Subsection 85.1(1) - Share for share exchange

Administrative Policy

2021 Ruling 2020-0852951R3 - Public Spin-Off Butterfly

Parent, a listed corporation with a specified shareholder (and perhaps with two classes of multiple voting and single voting shares), wishes to spin off one of its subsidiaries, whose shares are held, in part, through a subsidiary of Parent (Sub1) and partly by Parent directly. CRA provided butterfly and other ruling on two successive spin-off butterflies pursuant to which Sub1 spins-off its shares of the subsidiary to Parent, then Parent drops all of its shares of the subsidiary into a Newco which then is spun-off to its shareholders.

In addition:

- S. 85.1 applies to the component of the second spin-off pursuant to which the Parent shareholders exchange special shares of Parent received by them under a s. 86 reorg to Newco in exchange for Newco shares (unless they choose to jointly elect with Newco under s. 85(1)).

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.02) | spin-off of grandchild of public corporation to direct Newco subsidiary followed by spin-off to public shareholders | 562 |

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(1.4) | stock options replaced by stock options with lower exercise price on shares of shrunken post-spin-off corp | 131 |

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Public Corporation | election made for Newco that is spun-off by Pubco | 130 |

2014 Ruling 2014-0530371R3 - Combination of credit unions

CRA provided s. 85.1 rulings respecting "Acquireco" acquiring all of the shares of the members of a widely-held credit union under s. 85.1 in exchange for Acquireco treasury shares (with the exception of the Class D shares of the target, which will be redeemed for cash).

See summary under s. 88(1).

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 137 - Subsection 137(4.1) | s. 137(4.1) inapplicable to Buyer of credit union who winds it up rather than becoming a member | 263 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) | "immediately before" referenced share ownership on completion of the preceding transaction in a same-day series | 268 |

S4-F5-C1 - Share for Share Exchange

Subsection 85.1(1) will not apply where:

a. the vendor acquires shares of the purchaser in exchange for other shares of the purchaser;

b. the vendor acquires shares of the purchaser from a shareholder of the purchaser in exchange for shares of the acquired corporation; ...

g. subject to ¶1.7, the consideration received by the vendor for the exchanged shares includes shares of more than one class of the capital stock of the purchaser (paragraph 85.1(2)(d)); or

h. subject to ¶1.7, the consideration received by the vendor for the exchanged shares includes consideration other than shares of the purchaser (non-share consideration) (paragraph 85.1(2)(d)). A right to acquire shares to be issued by the purchaser in the future as a settlement of a portion of the exchange is non-share consideration.

1.7 In certain circumstances, even if a share exchange is one that is described in ¶1.6(g) or (h,) subsection 85.1(1) could still apply. Subsection 85.1(1) may apply where a vendor:

- receives newly issued shares of one class from the purchaser for some of the exchanged shares and non-share consideration or shares of a different class for other exchanged shares. The vendor must be able to clearly identify which exchanged shares were exchanged in consideration for the newly issued shares of that class of the purchaser and which were exchanged in consideration for shares of another class of the purchaser or for non-share consideration….

- receives newly issued shares of the purchaser and non-share consideration for each exchanged share. The purchaser's offer must clearly indicate which fraction of each exchanged share is exchanged in consideration for the newly issued shares of the purchaser and which fraction of each exchanged share is exchanged for non-share consideration….

- cannot receive a fractional share but is entitled under an exchange agreement to receive cash or other non-share consideration in lieu of a fraction of a newly issued share of the purchaser. Where the total value of the non-share consideration is $200 or less, the vendor may ignore the computation of the gain or loss on the partial disposition and reduce the adjusted cost base of the shares received by the amount of that value. Alternatively, the vendor may report the gain or loss. …

1.12 Paragraph 85.1(1)(b)… appl[ies] even if the vendor has otherwise reported a gain or loss on the exchange.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85.1 - Subsection 85.1(2.1) | 26 | |

| Tax Topics - Income Tax Application Rules - Subsection 26(26) | 104 |

25 August 1991 T.I. (Tax Window, No. 8, p. 16, ¶1412)

The fact that shares are divided into two blocks -one of which is exchanged for cash and the other which is exchanged for shares - in order to bring the transaction within s. 85.1, does not by itself result in the application of GAAR.

IT-450 "Share for Share Exchange"

7

...Where the vendor receives shares and cash or other consideration for each exchanged share, subsection 85.1(1) may be utilized for the fraction of each exchanged share for which only share consideration was received, provided that the purchaser's offer clearly indicates that the share consideration will be exchanged for a specified fraction of each share tendered and the non-share consideration will be given for the remaining fraction. ...

Articles

Cobb, "Share-for-Share Exchanges: Section 85.1", The Taxation of Corporate Reorganizations, 1995 Canadian Tax Journal, Vol. 43, No. 6, p. 2230.

Smith, "Corporate Restructuring Issues: Public Corporations", 1990 Corporate Management Tax Conference Report, pp. 6:8-6:10: discussion of receipt of non-share consideration.

Paragraph 85.1(1)(a)

Administrative Policy

20 July 2000 External T.I. 1999-0008445 F - Produit de Disposition

The shareholders of Opco agreed to sell each Opco share for a sale price of $10, which was to be satisfied at their option in cash or by the issuance of 5 shares of Pubco whose FMV at the time of the agreement was $2 per share.

The Agency indicated that where a vendor receiving Pubco shares was a self-directed RRSP, which did not make an election under s. 85(1), the rules in s. 85.1(1)(a) would apply to it.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85.1 - Subsection 85.1(1) - Paragraph 85.1(1)(b) | cost to purchaser is determined under s. 85.1(1)(b) irrespective of gain elected to be recognized by vendor | 118 |

Paragraph 85.1(1)(b)

Administrative Policy

20 July 2000 External T.I. 1999-0008445 F - Produit de Disposition

The shareholders of Opco agreed to sell each Opco share for a sale price of $10, which was to be satisfied at their option in cash or by the issuance of 5 shares of Pubco whose FMV at the time of the agreement was $2 per share.

The Agency indicated that the cost of the Opco shares to the purchaser (Pubco) acquired for Pubco shares would be determined pursuant to s. 85.1(1)(b) even if the vendor included in its income the taxable capital gain from the disposition of the shares, and regardless of the amount allocated by Pubco to the stated capital of the shares of its capital stock issued as consideration for the exchanged Opco shares.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85.1 - Subsection 85.1(1) - Paragraph 85.1(1)(a) | rules in s. 85.1(1)(a) applied to vendor RRSP | 79 |

Subsection 85.1(2.1) - Computation of paid-up capital

Administrative Policy

S4-F5-C1 - Share for Share Exchange

1.16 Paragraph 85.1(2.1)(a) is applicable…even if the vendor has otherwise reported a gain or loss on the exchange.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85.1 - Subsection 85.1(1) | 412 | |

| Tax Topics - Income Tax Application Rules - Subsection 26(26) | 104 |

17 February 2003 External T.I. 2002-0176455 - Amount Added to Paid-up Capital of Shares

Aco holds 30 common shares of Opco (30% of the common shares) having an ACB and PUC of $30 and an FMV of $300 (the gross and net fair market value of the assets of Opco having an FMV of $1,000). A (an individual who is the sole shareholder of Aco) transfers all his common shares of Aco (being 30 common shares having an FMV of $300 and ACB and PUC of $30) to Opco in exchange for 30 Opco shares, realizing a capital gain of $270. A and Aco deal at arm's length with Opco.

Subsection 85.1(2.1) will apply to grind the paid-up capital of the Opco shares from $300 down to $30.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(1) | no 84(1) application on tuck under | 112 |

Subsection 85.1(3) - Disposition of shares of foreign affiliate

Administrative Policy

2016 Ruling 2015-0571441R3 - Dutch Cooperative - 93.2 & 95(2)(c)

Ruling respecting the combined operation of s. 95(2)(c) (similar in this regard to s. 85.1(3)) and s. 93.2) on a joint contribution by the three foreign affiliate shareholders of a foreign affiliate of their respective shareholdings to a Dutch co-operative (with membership interests rather than share capital) in consideration for credits to their respective membership interest accounts.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(c) | rollover is available on joint drop-down of shares of a Dutch private limited liability company into a Dutch cooperative in consideration for respective credits to the membership accounts | 502 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Corporation | Dutch cooperative whose articles limited member liability was a corp | 263 |

| Tax Topics - Income Tax Act - Section 93.2 - Subsection 93.2(2) | membership interest in Dutch cooperative ruled to be shares | 92 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Controlled Foreign Affiliate | non-resident subsidiaries CFAs of bottom-tier Cdn partnership and FAs of Canadian corporate partners | 130 |

26 May 2016 IFA Roundtable Q. 10, 2016-0642101C6 - 93.2 & 95(2)(c)

S. 95(2)(c) which, insofar as relevant to the question of how it dovetails with s. 93.2, is essentially identical to s. 85.1(3). Respecting the transfer by a foreign affiliate (FA1) of Canco of all its the shares of FA2 to another non-resident subsidiary of FA1, viz., a non-share corporation (“FA3”), as a capital contribution, CRA noted that, as a technical matter, s. 93.2(3)(a) does not appear to go quite far enough so as to permit the particulars of the cost-apportionment formula in s. 95(2)(c) to be filled in. However, CRA went on to find that despite these “textual challenges,” the s. 95(2)(c) rollover would be available provided that the fair market value of the membership interest in FA3 increased by the FMV of the contributed shares.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(c) | dropdown of shares made to an LLC as a contribution of capital deemed by s. 93.2(3) to be for "share” consideration | 154 |

| Tax Topics - Income Tax Act - Section 93.2 - Subsection 93.2(3) | s. 95(2)(c) rollover can apply on a dropdown of shares made to an LLC as a contribution of capital rather than for “share” consideration | 278 |

2016 Ruling 2016-0648991R3 - Internal spinoff reorganization of XXXXXXXXXX

CRA provided s. 55(3)(a) rulings respecting a spin-off by one Canadian subsidiary (CanSub1) of a public company (ParentCo) of CanSub1’s foreign subsidiary (ForSub1) to another wholly-owned Canadian subsidiary (CanSub2) of ParentCo. It was proposed that the acquisition by CanSub2 of the ForSub1 shares be followed by their s. 85.1(3) drop-down to a foreign subsidiary of CanSub2 in consideration for common shares of equivalent value. CRA ruled that this double transfer of the ForSub1 shares would not result in those shares not qualifying as capital property:

For purposes of subsection 85.1(3), provided that the ForSub1 Common Shares constitute capital property to CanSub1 immediately prior to the transfer of the shares by CanSub1 to CanSub2 … the transfer by CanSub1 of the ForSub1 Common Shares to CanSub2 … and the subsequent transfer by CanSub2 of such shares to ForSub2 … will not, in and by themselves, cause such ForSub1 Common Shares not to be capital property of CanSub2.

The reorganization also included a similar double-transfer of shares of another subsidiary (ForSub3), and CRA provided a similar ruling.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) | spin-off from one sub of public company to another with no streaming of cost base and cross redemption of preferred shares | 519 |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Shares | shares did not lose capital property character on internal spin-off transfer with a view to their further dorp-down | 108 |

21 October 2013 Internal T.I. 2013-0505831I7 - Rollover and subsequent disposition of property

The taxpayer, a Canadian corporation, transferred all its voting and participating shares of Subco, a non-resident subsidiary wholly-owned corporation, to Forco (another controlled foreign affiliate) in consideration for shares of Forco. Forco also exercised an option to acquire IP from a group member. Forco sold its IP to an arm's length US purchaser ("Purchaseco") and another company in the Purchaseco group, and then sold all its shares of Subco to Purchaseco.

In finding that s. 69(11)(b) did not apply to deny a rollover under s. 85.1(3) for the drop-down of Subco to Forco, the Directorate stated:

The fact that there is no tax payable under the Act by Forco with respect to its gain on the disposition of the Subco shares is due to the fact that the disposition does not result in any income under the Act (Forco is simply not subject to tax under subsection 2(3) of the Act), not because an exemption from tax payable under the Act is available to Forco. Consequently, paragraph 69(11)(b) of the Act would not apply… .

The Directorate went on to state:

[A] court would probably be reluctant to apply subsection 69(11) of the Act to deny the benefit of the 85.1(3) rollover where the conditions to apply subsection 85.1(3) of the Act are met (considering paragraph 95(6)(b) of the Act) and where subsection 85.1(4) of the Act does not apply in a particular situation.

S. 85.1(4) was not considered here because there was to be a separate referral on that issue.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(11) - Paragraph 69(11)(b) | s. 69(11)(b) inapplicable to s. 85.1(3) drop-down of CF1 to CF2 followed by sale of CF1 "exempted" by s. 2(3) | 259 |

2010 Ruling 2010-0373801R3 - Conversion from a BV to a DC

Proposed Transactions

Holdco (resident in Canada) transfers a portion of its shares of a Netherlands private limited liability company (“BV”) to a newly-incorporated Canadian subsidiary (“Newco”) under s. 85(1), following which BV is converted to a Dutch cooperative (“DC”), as a result of which all the shares of BV are cancelled and Holdco and Newco automatically become members of DC holding membership interests in proportion to their previous respective shareholdings. The parent of Holdco (“Canco”) then transfers shares of directly-held foreign affiliates (“FAs”) to Holdco in consideration for Holdco shares, and Holdco then transfers such FA shares to DC (and to Newco under s. 85(1)) in consideration for an increase to its membership interest in DC by an amount equal to the FMV of such transferred shares (and for the issuance of Newco shares – with Newco then dropping down its FA shares to DC in consideration for a correlative increase in its membership interest).

Rulings

Including that Holdco and Newco are each considered to own shares of DC in the indicated respective proportions, and that s. 85.1(3) will apply to their respective drop-down transactions on the basis that they received treasury shares of DC.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(4) - Direct Equity Percentage | 46 | |

| Tax Topics - Income Tax Act - Section 86 - Subsection 86(1) | exchange of shares in Netherlands BV for membership interests in Dutch coop qualified under s. 86 | 147 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Share | membership interest in Dutch coop a share | 139 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | conversion of Netherlands BV to Dutch co-op | 97 |

Articles

Tasso Lagios, Arda Minassian, "Foreign Accrual Property Income: Pitfalls for the Unwary", 1999 Conference Report, c. 3.

R. Ian Crosbie, "Canadian Income Tax Issues Relating to Cross-Border Share Exchange Transactions", 1997 Corporate Management Tax Conference Report, c. 12.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(8) | 0 |

Schwartz, "Tax-Free Reorganizations of Foreign Affiliates", 1984 Canadian Tax Journal, November-December 1984, p. 1039.

Subsection 85.1(4) - Exception

Administrative Policy

25 October 1994 External T.I. 9414095 - TRANSFER OF SHARES OF FOREIGN AFFILIATE (HAA 6363)

S.85.1(4) will not apply where Canco, which owns 100% of USco, transfers its shares of USco for fair market value consideration to a U.S. holding company ("Holdco") that also is a foreign affiliate of Canco, and Holdco then issues common shares to the public and has some of its shares sold by Canco to the public.

Articles

Bryan Leslie, "Proposed Amendments to Subsection 85.1(4)", International Tax Highlights, Vol. 4, No. 4, November 2025, p. 5

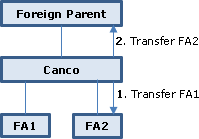

Example 1 of the operation of s. 85.1(4)

- A non-resident corporation (“Foreign Parent”) wholly owns Canco, which in turn wholly owns two controlled foreign affiliates, FA1 and FA2.

- Canco disposes of the shares of FA1, which have an accrued gain, to FA2 in exchange for shares of FA2. Subsequently, Canco disposes of all or a portion of its shares of FA2 to Foreign Parent in a transaction that is fully taxable for ITA purposes.

- If it is determined that the initial and subsequent dispositions are part of the same series of transactions, the subsequent disposition of the FA2 shares by Canco to Foreign Parent should be considered a “relevant disposition” under proposed s. 85.1(4)(a)(i)(C) on the basis that the shares of FA2 would, at the time of disposition by Canco, derive a portion of their fair market value (FMV) from the shares of FA1.

- Furthermore, Foreign Parent would be an acquirer described in proposed s. 85.1(4)(a)(ii)(B) because, during the testing period commencing with the disposition of the FA1 shares and ending immediately after the series of transactions, Foreign Parent is a non-resident person not dealing at arm's length with Canco and that is not a controlled foreign affiliate (CFA) of Canco described in s.17 (a “s. 17 CFA”).

- Accordingly, the s. 85.1(3) rollover would be inapplicable to Canco’s disposition of its FA1 shares.

- Note that even if this were the case, the corporate reorganization exception in s. 212.3(18)(b)(ii) could still apply to prevent the foreign affiliate dumping rules from applying to that disposition, given that s. 212.3(18)(b)(ii) is read without reference to s. 85.1(4).

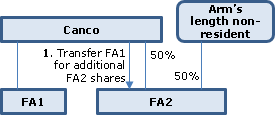

Example 2

- Canco owns all the shares of FA1 (a CFA) and 50% of the only class of shares of a non-controlled foreign affiliate, FA2. The remaining 50% is owned by a non-resident of Canada who deals at arm's length with Canco.

- Canco disposes of the shares of FA1, on which it has an accrued gain, to FA2 solely in exchange for additional shares of the same class of FA2.

- The draft s. 85.1(4) rule is expected to deny the s. 85.1(3) rollover:

- First because the disposition of the shares of FA1 would be considered a “relevant” disposition under proposed s. 85.1(4)(a)(i)(A) (whose definition includes a disposition of the rolled FA shares themselves).

- Second, that relevant disposition is made to an acquirer described in proposed s. 85.1(4)(a)(ii)(B) because: (i) FA2 is a non-resident person with whom Canco does not deal at arm's length at the time immediately after the disposition of the shares of FA1 to FA2; and (ii) FA2 is not a s.17 CFA of Canco at the time of the disposition of the FA1 shares (and instead, only became a s. 17 CFA of Canco immediately after that disposition).

Joint Committee, "August 2022 legislative proposals relating to the Income Tax Act and the Income Tax Regulations", 16 February 2023 Joint Committee Submission

Elimination of purpose test (p. 2)

- Given the breadth of the “series of transactions” concept, the proposed elimination of the purpose test could result in significant uncertainty.

Switch to carve-out for s. 17 CFAs (pp. 2-3)

- While the intention was to limit the opportunity for tax-deferred “out-from-under transactions,” moving from the current qualifying interest (votes and value) test to a voting control test (based on CFA status) could potentially facilitate avoidance transactions.

Application of subsequent disposition rule to dispositions by Canadian taxpayers, and lack of proportionality (p.3)

- Relevant subsequent dispositions should not extend to dispositions of foreign affiliate shares by a Canadian taxpayer (even if such shares derive value from the shares of the first affiliate) - nor to dispositions of shares of the Canadian taxpayer or of shares further up the chain.

- Further, proportionality should apply, so that a disposition of shares of another foreign affiliate deriving any of their FMV from the shares of the first affiliate (or substituted property) only leads to a denial of rollover treatment on a proportionate basis.

Excluded property test should be applied only once at time of subsequent disposition (pp. 3-4)

- The excluded property test should be applied regarding the excluded property status of the property that is disposed of on the subsequent disposition, and the (existing) requirement to test the excluded property status of the property of the first affiliate at the time of the initial transfer should be eliminated.

David Bunn, Mark Dumalski, "Proposed Amendments to Subsection 85.1(4)", International Tax Highlights, Vol. 1, No. 2 November 2022, p. 6

Target of current s. 85.1(4) (p. 6)

- The current version of s. 85.1(4) avoids deferral of the capital gain that would otherwise be realized on the outright sale of a directly held FA (the first affiliate) through transferring it under s. 85.1(3) to a second affiliate, which then sells the first affiliate shares to a subsequent acquiror – where the first affiliate shares are excluded property so that such sale occurs on a deferred basis.

Elimination of purpose test, reliance on “series" test (p. 7)

- The current purpose test is eliminated.

- Instead, there is simply a requirement that the initial transfer be part of a series of transactions that includes another disposition of the first affiliate shares (or certain other properties that derive a portion of their value from such shares.)

- For two events to be part of the same series, one needs to be undertaken “because of” or “in relation to” the other, and the connection between the events needs to be closer than an extreme degree of remoteness or a mere possibility (OSFC Holdings and Copthorne).

Expanded non-permissible subsequent acquirors (p. 7)

- Rollover treatment is now denied not only where the subsequent acquiror is an arm’s-length person, but also where it is a non-arm’s-length non-resident person, other than a controlled FA of the taxpayer (within the narrower s. 17 meaning).

- This expansion presumably is intended to address. 85.1(3) being used as a means of moving a directly held FA out from under Canada on a tax-deferred basis.

- Providing a carve-out for subsequent FA acquirors only where they are controlled by the taxpayer and other non-arm’s-length Canadian residents represents an abandonment of a “votes and value” test in favour of a test of voting control – which could open up opportunities to transfer the economics associated with the ownership of an FA (but not its de jure control) out from under Canada.

Expansive substituted or indirect property test (pp. 7-8)

- The expansion of s. 85.1(4) to encompass a subsequent disposition of any property that is substituted for the share of the first affiliate, as well as any other property any of the FMV of which is derived, directly or indirectly, from the first affiliate shares is inappropriately broad.

- For example, the transfer of the first affiliate from a Canadian corporation to a second affiliate followed by an outright sale of the second affiliate by the Canadian corporation is caught, even where such subsequent disposition is fully taxable in Canada.

- Second, the transfer of the first affiliate by a Canadian corporation to a second affiliate, followed by an outright sale of the Canadian corporation by its shareholders, is caught because the FMV of the Canadian corporation’s shares is derived, in part, from that of the first affiliate shares.

- Third, if all of the first affiliate shares are transferred to the second affiliate for 100 shares of the second affiliate, and then to the third affiliate for 100 shares of the third affiliate, following which only one share of the second affiliate is sold to a subsequent acquiror, rollover treatment would be denied for all (rather than only 1/100) of the first affiliate shares because the single share derived a portion of its FMV from each first affiliate share.

Timing of testing for excluded property (p. 8)

- The requirement for excluded property status can now be satisfied if either (i) all or substantially all of the property of the first affiliate is excluded property at the time of the initial transfer, or (ii) the first affiliate shares are excluded property at the time of the subsequent disposition.

- The addition of the second test addresses a transfer of a first affiliate with property that includes non-excluded property to a second affiliate, which is purified, and then sold to a subsequent acquiror at a time when the first affiliate shares are excluded property.

- That said, all or substantially all of the property of the first affiliate might be excluded property at the time of the initial transfer, but the first affiliate shares, or any other shares deriving their value from such shares, could not be excluded property at the time of the subsequent disposition – in which event, the initial transfer would be denied rollover treatment even though the subsequent disposition triggered FAPI.

Paragraph 85.1(4)(a)

Subparagraph 85.1(4)(a)(i)

Articles

Joint Committee, "August 15, 2025 Legislative Proposals", Submission of the Joint Committee dated 15 September 2025

Property Carve-Outs

- S. 85.1(4) excludes rollover treatment for a drop-down described in s. 85.1(3) where there is a “relevant disposition” as part of the same series of the rolled-down shares, property substituted therefor or of property deriving any portion of its FMV from such shares or property – but with a narrow exclusion (i.e., carve-out) for dispositions of shares of a Canadian-resident corporation.

- Detailed examples are provided to illustrate the proposition that this carve-out rule in s. 85.1(4)(a)(i) (and a similar rule in s. 87(8.3)(b)) should be expanded to include dispositions of property by a Canadian taxpayer (given inter alia that this generates tax to the Canadian system), and dispositions of some types of non-share property such as indebtedness also should not be problematic.

- An exception should also be included in s. 85.1(4)(a)(i)(B) for non-share consideration described in s. 85.1(3)(a), so that the transfer of such non-share consideration (or property that derives its value from such non-share consideration) would not affect the application of s. 85.1(3).

Clause 85.1(4)(a)(i)(B)

Articles

Joint Committee, "August 15, 2025 Legislative Proposals", Submission of the Joint Committee dated 15 September 2025

Exception for s. 17 CFAs

- S. 85.1(4)(a)(ii)(B) describes one of the “bad” transferees for purposes of what is a relevant disposition, namely, a non-resident who is not at arm’s length with the taxpayer throughout the series, but with a safe-harbour carve-out for a controlled foreign affiliate (CFA) of the taxpayer as described in s. 17.

- This carve-out is problematic because it requires that such CFA not deal at arm's length with the taxpayer throughout the series.

- For example, where Canco acquires a foreign corporation (CFA2), which thus would not be a CFA at the commencement of the series, and then contributes CFA2 to an existing CFA, CFA2 would not be a CFA of Canco prior to the acquisition of CFA2 for purposes of the above carve-out (and also would not be dealing at arm's length with Canco immediately before the beginning of the series for purpose of the carve-out in s. 85.1(4)(a)(ii)(A)(I)).

- Where there is a merger of CFAs of Canco, there is no continuity rule deeming the merged corporation to be a continuation of the predecessors. As a result, it could not be considered to be an s. 17 CFA for purposes of the portion of the series preceding such merger.

Subsection 85.1(5) - Foreign share for foreign share exchange

Administrative Policy

23 August 2016 External T.I. 2015-0614981E5 - Foreign Share for share Exchange

Shares of a foreign public company (“Foreign Target”) were exchanged by a Canadian partnership (“Vendor”) for treasury shares of another foreign public company (“Foreign Purchaser”) and cash. Although the cash received for each share tendered was specified in the offer, the fraction of the total consideration that it represented could not be determined until the date of the exchange because the total exchange consideration was dependent upon the average trading price of Foreign Purchaser’s shares immediately before the exchange. Except respecting the treatment of the cash consideration, all the s. 85.1(5) conditions were satisfied. Was the s. 85.1(5) rollover applicable?

CRA quoted S4-F5-C:

Subsection 85.1(1) may apply where a vendor receives newly issued shares of the purchaser and non-share consideration for each exchanged share. The purchaser’s offer must clearly indicate which fraction of each exchanged share is exchanged in consideration for the newly issued shares of the purchaser and which fraction of each exchanged share is exchanged for non-share consideration.

and then stated:

[W]e note that the position in point 2 of paragraph 1.7 [of S4-F5-C1] would equally apply to a foreign share for share exchange… . Nonetheless, where the purchaser’s offer does not clearly specify the fractional information noted in point 2 of paragraph 1.7 of the Folio…the requirements of 85.1(5) will not be met in a situation where a vendor receives newly issued shares of the purchaser and non-share consideration for each exchanged share.

19 June 2000 Internal T.I. 2000-0027787 - OPTIONS, ROLLOVER

Where a U.S. public company of which the taxpayer's employer was a Canadian subsidiary merges with another corporation, s. 85.1(5) will not provide rollover treatment in respect of the issuance of shares by the merged corporations to the taxpayer in exchange for his employee stock option rights.

Articles

Ken Snider, "Share for Share Exchanges — Subsection 85.1(5) Revisited", International Tax (Wolters Kluwer CCH), No. 114, October 2020, p. 5

Potential deeming of shares of non-resident to be taxable Canadian property (TCP) (p.5)

Where the Exchanged Foreign Shares are taxable Canadian property ("TCP") to the vendor, the Issued Foreign Shares are deemed to be TCP at any time within 60 months after the exchange. This could arise, for example, if a non-resident is disposing of shares of a non-resident corporation whose sole asset is shares of a Canadian corporation whose principal asset is Canadian real property or a Canadian resource property.

Christopher Steeves, "Foreign Share Exchanges and Foreign Spinoffs", The Taxation of Corporate Reorganizations, 2001 Canadian Tax Journal, Vol. 49, No. 4, p. 1066.

Subsection 85.1(7) - Application of subsection (8)

Articles

Mitchell, Sherman, "SIFT Update - Conversions and Normal Growth", Corporate Finance, 2009, p. 1678.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107 - Subsection 107(3) | 0 | |

| Tax Topics - Income Tax Act - Section 88.1 - Subsection 88.1(2) | 0 |

F. Brent Perry, "Income Trusts: Reorganiations and Planning for 2011", 2008 Conference Report.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88.1 - Subsection 88.1(2) | 0 |