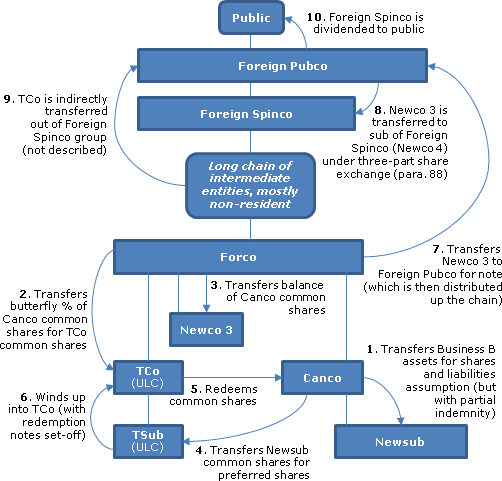

2013 Ruling 2013-0491651R3 - Cross-Border Butterfly

Background

Foreign PubCo will spin-off Foreign SpinCo to its shareholders. Foreign SpinCo is a great-grandchild subsidiary held by it "through"...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | cross-border b/f with 3-party exchange, cash-out of ineligible shareholders, proportionate allocation of foreign spinco debt, pension liability classification, prelim non-series dividend | 1011 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.1) - Paragraph 55(3.1)(b) - Subparagraph 55(3.1)(b)(i) | cross-border b/f with 3-party exchange, pro rata application of upper tier debt, cash-out of ineligible shareholders | 501 |

| Tax Topics - Income Tax Act - Section 86 - Subsection 86(1) | exchange for substantively identical common shares | 124 |

7 October 2011 Roundtable, 2011-0399401C6 - Butterfly, life insurance policies, grandfathering

Two siblings are the shareholders of two transferee corporations which are to receive two life insurance policies taken out by the distributing...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | CSV of life insurance policy was a cash asset - FMV excess could be an investment asset if no cash-out intention | 212 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(4) | s. 55(4) inapplicable if the principal reason for parent’s control of DC was parent's economic interests | 178 |

2000 Ruling 1999-0010723 - sequential butterfly reorganizations

A reallocation of mortgage balances in respect of two of the properties to be transferred would result in an acquisition of property by the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Other | 35 |

Income Tax Technical News, No. 16, 18 December 1998

discussion whether Parthenon would indicate that a distributing corporation would not be considered to control its subsidiaries if ultimate...

14 June 1996 CTF Roundtable Q. 18, 9620790 - PRE-BUTTERFLY TRANSACTIONS

"Where the butterfly is being carried out on a 'net equity' basis, the repayment of a debt (whether owing to a third party or a shareholder)...

Income Tax Regulation News, Release No. 3, 30 January 1995 under "Butterfly Reorganizations"

Where in contemplation of a butterfly, a corporation transfers property to a partnership in consideration for a partnership interest, the...

Articles

Marshall Haughey, "Spinoff Butterflies in Trouble?", Canadian Tax Focus, Volume 3, No. 4, November 2013, p. 3.

Exchange of shares to DC on permitted exchange (p. 3)

As a pre-distribution step in a typical spinoff butterfly, shareholders of the distributing...

Firoz Ahmed, "Subsection 55(3) Update", Canadian Current Tax, Vol. 15, No. 8, May 2005, p. 69:

Discussion of effect of contractual agreements on property-becoming-property test in s. 55(3.1)(a).

Vance Sider, "Section 55: Administrative Developments", 1995 Corporate Management Tax Conference Report, c. 8.

Paragraph 55(3.1)(b)

Administrative Policy

22 January 2016 External T.I. 2015-0617601E5 F - Pipeline followed by butterfly

CRA considered transactions in which, during the second year of conventional pipeline transactions, the Newco ("Corporation 2") was split between...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | pipeline transaction can be coupled with a butterfly split-up | 468 |

8 October 2010 Roundtable, 2010-0373211C6 F - Butterfly Transaction - Permitted Exchange

Where after a butterfly transaction, a family trust (whose beneficiaries are persons unrelated to the transferee corporation, the distributing...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Permitted Exchange - Paragraph (b) | issuance of shares by TC after the DC distribution not relevant to there being “permitted exchange” | 214 |

Articles

Christian Desjardins, Nik Diksic, "Cross-Border Butterflies in the Context of Public Spin-Off Transactions", 2015 CTF Annual Conference paper

History of s. 55(3.1)(b) (pp. 29:3)

[The main purpose of the original version of subsection 55(3.1) was to prevent…using the butterfly exemption...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | 1439 |

Subparagraph 55(3.1)(b)(i)

Administrative Policy

2014 Ruling 2014-0530961R3 - Cross-Border Butterfly

In connection with a spin-off by a U.S. public company (Foreign PubCo) of a U.S. subsidiary (Foreign Spinco) to which one of its businesses was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | U.S./Cda b/f including conversion of Foreign Spinco and TC from fiscally disregarded to regarded for Code purposes/2-stage transfer to TC of cash assets/post-b/f dividend by DC/s. 86.1 treatment/proportionate allocation of Foreign Spinco debt | 1479 |

| Tax Topics - Income Tax Act - Section 86.1 - Subsection 86.1(2) | spin-off by U.S. pubco of U.S. spinco after Canadian butterfly | 115 |

2013 Ruling 2013-0491651R3 - Cross-Border Butterfly

{kind=link}

Background

Foreign PubCo will spin-off Foreign SpinCo to its shareholders. Foreign SpinCo is a great-grandchild subsidiary held by it "through"...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | cross-border b/f with 3-party exchange, cash-out of ineligible shareholders, proportionate allocation of foreign spinco debt, pension liability classification, prelim non-series dividend | 1011 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.1) - Paragraph 55(3.1)(a) | preliminary LP acquisition, cross-border debt repayments and dividend: not part of series | 230 |

| Tax Topics - Income Tax Act - Section 86 - Subsection 86(1) | exchange for substantively identical common shares | 124 |

2012 Ruling 2011-0425441R3 - Cross Border Butterfly

{kind=link}

Overview

A non-resident public company (Foreign Pubco) will be spinning off Business A to its shareholders, to be accomplished by a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | cross-border b/f with 3-party exchange to address s. 55(3.2)(h)/indemnity neutralizes liability assumption/Newco 3 is implicit DC | 367 |

2012 Ruling 2012-0439381R3 - Cross-border spin-off butterfly

underline;">: Background. After preliminary transactions, DC becomes owned by Foreign Pubco. In order to accomplish a butterfly spin-off of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | cross-border b/f as part of foreign spin-off including (U.K.?) demergers | 822 |

2012 Ruling 2011-0431101R3 - Cross-border spin-off butterfly

As preliminary transactions to a butterfly distribution by DC, which is owned by a non-resident subsidiary (Foreign Sub 1) of a non-resident...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | interest deduction following b/f cross-redemption | 143 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | cross-border b/f as part of double Code s. 355 spin-off | 1540 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Permitted Exchange | 429 |

Articles

David Carolin, Manu Kakkar, Paola D’Agostino, "To Redeem or Not To Redeem a Specified Shareholder: That Is the 55(3)(b) Question", Tax for the Owner-Manager, Vol. 23, No. 4, October 2023, p. 6

S. 55(3.1)(b)(i)(C) concern if the preferred shares of a related individual (Dad) are redeemed at the commencement of a butterfly (pp. 6-7)

- The...

Clause 55(3.1)(b)(i)(A)

Subclause 55(3.1)(b)(i)(A)(II)

Administrative Policy

2023 Ruling 2022-0943871R3 - Cross-border spin-off butterfly

Background

Foreign Pubco, the non-resident and publicly traded parent of the group, held DC (a taxable Canadian corporation, or “TCC”)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | cross-border butterfly with 3-corner agreement | 360 |

Clause 55(3.1)(b)(i)(C)

Articles

David Carolin, Manu Kakkar, "Freezes and Butterflies: Who Said Freezes are Easy?", Tax for the Owner-Manager,” Vol. 25, No. 2, April 2025, p. 9

Inapplicability of s. 55(3.1)(b)(i) exception if post-butterfly freeze by TC entails only a subscription by trust for common shares (pp....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) - Subparagraph 55(3)(a)(ii) | 132 |

Paragraph 55(3.1)(c)

Administrative Policy

2023 Ruling 2022-0958601R3 - Post Butterfly Transactions

Background

Xco is a corporation holding cash and shares of Yco. (Yco's other shareholders are management employees and their holding company. )...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | post-butterfly sales and redemptions of shares received on the butterfly were not part of the same series | 444 |

29 November 2016 CTF Roundtable Q. 2, 2016-0669651C6 - Computation of safe income

CRA characterized hypothetical transactions involving the use of discretionary dividend shares as entailing a transfer of value from two related...

2010 Ruling 2010-0357061R3 - Split-up butterfly

After describing the distribution of property by the distributing corporation (DC) to three transferee corporations (TC1, TC2 and TC3) under a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 96 | co-ownership not a partnership | 233 |

3 October 2011 External T.I. 2011-0421341E5 - Paragraphs 55(3.1)(c) or (d)

before a distribution made in the course of a butterfly reorganization, Opco sells real estate used in operating its business (and representing...

27 August 1999 External T.I. 9828785 F - PAPILLON

In finding that if the butterfly was effected on a net FMV basis, so should the application of the 10% test, the Directorate stated:

The...

x1995 Tax Executives Institute Round Table, Q. 2, File No. 951074

S.55(3.1)(c) would apply to deny the protection of the butterfly exemption in a situation where a corporate 30% shareholder of the distributing...

31 July 1995 External T.I. 9518445 - 50731

Example of a problem arising because s. 55(3.1)(c)(ii)(B) is not modified by the parenthetical expression "(other than money and indebtedness that...

Articles

David Carolin, Manu Kakkar, "Problematic Post-Butterfly Transferee Corporation Dispositions Involving Paragraph 55(3.1)(c): Part I", Tax for the Owner-Manager, Vol. 22, No. 2, April 2022, p. 3

Purpose of s. 55(3.1)(c) continuity-of-interest rule (p.3)

The underlying purpose of paragraph 55(3.1)(c) is to prevent a butterfly whereby a...

Subparagraph 55(3.1)(c)(ii)

Clause 55(3.1)(c)(ii)(B)

Administrative Policy

28 February 2002 External T.I. 2002-0120315 F - Butterfly Transactions

1st situation (post-butterfly share issuance by distributed corporation)

In the first situation, Holdco made pursuant to a butterfly...