Cases

Canada v. Hutchison Whampoa Luxembourg Holdings S.À R.L., 2025 FCA 176, aff'g sub nom. Husky Energy Inc. v. The King, 2023 TCC 167

Regarding the CRA decisions to not only assess the dividend payer under s. 215(6) but also make “protective assessments” of the dividend recipients under s. 212(2), Goyette JA stated (at para. 106):

The Crown’s position is troubling as it seemingly contradicts the Minister’s statutory duty to assess and make decisions based on the facts and the law and to not make deals or take positions that are divorced from these considerations [citing inter alia Harris and Galway] … .

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 10 | a securities loan between residents of two Treaty countries did not change the beneficial ownership of the transferred shares | 345 |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(2) | Tax Court finding that the recipient of a dividend for s. 212(2) purposes was other than the dividend’s beneficial owner was potentially troubling | 222 |

| Tax Topics - General Concepts - Substance | agreements styled as securities lending agreements were not such in their legal substance | 202 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(1) | CRA assessments of dividend payer under s. 215(6) and “protective assessments” of dividend recipients under s. 212(2) were “troubling” in light of Galway principle | 239 |

Cardinal Meat Specialists Ltd. v. Devereux, 92 DTC 6357 (Ont CA)

The respondent, which failed to withhold income tax on a payment to the appellant, was entitled under s. 215(6) to recover from the respondent the amounts of income tax which it paid on her behalf.

See Also

3792391 Canada Inc. v. The King, 2023 TCC 37 (Informal Procedure)

The taxpayer was assessed under s. 215(6) for failure to withhold and remit Part XIII tax on rents paid by it in its 2011 to 2016 taxation years to its lessor, Ms. Trimarchi, who lived in Italy (and who had acquired the leased property before the years in issue from some apparently-resident siblings). St-Hilaire J quoted with approval (at para. 38) the statement in J.K. Read that:

Subsection 215(6) of the Act is a charging provision that makes the payer liable for the payee's tax if the payer fails to deduct or withhold at the time of payment tax that is payable by the payee. In contrast, subsection 227(8) of the Act is a penalty provision. A due diligence defence can be mounted against the latter but not the former.

St-Hilaire J further added (at para. 42):

[W]hen the legislator wants to limit a resident’s liability to circumstances where they have knowledge or belief, it expressly does so.

Although the taxpayer was able to point to some minor indicators suggestive of Canadian residence of Ms. Trimarchi (e.g., a Canadian bank account to receive the rent payments, a Canadian SIN, and a Montreal address shown on some documents), the preponderance of the evidence (presented by the Crown, even though the onus was not on it) suggested that Ms. Trimarchi was a non-resident.

The assessments under ss. 215(6) (and 227(8)) were confirmed.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 227 - Subsection 227(8) | taxpayer failed to establish a due diligence defence | 281 |

Solomon v. The Queen, 2007 DTC 1715, 2007 TCC 654 (Informal Procedure)

After noting that the University of Waterloo and Human Resources and Development Canada had failed to withhold Part XIII tax on pension income and Canada Pension Plan and Old Age Security payments made to the taxpayer, Miller J. stated (at para. 9):

"Subsection 215(6) does not shift a tax burden to the University of Waterloo and the HRDC. The University of Waterloo and the HRDC are liable for the tax they failed to deduct; however, this does not aid Mr. Soloman as both entities can recover the taxes from him."

Havlik Enterprises Ltd. v. MNR, 89 DTC 159, [1989] 1 CTC 2262 (TCC)

Sales contracts which the Canadian taxpayer ("Havlik") entered into with a Chinese supplier required Havlik to obtain irrevocable letters of credit in favour of the seller. When a particular letter of credit was due, the bank would draw the face amount of the letter of credit from Havlik's account and make payment to the supplier.

It was held that a failure of the bank to withhold from payments made under amended versions of the letters of credit in respect of interest gave rise to liability to Havlik because under s. 215(6), the debtor and the person who paid or credited an amount on behalf of the debtor are jointly liable.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(b) | 100 | |

| Tax Topics - Income Tax Act - Section 215 - Subsection 215(2) | meaning of "or otherwise" | 67 |

Administrative Policy

2013 Ruling 2013-0488291R3 - Reorganization of Corporations - Rollover

Background

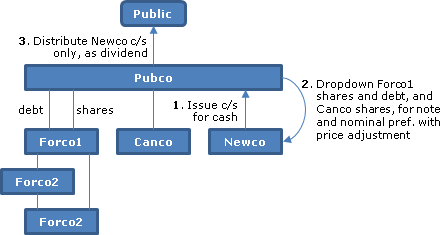

Pubco (a Canadian public company) wishes to spin-off Canco and Forco1 (a foreign affiliate) to its shareholders without incurring the expense of a plan of arrangement or holding a shareholders' meeting.

Proposed transactions

- Pubco will incorporate Newco (a taxable Canadian corporation) and subscribe for common shares.

- Pubco will transfer its shares of Canco and Forco1, and a loan owing by Forco1, to Newco mostly in consideration for interest-bearing notes of Newco - as well as the issuance of preferred shares with a nominal redemption amount and subject to a price adjustment clause. The agreed amount in s. 85(1) elections will be the fair market value of the transferred properties.

- Pubco will declare and pay a dividend-in-kind to its shareholders consisting of the Newco common shares.

- Pubco will lend cash to Newco for an interest-bearing note.

- "To facilitate the payment of the Part XIII tax associated with the dividend in kind, PUBCO will cause Newco to repurchase shares of its capital stock from the affected shareholder with a value equal to the amount of the withholding tax owing, which will then be remitted to the CRA."

Rulings

Include that s. 84(3) deemed dividends will arise in 5 based on any excess of the repurchased shares' fmv over their PUC.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | no ruling on price adjustment clause | 157 |

| Tax Topics - Income Tax Act - Section 52 - Subsection 52(2) | taxable dividend spin-off of thinly capitalized sub | 299 |

16 November 2011 External T.I. 2011-0419191E5 - Foreign Intermediaries & Canadian Owners

Where a foreign financial intermediary ("FFI") has represented to a Canadian financial institution ("CFI") that the beneficial owners of securities in a subaccount are eligible for a 0% rate of withholding based on Treaty exemptions and CFI later learns that there are Canadian beneficial owners in those accounts, CFI should withhold at a 25% rate as FFI has breached its undertaking to provide a replacement certificate which is accurate.