Administrative Policy

17 May 2023 IFA Roundtable Q. 3, 2023-0964551C6 - T1134 Supplement

Finance indicated that given that (as stated in the Explanatory Notes) ss. 90(2) and (5) provided a comprehensive definition of what constituted a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 233.5 | T1134 should be timely-filed with missing information noted | 162 |

2016 Ruling 2015-0617351R3 - payments under a German profit transfer agrmt “PTA"

Current structure

XX2, an indirect controlled foreign affiliate of a Canadian public corporation, is the sole limited partner of a German KG, and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(8.1) | survivor merger of two German CFAs | 44 |

11 April 2017 Internal T.I. 2016-0670541I7 - Foreign affiliate share redemption

Canco owned 100% of the preferred shares of a Barbados International Business Company (“FA”), all of whose common shares are held by a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Dividend | redemption proceeds might in part be a dividend under Barbados law | 147 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(6) - Paragraph 95(6)(b) | skewing exempt surplus to Canco could engage s. 95(6) | 137 |

2015 Ruling 2014-0541951R3 - Foreign Affiliate Debt Dumping

A limited liability partnership (FA1) will pay a distribution proportionately to its partners who directly comprise (i) a limited partner...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(9) - Paragraph 212.3(9)(b) - Subparagraph 212.3(9)(b)(ii) | s. 212.3(9)(b)(ii) PUC restoration for upper-tier QSCs on the payment by a U.S. LLP of a proportionate “dividend” to lower tier CRIC partners | 349 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Corporation | proportionate distribution by LLP treated as dividend | 128 |

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(3) | two Canadian corporate partners immediately beneath the U.S. border are QSCs respecting investments made by lower-tier CRICs in a U.S. LLP | 238 |

26 May 2016 IFA Roundtable Q. 6, 2016-0642081C6 - German Organschafts

Under an “Organschaft,” a German corporation (“Parentco”) and another corporation resident in Germany (“Subco”) enter into a Profit...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(a) - Subparagraph 95(2)(a)(ii) - Clause 95(2)(a)(ii)(B) | profit transfer payments made by a German sub to German parent are s. 90(2) dividends not within s. 95(2)(a)(ii)(B) after 2016 | 153 |

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(1) - Paragraph 53(1)(c) | German profit transfer payment to loss subsidiary is contribution of capital | 158 |

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(x) | loss compensation payment under Organschaft | 123 |

8 January 2016 Internal T.I. 2015-0604491I7 - mandatory redeemable preferred shares

CRA applied the two-step approach to entity classification to find that MRPS (Luxembourg hybrid instruments which were “very similar to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Share | MRPS (Luxembourg hybrid instruments which were “very similar to traditional shares under Canadian business corporations statutes”) were equity | 731 |

2015 Ruling 2014-0527961R3 - Deemed dividend under subsection 90(2)

underline;">: €/US$ share structure. The constating documents of FA (which is a wholly-owned subsidiary of Canco that was incorporated and is...

17 June 2014 External T.I. 2013-0506731E5 - Immigration

An individual shareholder immigrates to Canada, thereby becoming a Canadian resident, and then receives $1,000 from a wholly-owned non-resident...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Payment & Receipt | note satisfied dividend | 83 |

| Tax Topics - Income Tax Act - Section 128.1 - Subsection 128.1(1) | dividend receivable acquired on immigration | 141 |

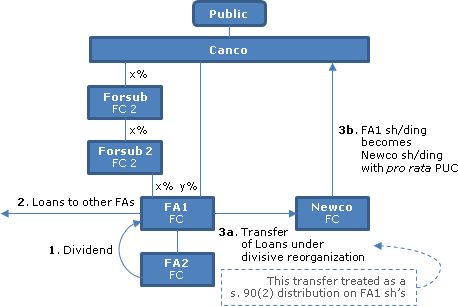

2013 Ruling 2012-0463611R3 - Foreign Divisive Reorganization

{kind=link}

Structure

Canco, a Canadian public company, directly owns a portion of the shares of FA1. FA1 is a controlled foreign affiliate of Canco...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) - Paragraph 15(1)(b) | 452 |

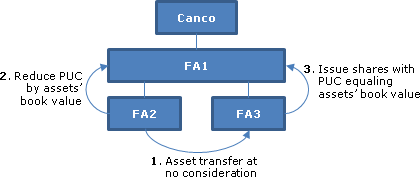

23 May 2013 IFA Round Table, Q. 2

{kind=link}

Canco owns 100% of the shares of FA1 and FA1 owns 100% of the shares of FA2. FA3 is either formed with nominal assets by FA1 or comes into...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) - Paragraph 15(1)(b) | 219 |

Articles

Melanie Huynh, Paul Barnicke, "German Organschafts", Canadian Tax Highlights, Vol. 24, No. 6, June 2016, p. 5

Unclear whether CRA view on application of s. 90(2) to Organschaft profit transfers applies where s. 90(2) applies retroactively (p. 6)

Referring...

Michael Gemmiti, "FA Dividends Must be Pro Rata", Vol. 3, No. 3, August 2013, p. 7

The new pro rata rule can present problems. For example, a US LLC (which qualifies as an FA of a taxpayer) may have only one class of units but...

Patrick W. Marley, Kim Brown, "Foreign Mergers and 'Demergers' Under Recent Canadian Proposals", Tax Management International Journal, 10 February 2012, Vol 41, No. 2, p. 86

A demerger, which under the foreign corporate law, might be viewed as one stream splitting into two, might not qualify under draft s. 90(2) as a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | 46 | |

| Tax Topics - Income Tax Act - Section 52 - Subsection 52(2) | 88 |

Geoffrey S. Turner, "Upending the Surplus Ordering Rules: Implications of the New Regulation 5901(2)(b) Election", CCH Tax Topics, No. 2079, p. 1, 12 January 2012

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5901 - Subsection 5901(2) - Paragraph 5901(2)(b) | 32 |

Elaine Buzzell, "Distributions of Share Premium by Foreign Affiliates", Corporate Finance, Vol. XVII, No. 2, 2011, p. 1962

Includes discussion of the treatment under the previous version of s. 90 of payments out of a share premium account as a dividend or shareholder...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5901 - Subsection 5901(2) - Paragraph 5901(2)(b) | 9 |