Cases

Canada v. Alta Energy Luxembourg S.A.R.L., 2021 SCC 49, [2021] 3 S.C.R. 590

Two US firms transferred their investment in a Canadian subsidiary (Alta Canada), that was to develop a shale formation in northern B.C., to a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | Treaty shopping to avoid capital gains tax on Canadian resource assets was contemplated, and not a Treaty abuse | 660 |

| Tax Topics - Treaties - Income Tax Conventions - Article 4 | a company resident under Luxembourg domestic law (its legal seat was there), and that was “liable to be liable to tax,” was resident there for Treaty purposes even though a conduit | 386 |

| Tax Topics - Treaties - Income Tax Conventions | subsequent OECD Treaty commentary not followed | 198 |

| Tax Topics - Statutory Interpretation - Treaties | additional consideration in Treaty context of giving effect to the contractual bargain | 237 |

Canada v. Alta Energy Luxembourg S.A.R.L., 2020 FCA 43, aff'd 2021 SCC 49

A Blackstone LP and a U.S. shale company transferred their investment in a Canadian subsidiary (Alta Canada), that was to develop a shale...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | object and spirit of Lux Treaty was no broader than its words | 465 |

Canada v. Sommerer, 2012 DTC 5126, 2012 FCA 207

After finding that s. 75(2) did not apply to attribute to the Canadian-resident taxpayer a taxable capital gain realized by an Austrian private...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(1) | Austrian foundation likely not a trust | 181 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(5) | 84 | |

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | does not apply to FMV purchases | 236 |

| Tax Topics - Treaties - Income Tax Conventions | treaty applies to economic double taxation | 356 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | s. 75(2) should not be applied to attribute the same gain to 2 taxpayers | 115 |

Haas Estate v. Canada, 2001 DTC 5001 (FCA)

Where a United States resident has disposed of Canadian real property, the calculation of the reduction under Article XIII(9) of the Canada-U.S....

Canada (Attorney General) v. Kubicek Estate, 97 DTC 5454, (sub nom. Kubicek Estate v. R.) [1997] 3 C.T.C. 435 (FCA)

Given that "the ordinary meaning of 'gain' for the purposes of Article XIII of the [Canada-U.S.] Convention is the gain which is subject to tax"...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions | 64 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 3 | no requirement for a definition per se in the domestic legislation for 3(2) to apply | 94 |

Gladden Estate v. The Queen, 85 DTC 5188, [1985] 1 CTC 163 (FCTD)

The "sale or exchange" of capital assets under Article VIII of the 1942 Canada-U.S. Convention included a deemed disposition of capital property...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions | Tax Treaty should be accorded a liberal interpretation | 47 |

Hurd v. The Queen, 81 DTC 5140, [1981] CTC 209 (FCA)

The purchase of shares pursuant to an employee stock option agreement was found not to be "an exchange of capital assets" within the meaning of...

See Also

C & W Offshore Ltd. v. The King, 2026 TCC 40

The Canadian taxpayer (“C&W Offshore”) was contacted by one of its Canadian customers, Cedrill Canada, to procure replacements for mooring...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Agency | equipment not subleased as agent for the lessor | 143 |

| Tax Topics - Income Tax Act - Section 227 - Subsection 227(8) - Paragraph 227(8)(a) | due diligence defence not established where taxpayer had been oblivious to withholding tax issue | 248 |

Alta Energy Luxembourg S.A.R.L. v The Queen, 2018 TCC 152, aff'd 2020 FCA 43, aff'd 2021 SCC 49

A U.S. corporation (“Alta Resources USA”), which was a leader in the development of shale oil and gas assets in the U.S., and a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | no abuse in non-resident investors using a s.à r.l. to avoid capital gains tax on a new Canadian exploration company | 384 |

| Tax Topics - Statutory Interpretation - Interpretation Bulletins, etc. | taxpayers should be able to rely on CRA position in making a capital investment | 125 |

Resource Capital Fund IV LP v Commissioner of Taxation, [2018] FCA 41 (Federal Court of Australia), rev'd on various grounds [2019] FCAFC 51

Two Caymans investment LPs (“RCF IV” and RCF V”) whose limited partners were mostly U.S. residents, realized gains on income account from...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Shares | private equity fund LP with 5-year holding objective realized share gain on income account | 175 |

| Tax Topics - Income Tax Act - Section 115 - Subsection 115(1) - Paragraph 115(1)(a) - Subparagraph 115(1)(a)(ii) | gains of a NR PE fund from disposals of Australian share investments that were managed in part in Australia were derived from Australia | 427 |

| Tax Topics - Treaties - Income Tax Conventions - Article 3 | each U.S.-resident partner of a Caymans PE LP carried on a U.S. “enterprise” | 234 |

| Tax Topics - General Concepts - Stare Decisis | lower court not bound by a point of law that was assumed rather than examined by a higher court | 292 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(1) | assessment of partnership was assessment of partners | 89 |

| Tax Topics - Treaties - Income Tax Conventions - Article 6 | Art. 6 extends common law meaning of real property | 198 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Taxable Canadian Property - Paragraph (d) | shares of lithium mining and processing company were derived principally from the processing rather than mining operation and, thus, were not taxable Australian real property | 514 |

| Tax Topics - Income Tax Act - Section 218.3 - Subsection 218.3(1) - Canadian Property Mutual Fund Investment | shares of Australian mining company were primarily attributable to the processing rather than mining operations | 142 |

| Tax Topics - General Concepts - Fair Market Value - Other | processing assets of mining company were more valuable than its mining assets | 238 |

Commissioner of Taxation v. Resource Capital Fund III LP, [2014] FCAFC 37 (Fed. Ct. of Austr.)

The appellant ("RCF") was a non-Australian partnership which was assessed on the basis that its gain from the sale of a "member ship interest" in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Other | mining information not to be valued separately at reproduction cost | 296 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Taxable Canadian Property | mining information not to be valued separately at reproduction cost | 296 |

| Tax Topics - Treaties - Income Tax Conventions - Article 4 | reverse hybrid partnership | 431 |

Resource Capital Fund III LP v. Commissioner of Taxation, [2013] FCA 363 (Fed. Ct. of Austr.), rev'd supra.

The appellant ("RCF") was a Caymans limited partnership with mostly US-resident partners, which was assessed under the "taxable Australian real...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Other | 412 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 4 | 320 |

Kaplan Estate v. The Queen, 94 DTC 1816 (TCC)

Land of U.S.-resident (which had an adjusted cost base to him of $17,050 based on its V-day value) was acquired by him in 1952 at a cost of $7,000...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Interpretation Bulletins, etc. | 39 |

Administrative Policy

17 November 2025 External T.I. 2020-0854261E5 - German Treaty - Art.13

A Canadian resident corporation (Canco), whose beneficial shareholders were residents of Germany, each owning at least 10% of its shares, wholly...

2023 Ruling 2022-0958521R3 - foreign absorptive mergers

After giving effect to some preliminary transactions, a U.S. corporation which was a qualifying person for purposes of the Canada-US Treaty (the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(8.2) | rulings on foreign absorptive downstream and upstream mergers | 570 |

3 February 2022 Internal T.I. 2021-0922301I7 - Art. XIII(7) Canada -US Treaty and Trusts

A Canadian-resident trust (the “Trust”) will realize a capital gain on a deemed disposition (the “Deemed Disposition”) pursuant to s....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 24 | Art. XXIV(2)(a) of the U.S. Treaty does not require s. 126(1) to provide a carryback of US tax | 316 |

2020 Ruling 2019-0801011R3 - Article 13(4) of the Treaty

Background

Mr. A, who has never been a resident of Canada and is a resident of a redacted country for purposes of Art. 4 of the Treaty with that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 116 - Subsection 116(5.02) | children under 18 had the legal capacity to give a s. 116(5.02) notice | 171 |

4 June 2019 Internal T.I. 2018-0783441I7 F - Sale of land by a resident of Hong Kong

A non-resident individual (the "Non-resident") residing in Hong Kong for the purposes of the Canada-Hong Kong Convention disposed of land located...

7 June 2017 CPTS Roundtable, 2017-0695131C6

If a U.K. resident disposes of shares of its Canadian subsidiary that derive the greater part of their value from rights related to an active oil...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(21) - Proceeds of Disposition | Q.1 - Daishowa extends beyond reforestation and reclamation obligations only on a case-by-case basis | 213 |

| Tax Topics - Income Tax Act - Section 66 - Subsection 66(15) - Canadian Resource Property - Paragraph (d) | Q.2 - a Canadian resource royalty interest requires a right to “take production” | 135 |

| Tax Topics - Income Tax Act - Section 115 - Subsection 115(1) - Paragraph 115(1)(a) - Subparagraph 115(1)(a)(ii) | Q.4 - by analogy to mining, hydrocarbons may be similar properties | 348 |

| Tax Topics - Income Tax Regulations - Regulation 1101 - Subsection 1101(1) | Q.5 - normal course dispositions of oil and gas properties generally are not of a separate business | 131 |

| Tax Topics - Income Tax Act - Section 4 - Subsection 4(1) - Paragraph 4(1)(a) | Q.5 - application of Scales test to determining whether there is a separate business | 224 |

| Tax Topics - Income Tax Regulations - Schedules - Schedule II - Class 26 | Q.7 - refinery catalysts are Class 26 property | 87 |

| Tax Topics - Income Tax Regulations - Schedules - Schedule II - Class 49 | Q.8 - taxpayers generally have the documentary evidence on hand to allocate costs between pipelines and pipeline appendages | 117 |

22 September 2017 External T.I. 2016-0668041E5 - TCP and Article 13(5) of Canada-UK Treaty

A Netherlands corporation (BVCo) holds 1/3 of its assets as shares of an Australian subsidiary (“AusCo”), whose Australian real estate assets...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Taxable Canadian Property - Paragraph (d) | proportionate value approach to determining whether shares of a foreign holding company are derived more than 50% from Canadian immovable property for Treaty purposes | 308 |

17 February 2017 External T.I. 2015-0602781E5 - Disposition of farm property by a non-resident

A resident of Germany will gift her shares, each qualifying as a “share of the capital stock of a family farm or fishing corporation” under s....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 116 - Subsection 116(4) | CRA may accept a T2062 showing deemed s. 73(4.1) rollover proceeds | 297 |

| Tax Topics - Income Tax Act - Section 116 - Subsection 116(6.1) | failure to file notice within 30 days | 150 |

1 March 2017 External T.I. 2016-0658431E5 - Article XIII of Canada-U.S. Convention

Are shares or trust interests in a resident corporation or trust considered to derive their value principally from real property situated in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Taxable Canadian Property - Paragraph (d) | derived principally test done on look-through basis | 144 |

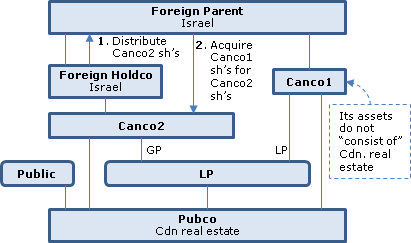

2014 Ruling 2014-0527221R3 - Disposition of shares under Canada-Israel Treaty

{kind=link}

Current structure

Foreign Parent, an Israeli public company, holds its LP interest in LP through a Canadian subsidiary (Canco1) and holds its GP...

17 November 2014 External T.I. 2014-0555061E5 - Canada-Japan Income Tax Convention, Article 13

Paragraph 4 of the Canada-Japan Treaty states that "Gains derived by a resident of a Contracting State from the alienation of any property other...

24 September 2014 External T.I. 2014-0543071E5 F - Article XIII of the Canada-France Treaty

An individual resident in Canada, who held the bare ownership of French immovable property, disposed of the property at a gain. France was...

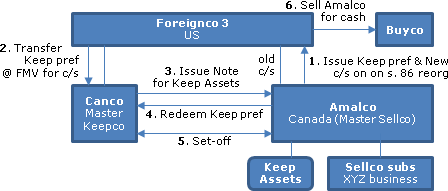

2012 Ruling 2011-0403291R3 - Treaty exempt sale

{kind=link}

Following a preliminary reorganization (including an amalgamation of predecessors of Amalco so as to "consolidate the tax attributes"), all the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | partnership distribution to one of partners not disposition of the partnership interests | 74 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2) | Treaty step-up to avoid the application of s. 55(2) to a spin-off made to effect an arm's length sale of the rump | 337 |

14 April 2014 Internal T.I. 2013-0516151I7 F - Article XIII(4) of the Canada-XXXXXXXXXX Convention

A non-resident corporation (Vendor) disposed at a gain of shares of Canco, which held partnership interests in two Quebec real estate partnerships...

4 December 2013 Internal T.I. 2013-0489051I7 - Personal-Use-Property & Article XIII(9)

A U.S. resident owned vacant land in Canada from before September 26, 1980 and after that date built a cottage thereon. CRA found:

If the cottage...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 116 - Subsection 116(1) | personal-use land and building are one property | 107 |

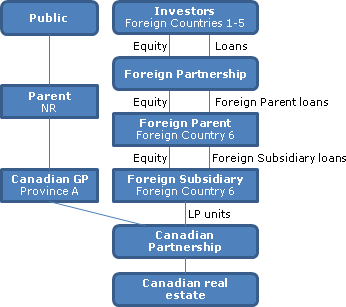

2013 Ruling 2012-0444431R3 - Taxable Canadian Property

{kind=link}

A partnership (Foreign Partnership), whose non-resident members (Investors) are resident in Foreign Countries 1 through 5, uses a portion of its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Taxable Canadian Property - Paragraph (d) | foreign partnership holding debt in addition to equity of foreign holdco | 160 |

28 November 2011 CTF Roundtable, 2011-0425901C6 - Does share derive value principally from real prop

After the questioner referenced the previous position that, in the context of Treaty references to shares deriving in their value principally from...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Taxable Canadian Property - Paragraph (d) | proportionate consolidation | 152 |

17 May 2012 IFA Roundtable, 2012-0444161C6 - Competent Authority Agreements

In responding to a query which noted that the Canada-U.S. Treaty, unlike other Conventions, specifically referred to deferral agreements of...

22 June 2012 External T.I. 2011-0416521E5 - Share Options and Taxable Canadian Property

The definition in Art. XIII of the Canada-US Convention of "real property situated in the other Contracting State" includes, in the case of real...

2012 Ruling 2011-0429961R3 - Hydrocarbon & Immovable property: Canada-UK Treaty

Ruling that the transfer of shares of a UK company (Forco2 - whose value is derived from CAnco shares) by two other UK companies (Forco1 and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 116 - Subsection 116(6.1) | 117 |

2008 Ruling 2008-0272141R3 - Conversion of Delaware corporation into LLC

The shares of a U.S. corporation (D Co) holding two Canadian subsidiaries (G Co and H Co) whose shares are taxable Canadian property are...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | conversion into Delaware LLC of U.S. corp. holding taxable Canadian property | 109 |

20 August 2007 External T.I. 2005-0111151E5 - Article 13(4) Canada - Germany Tax Agreement

"Real property would not be considered rental property for purposes of Article 13(4) of the [Canada-Germany] Treaty unless the property was...

9 September 2004 External T.I. 2004-0093091E5 - Approved Stock Exchange; Article 13

An "approved stock exchange" in Article 13 of the Luxembourg and Netherlands Conventions meant a stock exchanged prescribed for purposes of the...

5 September 2003 External T.I. 2003-0029675 - Article XIII(3)(b)(ii) U.S. Treaty

Although in most cases comparing gross asset values will be the simpler (and perhaps quite often the most reasonable) method for making the 50...

8 April 2003 External T.I. 2003-000199

After referring to Bromley v. Tryon, [1952] AC 265 (HL) ("'greater part' means anything over one-half"), CCRA stated that:

"The term 'value or the...

26 March 2001 External T.I. 2001-0070585 F - Interaction entre Convention Canada-US et LIR

A U.S. resident subsequently disposes of shares, which were taxable Canadian property, received on a s. 87(1) amalgamation in exchange for shares...

9 January 2001 External T.I. 2000-0042545 - Immovable property

The exception for real property in which the business of the enterprises carried on apparently was viewed as being available where the shares of a...

2000 Ruling 2000-0015753 - Article 13 - Canada-Netherlands Treaty

A disposition by a Netherlands resident of shares of a Canadian corporation (perhaps a Canadian holding company holding a Canadian oil and gas...

30 November 1999 External T.I. 9825155 - CANADA-UK TAX CONVENTION

Where an individual resident of the U.K. owns all the shares of a private Canadian corporation that, in turn, has as its principal asset less than...

22 October 1997 External T.I. 9710835 - ARTICLE XIII(5) U.S. TREATY (DUAL RESIDENTS)

Where an individual resident of Canada moves to the United States in 1994 and becomes a resident of the United States at that time for treaty...

15 October 1997 External T.I. 9713855 - ARTICLE XIII CANADA-ISRAEL TAX TREATY

Canada has the right to tax gains of a taxpayer from the deemed disposition of real property situate in Israel as a result of the taxpayer ceasing...

25 April 1997 External T.I. 9709905 - SALE OF P-SHIP INTEREST BY NON-RESIDENT.

A gain realized by the disposition by a U.S. resident of an interest in a partnership the value of which is not derived principally from real...

2 January 1996 External T.I. 9514185 - ARTICLE XIII CANADA-ISRAEL TREATY

Where a corporation resident in Israel alienates shares of a corporation resident in Canada the only assets of which are shares of a second...

18 September 1995 External T.I. 9510365 - SOURCE OF CAPITAL GAIN CANADA-JAPAN TREATY

In considering where a gain from the alienation of shares would be considered to "arise" for purposes of paragraph 4 of Article XIII of the...

13 September 1995 Internal T.I. 9518087 - GAINS IN U.S. TREATY & LIFE INSURANCE PROCEEDS

The word "gains" in article XIII of the Canada-U.S. Convention means capital gains.

29 August 1995 External T.I. 9506785 - PROPERTY...IN WHICH BUSINESS OF CO CARRIED ON

"Property... in which Business of Co. Carried on"): Respecting the exclusion in Article XIII, paragraph 4 of the Canada-Netherlands Convention...

13 July 1995 External T.I. 9505185 - UK CONVENTION ART XIII - SHARES

Capital gains realized by a U.K. shareholder on the alienation of shares of a Canadian public corporation and whose shares derived most of their...

26 April 1995 External T.I. 9501815 - CAP. GAIN - CANADA-IRELAND TAX AGREEMENT

A resident of Ireland is subject to tax of 15% on the disposition of shares that are taxable Canadian property in light of Article VI of the...

10 February 1995 External T.I. 9426405 - ART XIII(3) CANADA-U.S. CONVENTION -SHARE INCLUDES OPTION

"The reference in paragraph 3 of Article XIII [of the Canada-U.S. Convention] to 'a share of the capital stock of a company, the value of whose...

12 June 1995 External T.I. 9500915 - ARTICLE 13 CANADA-U.K. TREATY AND LOOK THROUGH BASIS

Given that paragraph 5 of Article 13 of the Canada-U.K. Convention is to be applied on a look-through basis, subparagraph 7(b) of Article 13 also...

Income Tax Technical News, No. 4, 20 February 1995

When the pro rata method in Article XIII, para. 9 of the U.S. Convention is used to reduce the amount of the capital gain, the months before 1972...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 149 - Subsection 149(1) - Paragraph 149(1)(l) | 22 | |

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | 62 |

6 June 1994 External T.I. 9335425 - "ALIENATION OF PROPERTY" AND "INCOME"

A resident of the U.K. will be granted relief from Canadian tax under Article 13, paragraph 8 of the Canada-U.K. Convention on the deemed...

1993 A.P.F.F. Round Table, Q. 25

A capital gain arising as a result of a distribution of paid-up capital on common shares held by a non-resident generally would be exempt under...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 116 - Subsection 116(1) | 28 |

11 December 1992 T.I. (Tax Window, No. 27, p. 17, ¶2329)

A U.K. citizen who is resident in Canada for 20 years, then resident in the U.K. for seven years, before he sells a U.K. real property in respect...

6 November 1992 Income Tax Severed Letter 9233205 - Article XIII, 7(b) of U.K. Convention

With respect to the exclusion in paragraph 7 of Article XIII of the Canada-U.K. Convention for property (other than real property) in which the...

8 October 1992 T.I. 920970 (September 1993 Access Letter, p. 419, ¶C111-056)

Where a property drops in value after 1984 and then recovers before the date of its disposition, the availability of any transitional relief in...

17 March 1992 T.I. (Tax Window, No. 18, p. 11, ¶1809)

The gain realized by a U.S. resident who sells an interest in a U.S. partnership which conducts a manufacturing business in Canada and does not...

18 July 1991 T.I. (Tax Window, No. 6, p. 7, ¶1361)

An individual is resident of Canada for 15 years or more (paragraph 9) if he is a resident of Canada for discrete periods aggregating 15 years and...

90 C.P.T.J. - Q.33

Although Canadian resource properties are now viewed as something other than capital assets, paragraph 9 of Article XIII of the U.S. Convention...

27 February 1990 Memorandum (July 1990 Access Letter, ¶1335)

The Canada-U.S. Income Tax Convention would have the effect of exempting a U.S. resident from AMT with respect to capital gains.

84 C.R. - Q.58

guidelines re principal derivation of value from real estate.

84 C.R. - Q. 40

RC accepts the interpretation of "alienation" contained in the Treasury Department's technical explanation, which refers to deemed dispositions...

Articles

Michael Lang, "Income Allocation Issues Under Tax Treaties", Tax Notes International, April 21, 2014, p. 285.

Allocation conflict in Sommerer (pp. 289-90)

[S]ubsection 75(2)…is an allocation rule that can lead to the income being taxed in the hands of a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions | 243 |

Geoffrey S. Turner, "Harmonizing Tax Treaty Exemptions and Taxable Canadian Property: Demise of the Buisness Property Exemption", International Tax, No. 64, CCH, June 2012, p. 5

"The older tax treaties with broad exeptions for business property, listed shares, and minority 'non-substantial' interests no longer manifest...

Greg S. Lindsay, "U.S. Investment in Canadian Resource Property: Recent Developments", International Tax Planning, Vol. XVI, No. 3, 2011, p. 1120

Includes discussion of exclusions in immovable property definition in Luxembourg and Netherlands treaties; and treaty shopping.

Lanthier, "Acquiring, Holding and Financing Canadian Corporations", Bulletin for International Fiscal Documentation, Vol. 48, No. 8/9, August/September 1994, Special IFA issue, p. 419.

Discussion of "Canadian spider" structure.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 133 - Subsection 133(1) | 0 |