Cases

Gestion M.-A. Roy Inc. v. Canada, 2024 FCA 16

Various whole life policies on the life of a resident individual (Mr. Roy) were owned by (i) a holding company (“Gestion Roy”), controlled by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | s. 246(1) benefit where a sisterco pays premiums on whole life policies owned by the taxpayer | 288 |

Laliberté v. Canada, 2020 FCA 97

The taxpayer, who was the founder and controlling shareholder of Cirque du Soleil, had been found by the Tax Court to have received a taxable...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | the Cirque du Soleil’s bearing most of the $41.8M cost of a space trip for its controlling shareholder gave rise to a shareholder benefit | 267 |

| Tax Topics - General Concepts - Onus | Tax Court could determine a taxable benefit percentage (different from that assumed by the Minister) based on all the evidence | 304 |

Babich v. Canada, 2013 DTC 5010 [at at 5556], 2012 FCA 276, aff'g 2010 TCC 352

The taxpayer ("Babich") was the sole shareholder of a corporation ("Able") which provided a car exclusively for use (both personal and business)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(e) | 194 |

The Queen v. Robinson, 2000 DTC 6176 (FCTD)

The inadvertent crediting by a company's accountants of an amount to the shareholder loan account owing to the taxpayer rather than to the sales...

Chopp v. R., 98 DTC 6014, [1998] 1 CTC 407 (FCA)

In finding that there was a shareholder benefit conferred when the taxpayer's daughter, while an inexperienced bookkeeper, used corporate funds to...

The Queen v. Fingold, 97 DTC 5449 (FCA)

A holding and management company owned by the taxpayer and his brother conferred a taxable benefit on the taxpayer when it purchased a Florida...

Hrga v. R., 97 DTC 5165, [1997] 2 CTC 172 (FCTD)

The taxpayer, who was the sole beneficial shareholder of a corporation ("Interconserv"), guaranteed a debenture of a partially-owned subsidiary of...

Toma v. The Queen, 95 DTC 5356, [1995] 2 CTC 239 (FCTD)

When one of the two corporations owned by the taxpayer ("Meridian Green") fell into financial difficulty, the taxpayer signed a personal...

Penny v. The Queen, 95 DTC 5083, [1995] 1 CTC 114 (FCTD)

An account receivable owing to a private corporation controlled by the taxpayer was found to have been appropriated by him given the receipt (and...

Cartwright v. The Queen, 94 DTC 6677, [1995] 1 CTC 15 (FCTD)

The shareholder benefit received by the taxpayer as a result of a seasonal residence of the corporation being made available for use by him and...

Winter v. The Queen, 90 DTC 6681, [1991] 1 CTC 113 (FCA)

Where an individual had a company controlled by him sell shares of another corporation to his son-in-law for a sale price that was less than their...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(2) | specific provisions applied before GAAR | 104 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | s. 56(2) inapplicable if actual transferee was taxable on the amount | 171 |

Youngman v. The Queen, 90 DTC 6322, [1990] 2 CTC 10 (FCA)

A corporation owned by the taxpayer and his family built a luxurious home in 1978 at a cost of $395,549 on land which originally had been acquired...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Onus | 85 |

Vine Estate v. The Queen, 89 DTC 5528, [1990] 1 CTC 18 (FCTD)

An incorporated car dealership (Carl Vine Ltd.) which was owned by an individual (Mr. Vine) and his wife contributed monies to fund the operating...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Loss v. Loss | 122 | |

| Tax Topics - Income Tax Act - Section 80.4 - Subsection 80.4(2) | 33 |

Friedland v. The Queen, 89 DTC 5341, [1989] 2 CTC 79 (FCTD)

An individual ("Friedland") carried on his business of economics consulting through a corporation ("SFRA"). When dissatisfied clients brought...

Grohne v. The Queen, 89 DTC 5220, [1989] 1 CTC 434 (FCTD)

The taxpayer, along with other promoters of a company, entered into a "standby agreement" whereby they agreed to purchase shares of the company...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Onus | 37 | |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Employee | 32 | |

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(5) | 149 | |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Shares | taxpayer had not previously acted as a promoter | 64 |

Cooper v. The Queen, 88 DTC 6525, [1989] 1 CTC 66 (FCTD)

With reference to whether an interest-free loan gives rise to a taxable benefit, Rouleau J. stated:

"There is a considerable difference between...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Illegality | income tax consequences attaching to illegal loan | 77 |

| Tax Topics - Income Tax Act - Section 105 - Subsection 105(1) | interest-free loan recognized as obligation rather than benefit | 103 |

R. v. Century 21 Ramos Realty Inc., 87 DTC 5158, [1987] 1 CTC 340 (Ont.C.A.)

The summary conviction appeal court judge indicated that even if shares received by the accused had a value of only $25, the accused should still...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Other Legislation/Constitution - Charter (Constitution Act, 1982) - Subsection 15(1) | 47 | |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | 97 |

Hall v. The Queen, 86 DTC 6208, [1986] 1 CTC 399 (FCTD)

The shareholders of a company ("Quebec") purchased a $453,000 note owing by the company for a purchase price of $250,000, payable in 20...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Debt/ receivables | 161 |

Indalex Ltd. v. The Queen, 86 DTC 6039, [1986] 1 CTC 219 (FCTD), aff'd 88 DTC 6053, [1988] 1 CTC 60 (FCA)

A "shareholder" does not include an affiliate that does not hold shares in the corporation.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Old | 66 | |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(2) | 208 |

Murphy v. The Queen, 85 DTC 5462, [1985] 2 CTC 248 (FCTD)

A company of which the taxpayer and her husband were the shareholders paid for work that was done on the family residence, which was owned by her...

The Queen v. Houle, 83 DTC 5430, [1983] CTC 406 (FCTD)

It was found that since a yacht had been acquired by a company primarily for business entertaining and promotional purposes rather than for the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Tax Avoidance | 30 |

Schlamp v. The Queen, 82 DTC 6274, [1982] CTC 304 (FCTD)

Rent-free accommodation provided by a company to its shareholder with respect to a home constructed by the company was a taxable benefit. $350 per...

The Queen v. Schubert, 80 DTC 6366, [1980] CTC 497 (FCTD)

It was held that the transfer of all the assets of an unincorporated printing-table business by the owner to a company controlled by him entailed...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Other | 36 |

Berbynuk v. The Queen, 78 DTC 6322, [1978] CTC 448 (FCTD)

A company did not report income generated from the sale of scrap metal. Some of the cash so generated came into the hands of the appellant, who...

Perrault v. The Queen, 78 DTC 6272, [1978] CTC 395 (FCA)

The appellant majority shareholder of a company, who agreed to purchase the shares held in the company by a minority shareholder in consideration...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | a single payment can result in income inclusions to 2 taxpayers - the 2nd as a taxable benefit | 91 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | 48 | |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | business continued "on a reduced scale" | 54 |

The Queen v. Ginter, 77 DTC 5274, [1977] CTC 418 (FCA)

A corporation, which was owned by the taxpayer, leased a building from him and made an addition to it. It was found that since it was anticipated...

Steeves v. The Queen, 76 DTC 6269, [1976] CTC 470 (FCTD)

Two individuals who were engaged in the road construction business elsewhere, owned 1/2 the shares of a corporation ("Paving") engaged in that...

The Queen v. Phillips, 76 DTC 6093, [1976] CTC 126 (FCA)

In 1964 the taxpayer acquired all the shares of a company from an individual ("Beaupré") for $12,000 and, as part of that arrangement, caused the...

Rosenblat v. The Queen, 75 DTC 5274, [1975] CTC 472 (FCTD)

In June 1967 a company ("Brilund") agreed to issue shares then worth no more than $120,000 to a non-resident shareholder, in consideration of past...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | 22 | |

| Tax Topics - General Concepts - Fair Market Value - Shares | 50 |

The Queen v. Neudorf, 75 DTC 5213, [1975] CTC 192 (FCTD)

The cost of improvements made by a company to leased building premises owned by its shareholder was included in his income. There was no agreement...

The Queen v. Leslie, 75 DTC 5086, [1975] CTC 155 (FCTD)

In 1959 the taxpayer sold his food storage business having a fair market value of $5,078 to a company of which he was the majority shareholder in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) | 97 |

Huron Steel Fabricators (London) Ltd. v. M.N.R., 75 DTC 5006, [1974] CTC 889 (FCTD)

The Crown's theory was that an arrangement, whereunder (a) the majority shareholder ("Fratschko") of a private company ("Huron") acquired the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Shares | 34 |

Angle v. M.N.R., 74 DTC 6278, [1975] 2 S.C.R. 248

"A tax assessment in respect of a benefit or advantage received is not inconsistent with an obligation to pay for the benefit or advantage where,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Res Judicata | 160 |

Byke Estate v. The Queen, 74 DTC 6585, [1974] CTC 763 (FCTD)

Following the acquisition of the shares of a company by the taxpayers for consideration that included a mortgage given by the company to the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | 77 |

Bernstein v. MNR, 74 DTC 6041, [1974] CTC 4 (FCTD), aff'd 77 DTC 5187, [1977] CTC 328 (FCA)

Pillsbury Holdings did not apply to a sale by a corporation ("Highland") to its individual shareholders of shares of a subsidiary ("Berkam") worth...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Dividend | 73 |

Kennedy v. MNR, 73 DTC 5359, [1973] CTC 437 (FCA)

The taxpayer's company acquired a property at a net cost of $159,000 and converted it for use in a car dealership at a cost of $185,000, so that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Other | 60 | |

| Tax Topics - Income Tax Act - Section 9 - Timing | 70 |

MNR v. Bisson, 72 DTC 6374 (FCTD)

The taxpayer, who was the general manager and one of the two principal shareholders of a bus company ("Hull City Transport") agreed, in settlement...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4) - Paragraph 152(4)(a) - Subparagraph 152(4)(a)(i) | reasonable mistake | 148 |

Guilder News Co. (1963) Ltd. v. MNR, 73 DTC 5048, [1973] CTC 1 (FCA)

The sale in 1964 of shares by a corporation to its sole shareholder at an undervalue gave rise to a benefit to the shareholder notwithstanding...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | 229 | |

| Tax Topics - Income Tax Act - Section 121 | 13 | |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Dividend | 70 |

MNR v. Pillsbury Holdings Ltd., 64 DTC 5184, [1964] CTC 294 (Ex Ct)

In 1953 two subsidiaries of the corporate taxpayer (the majority shareholder) waived the interest that was coming due on two loans they had made...

See Also

Greer v. The King, 2023 TCC 100

Spiro J applied the presumption in s. 181(3) of the Business Corporations Act (NB) that an entry in a share register is, in the absence of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4) - Paragraph 152(4)(a) - Subparagraph 152(4)(a)(i) | failure to consult a tax professional was indicative of negligence | 212 |

Gestion M.-A. Roy Inc. v. The King, 2022 TCC 144, aff'd 2024 CAF 16

The taxpayers were a (i) corporate shareholder (“Gestion Roy”) of a consulting firm (“R3D”) that was majority-owned by a resident...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | s. 246(1) applicable where subsidiary of sister company paid premiums on policy owned by the taxpayer (with such subsidiary, a revocable beneficiary) | 277 |

Jackman v. The Queen, 2022 TCC 73

The taxpayers (Bruce and Nancy) were the shareholders of a corporation (“C.A.B.”) that owned a marina on Vancouver Island. Paul (together with...

Boyd B. Harding v. Her Majesty the Queen, 2022 TCC 3

The taxpayer was the sole shareholder and sole director of a holding company (“654”) which, in turn, was the majority shareholder of a logging...

Le v. Agence du revenu du Québec, 2021 QCCQ 5290

Shortly after coming to Canada from Vietnam, the taxpayer came to be dominated by her aunt, with whom she stayed, and her aunt’s son. She...

Pelletier v. Agence du revenu du Québec, 2021 QCCQ 670 (Court of Quebec)

The ARQ accepted that the helicopter, that the corporate taxpayer (Héli) rented out for use by corporate group members (one of which was involved...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 173 - Subsection 173(1) | the net tax addition for the shareholder benefit from personal use of a corporate helicopter should reflect GAAP depreciation rather than (ITA) depreciable-property class rates | 213 |

Spiegel Sohmer Inc. v. Agence du revenu du Québec, 2021 QCCQ 69

A senior tax partner of a Montreal law firm (“Raich”) sought and received reimbursement from the firm’s management company (Spiegel Sohmer...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Income-Producing Purpose | reimbursing expenses for the wedding of a law firm partner’s daughter were non-deductible to the firm management company | 192 |

Wise v. The Queen, 2019 TCC 196

In September 15, 2010, the taxpayer leased a building to a corporation (“VWM”) of which she and her son were shareholders pursuant to a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | subsequent year’s transactions following a s. 15(1) assessment had no retrospective effect | 221 |

Kyard Capital 2007 Inc. v. Agence du revenu du Québec, 2019 QCCQ 1617

The individual taxpayer (“Fontaine”) was the president and majority shareholder of a corporation (“Kyard”) that earned fees from the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(a) | payment of professional dues was benefit | 152 |

| Tax Topics - General Concepts - Solicitor-Client Privilege | unnecessary to waive privilege in order to substantiate the nature of legal services provided | 143 |

Mikhail v. The Queen, 2019 TCC 49 (Informal Procedure)

A corporation which carried on a pharmacy business paid fees to one of its shareholders for his services as pharmacist and manager and wages to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4) - Paragraph 152(4)(a) - Subparagraph 152(4)(a)(i) | failure to properly account for near-cash rebates was neglect under s. 152(4)(a)(i) | 154 |

Laliberté v. The Queen, 2018 TCC 186, aff'd 2020 FCA 97

The taxpayer, who was the founder and controlling shareholder of Cirque du Soleil, was reassessed a $41.8 million shareholder benefit in respect...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | taxable benefit from one company initially bearing costs of shareholder space trip and then being reimbursed by an Opco | 218 |

Melançon v. The Queen, 2018 TCC 73

The taxpayer, who was the sole shareholder of a (“Gexco”), which used nine employees in its house-construction business. Gexco paid...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | rebooking of “expense” as shareholder advance was retroactive tax planning | 174 |

Rowntree v Commissioner of Taxation, [2018] FCA 182

The taxpayer, an experienced lawyer, received over $4 million in numerous dealings with companies that he controlled and, for most of them, was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | contract must be evinced by documents or conduct | 184 |

| Tax Topics - General Concepts - Evidence | contract must be evinced by documents or conduct |

Engelberg v. Agence du revenu du Québec, 2017 QCCQ 14819

The individual taxpayer (Engelberg) was a shareholder of the corporate taxpayer (“Canada Inc.) and did not deal with it at arm’s length. In...

R. v. Golini, 2016 TCC 174

The taxpayer (“Paul Sr.”) following an estate freeze held preferred shares of the holding company for the family business (“Ontario”)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Sham | sham doctrine did not apply to a "minor pretence" | 338 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | interest deduction on limited recourse loan | 305 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | use of corporate asset to create PUC was abuse of s. 84(1) | 250 |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(1) | policy of 84(1) | 219 |

Latham v. The Queen, 2015 DTC 1104 [at 617], 2015 TCC 75

The taxpayers ("John and Diane Latham") owned a corporation ("Farmers"), which rented out buildings to third parties, and to a related company. In...

| Other locations for this summary | |

|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | deemed dividend not possible where foreclosure eliminated corporations's assets |

Charania v. The Queen, 2015 DTC 1103 [at at 614], 2015 TCC 80 (Informal Procedure)

The taxpayer owned a large portion of the non-voting shares in a corporation ("B&N"). The taxpayer lived in a property that B&N had purchased and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | consideration for transfer to shareholder adjusted without price adjustment clause | 242 |

Rogers Estate v. The Queen, 2015 DTC 1029 [at at 124], 2014 TCC 348

Pursuant to a share appreciation right ("SAR") attached to stock options granted by a public corporation which he controlled and of which he was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(1) - Paragraph 39(1)(a) | capital gain can arise from property which is not capital property | 271 |

| Tax Topics - Income Tax Act - Section 5 - Subsection 5(1) | exercise of stock option surrender plan for FMV was not "remuneration" | 121 |

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(3) - Paragraph 7(3)(a) | s. 7 a complete code for taxation of stock option benefits | 230 |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Options | holding one's employee stock options until just before they expire is not typical of an adventure in the nature of trade | 185 |

Versteegh Ltd & Ors v. Commissioners, [2013] UKFTT 642 (TC)

One company in a group of UK companies (the "Lender") made a loan to a subsidiary (the "Borrower"). The loan terms obligated the Borrower to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Exempt Receipts/Business | taxable share interest on loan held by affiliate | 166 |

Tyskerud v. The Queen, 2012 DTC 1179 [at at 3453], 2012 TCC 196 (Informal Procedure)

The taxpayer's use of her corporation's line of credit to pay down her personal debt resulted in a clear shareholder benefit, and her failure to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 163 - Subsection 163(2) | obvious and substantial shareholder benefit | 58 |

McIntosh v. The Queen, 2012 DTC 1049 [at at 2741], 2011 TCC 579 (Informal Procedure)

The taxpayers were the sole shareholders and employees of a corporation engaged in the business of auto retailing. The corporation compensated...

Canadian Winesecrets Inc. v. The Queen, 2011 DTC 1310 [at at 1742], 2011 TCC 390 (Informal Procedure)

The taxpayer was incorporated by a non-resident individual carrying on a proprietorship. It then acquired assets of the proprietorship (comprising...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Other | 168 |

Boulet v. The Queen, 2010 DTC 1015 [at at 2602], 2009 TCC 261

On September 18, 1998, the two taxpayers agreed that they would incorporate a company (the “Company” – to be owned equally by them) to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Land | binding NAL agreement suppressed land's FMV | 217 |

| Tax Topics - Income Tax Act - Section 54 - Principal Residence | basement apartment was separate from principal residence | 63 |

Potvin v. The Queen, 2008 DTC 4813, 2008 TCC 319 (Informal Procedure)

The provision of a truck to the taxpayer's husband by a corporation of which she was the sole shareholder and he the principal employee was found...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(e) | 86 |

Gestion Léon Gagnon Inc. c. La Reine, 2007 DTC 267, 2006 TCC 682

No s. 15(1) benefit was conferred on the taxpayer when a corporation, ("CFIC") whose common shares were owned as to 55% by the taxpayer's sole...

Dyck v. The Queen, 2007 TCC 458

The taxpayer’s accountant recommended that an investment account (the ED account) held in the name of a corporation controlled by the taxpayers...

Park Haven Designs Inc. v. The Quenn, 2006 TCC 685

A husband and wife (the Jaques) owned a corporation (“Park Haven”) that managed the building of custom homes for customers. A property (the...

Truckbase Corporation v. The Queen, 2006 DTC 2930, 2006 TCC 215 (Informal Procedure)

In finding that the payment by a corporation of professional fees incurred for the preparation of shareholder agreements did not give rise to a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Legal and other Professional Fees | shareholder agreement expenses deductible | 101 |

Colubriale c. La Reine, 2006 DTC 2577, 2004 TCC 578

After finding that a shareholder benefit was conferred on the taxpayer when he transferred a property to a corporation of which he was majority...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Land | 129 |

Roth v. The Queen, 2005 DTC 1570, 2005 TCC 484, aff'd 2007 DTC 5222, 2007 FCA 38

The purported transfer by the taxpayer of an undeveloped project (i.e., of know-how he had developed with respect to a proposed LNG project) was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Incurring of Expense | purported transfer of knowhow to corportion did not entail acquisition of property | 98 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Property | knowhow not propery | 85 |

World Corp. v. The Queen, 2003 DTC 951, 2003 TCC 494

The taxpayer assigned a commission of $3.9 million that was to be paid on a deferred basis by a limited partnership in consideration for the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Other | 184 | |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(9) | 83 |

Dobbin v. The Queen, 2003 DTC 118 (TCC)

The taxpayer was unsuccessful in the submission that a shareholder benefit arising to him, computed as the difference between an imputed rate of...

Foresbec Inc. v. The Queen, 2002 DTC 1786 (TCC), aff'd 2003 DTC 5455, 2002 FCA 186

At the time of the purchase by the taxpayer of a control block of the shares of a public company (Foresbec), it and Foresbec "granted" to the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Sham | documents did not reflect legal reality | 58 |

| Tax Topics - General Concepts - Tax Avoidance | documents did not reflect legal reality | 58 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Income-Producing Purpose | 81 |

Robson v. The Queen, 2001 DTC 1039 (TCC)

Bowman A.C.J. stated (at pp.1043-1044):

"There is a departmental mindset, shrouded in the euphemistic rubric of fiscal symmetry, that says that if...

Davisson v. The Queen, 2000 DTC 2140 (TCC)

A loan made by a corporation of which the taxpayer was the sole shareholder to an insolvent corporation owned by his wife ("Arena") gave rise to...

Safety Boss Ltd. v. The Queen, 2000 DTC 1767 (TCC)

Before going on to find that amounts paid by the taxpayer to its non-resident shareholder and to a non-resident company controlled by him were...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) | 293 | |

| Tax Topics - Statutory Interpretation - Interpretation Bulletins, etc. | 53 |

Pellizzari v. MNR, 87 DTC 56, [1987] 1 CTC 2106 (TCC)

Before going on to find that the taxpayer had received income from employment under s. 5(1) as a result of a corporation of which she was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | 75 | |

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(a) | 112 |

Long v. R., 98 DTC 1420, [1998] 1 CTC 2995 (TCC)

The inadvertent failure of a corporation's bookkeeper to debit the payment of a personal expenditure against the balance for the loan owing by the...

Donovan v. The Queen, 94 DTC 1143, [1994] 1 CTC 2394 (TCC), aff'd 96 DTC 6085 (FCA)

The shareholder benefit to the individual taxpayer from his free use of a Florida residence that he had transferred to a family corporation was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(c) | imputed interest income under barter exchange would arise to extent that an interest-free loan to a corporation would have reduced the s. 15(1) benefit | 245 |

Dale v. The Queen, 94 DTC 1100, [1994] 1 CTC 2303 (TCC), aff'd supra.

At the time of a purported capital dividend on preference shares, the authorized capital of the corporation had not yet been amended to include...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) | shares must be issued within a reasonable time | 232 |

| Tax Topics - Statutory Interpretation - Drafting Style | 93 |

Del Grande v. The Queen, 93 DTC 133 (TCC)

The taxpayer, who was an officer, director and shareholder of two corporations and provided financial and business advice to the other principal...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | majority shareholder not subject to the direction of the minority shareholder | 65 |

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(5) | 114 | |

| Tax Topics - Statutory Interpretation - Specific v. General Provisions | 81 |

Simpson v. MNR, 92 DTC 1912, [1992] 2 CTC 2387 (TCC)

A lump sum of $433,333 received by the taxpayer from a bank was found to have been received in settlement of his claim against the bank for...

Mullen v. MNR, 90 DTC 1551, [1990] 2 CTC 2141 (TCC)

Brulé J. found that s. 15(1) did not apply to a shareholder of a connected corporation in light of the fact that this situation was specifically...

Doyon v. MNR, 90 DTC 1132, [1990] 1 CTC 2242 (TCC)

In rejecting a submission that because the majority shareholder of a plumbing company was (allegedly) aware of the company's payment of personal...

Gendron v. MNR, 89 DTC 582 (TCC)

A corporation engaged principally in the construction business but deriving 6% of its revenues from rental properties, purchased a Florida...

President of India v. La Pintada Companid Navigacion S.A., [1985] A.C. 104

The common law gives the creditor no right to interest on his debt. Such a right can only arise by agreement or by statute.

Cangro Resources Ltd. v. MNR, 67 DTC 582 (TAB)

A payment received by the taxpayer that was stated to be made out of "paid-in capital and paid-in surplus" pursuant to the provisions of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Dividend | distributions out of share premium based on number of shares held were dividends | 231 |

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(1) | distributions out of share premium based on number of shares held were dividends | 231 |

Administrative Policy

19 February 2025 External T.I. 2018-0744821E5 F - Régime d’assurance collective - groupe de personne

A corporation which already offers group insurance (life, health and disability) to all its employees with the premiums paid by them, has created...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(a) - Subparagraph 6(1)(a)(i) | for a 2-person plan, a higher level of benefits for the majority shareholder would suggest that there was an individual policy for him, rather than being a group plan component | 239 |

10 October 2024 APFF Financial Strategies and Instruments Roundtable Q. 1, 2024-1023641C6 - Intercompany loans and taxable benefits

Could CRA confirm that an interest-free loan between two corporations owned by different shareholders does not give rise to a taxable benefit...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | s. 246(1) not engaged by no-interest loan between corporations with different ownership | 122 |

7 May 2024 CALU Roundtable Q. 6, 2024-1007091C6 - Shareholder benefits

Regarding a question on an arrangement under which Holdco and Opco agree to share the premiums on, and the death benefit arising, on a term life...

4 June 2024 STEP Roundtable Q. 2, 2024-1003641C6 - Salary to Family Members

Where a corporation pays wages to an individual employee who is not a shareholder but does not deal at arm’s length with a shareholder and a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1.4) - Paragraph 15(1.4)(c) | application of s. 15(1.4)(c) avoided where s. 5 inclusion to taxpayer | 165 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | s. 248(28) applied where overpayment of wages was a s. 15(1) benefit | 53 |

20 June 2023 STEP Roundtable Q. 10, 2023-0965831C6 - Non-Resident Corporations Owning Canadian Real Estate

A non-resident corporation owned by a non-resident individual purchases a Canadian vacation home that is available for use by that individual and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 214 - Subsection 214(3) - Paragraph 214(3)(a) | Pt. XIII tax is applicable where non-resident corporation makes a Canadian property available to its non-resident shareholder or family | 133 |

7 October 2022 APFF Financial Strategies and Instruments Roundtable Q. 5, 2022-0936301C6 F - Guarantee fee

An individual, a sole shareholder of a corporation, borrows money in order to earn business or property income. To secure his personal loan, his...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(e.1) | one-time fee to subsidiary for mortgaging its property as security for a bank loan to the shareholder would not qualify under s. 20(1)(e.1) | 139 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(e) | one-time fee to subsidiary for mortgaging its property as security for a bank loan to the shareholder could qualify under s. 20(1)(e) | 175 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Business | guarantee or pledge fee is from a service and, therefore, is from an undertaking of any kind whatever | 160 |

3 May 2022 CALU Roundtable Q. 6, 2022-0928841C6 - Segregated Fund beneficiary Designation

Mr. A owns all the shares of a Canadian-controlled private corporation (Holdco) owning a segregated fund insurance policy (the Policy) under which...

2021 Ruling 2020-0847671R3 F - Transfert d'un immeuble

Background

A not-for profit corporation described in s. 149(1)(l) (the “Corporation”) governed by the CBCA acquired a building from a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Land | no demurral re a property’s FMV being suppressed by long-term leases with nil net rents | 247 |

| Tax Topics - Income Tax Act - Section 149 - Subsection 149(1) - Paragraph 149(1)(l) | CBCA corporation which leased its property rent-free to its shareholders presented to CRA as an NPO | 215 |

13 November 2020 Internal T.I. 2020-0864831I7 - Equity award plan and recharge agreement

Under an RSU plan established by the U.S. public-company parent (“USCo”) of CanCo, awards of RSUs are made to participants, including CanCo...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Salary Deferral Arrangement - Paragraph (k) | para. (k) not available where RSUs are granted early in Year 1 and vest 36 months later | 179 |

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(3) - Paragraph 7(3)(b) | s. 7(3)(b) did not apply to recharge agreement reimbursements made to a parent that had the discretion to settle the RSUs in cash | 293 |

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(1) | no agreement to issue shares under an RSU if the company can choose to settle in cash | 139 |

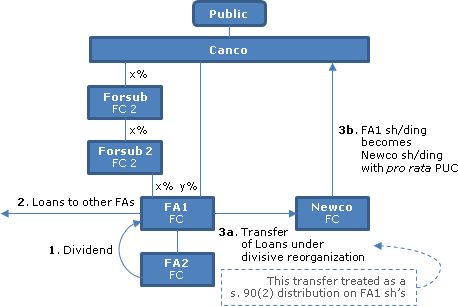

2019 Ruling 2018-0762581R3 - Foreign Affiliate Reorganization

Prior to the formal winding up of CFA2 into CFA1, it sold its assets at their book value (i.e., for less than their FMV) in exchange for a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(2) - Paragraph 5907(2)(f) | Reg. 5907(2)(f) does not apply where inventory is transferred on a foreign rollover basis | 361 |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(2.1) | Reg. 5907(5.1) applicable to pre-wind-up transfer on a foreign tax law rollover basis | 164 |

5 October 2018 APFF Roundtable Q. 14, 2018-0768851C6 F - Avantage imposable découlant de l’utilisation d’un aéronef

IT-432R2, para. 11 indicates that the value of a taxable benefit conferred on a shareholder respecting property made available by the corporation...

AD-18-01: "Taxable Benefit for the Personal Use of an Aircraft" 17 March 2018

This policy on the computation of taxable benefits arising from the personal use of aircraft will be effective for individual taxation years...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(a) | 720 | |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Income-Producing Purpose | non-deductibility where personal use of corporate aircraft by shareholders | 130 |

May 2017 CPA Alberta Roundtable, ITA Q.9

A small business only having employee(s) who are also shareholder(s), establishes a notional health care spending account(s) (a type of “private...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Private Health Services Plan | private health service plan rules generally are not available for a sole shareholder-employee | 186 |

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(a) - Subparagraph 6(1)(a)(i) | HCSA for sole shareholder-employee unlikely to operate as insurance plan | 208 |

May 2016 Alberta CPA Roundtable, Q.15

What is the CRA policy on rental claims by a corporation for use of a workspace in a shareholder’s residence (which, in one instance an auditor...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 67 | deduction by corporation of rents/reimbursements paid for use of office in shareholder’s home | 200 |

2016 Ruling 2016-0630761R3 - Transfer of Shares

A foreign affiliate (New FA) of a Canadian corporation (ACo) transferred all the shares of FA1 to a Canadian-resident subsidiary (BCo) of ACo in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 93 - Subsection 93(1.11) | transfer of an FA with exempt earnings by FA Holdco to Can Subco required to occur at less than the shares’ FMV | 548 |

| Tax Topics - Income Tax Regulations - Regulation 5901 - Subsection 5901(2) - Paragraph 5901(2)(b) | stated capital distribution from FA treated as pre-acq dividend | 188 |

7 October 2016 APFF Financial Strategies and Instruments Roundtable Q. 1, 2016-0651771C6 F - Critical Illness Insurance

CRA noted respecting the transfer for no consideration of a critical illness insurance policy by Opco (which was the policyholder, beneficiary and...

14 March 2016 External T.I. 2016-0626781E5 - Neuman Type Situation

The only issued and outstanding share of Opco (which has retained earnings of $500,000) is 1 Class A common share, with a fair market value of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | s. 56(2) likely non-applicable where spouse subscribes nominal consideration for Opco shares and receives a large discretionary dividend | 262 |

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | Kieboom treated as entailing disposition of right to receive dividends | 340 |

| Tax Topics - Income Tax Act - Section 73 - Subsection 73(1) | spousal rollover for Kieboom disposition of economic interest | 82 |

9 October 2015 APFF Roundtable Q. 4, 2015-0595541C6 F - Computation of taxable benefit

The value of the s. 15(1) benefit arising from the provision of property (e.g., a yacht or luxurious residence) to a shareholder may be computed...

7 October 2016 APFF Roundtable, Q.8

After indicating that the policy in Guide T4130, that the sale of “merchandise” by an employer will not give rise to a benefit from employment...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(a) | policy on employees’ purchases of discounted merchandise excludes condos | 177 |

9 October 2015 APFF Roundtable Q. 13, 2015-0595781C6 F - Reimbursement of attributed income

Most of the income of a partnership has been allocated and distributed to a partner which is a personal trust, but CRA reallocates most of such...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 103 - Subsection 103(1.1) | no secondary adjustments are required for the operation of most income attribution provisions | 117 |

S2-F1-C1 - Health and Welfare Trusts

1.41 Unless the particular facts establish otherwise, there is a general presumption that an employee-shareholder receives a benefit in the...

29 April 2015 External T.I. 2014-0532691E5 F - Vente immeuble - syndicat copropriétaire

After noting that a community of condominium owners is treated by s. 1039 of the Civil Code as a legal person, and is a corporation, CRA went on...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Corporation | community of condominium owners is treated by the Civil Code as a legal person, and is a corporation | 125 |

| Tax Topics - Income Tax Act - Section 149 - Subsection 149(1) - Paragraph 149(1)(l) | a syndicate of condominium co-owners could qualify as a s. 149(1)(l) corporation, so that a capital gain realized by it on a condo sale would be exempt | 151 |

3 March 2015 Internal T.I. 2014-0527841I7 F - Avantage imposable pour aéronef

In a situation where there was personal use of a corporate aircraft by the individual shareholder (Mr. A) of the "grandfather" (indirect parent)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(7) - Paragraph 13(7)(c) | apportionment of aircraft use between business and personal | 74 |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1.4) - Paragraph 15(1.4)(c) | s. 15(1.4)(c) applied to extend scope of Massicotte indirect benefit doctrine | 170 |

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | s. 15(1.4)(c) applied to extend scope of Massicotte indirect benefit doctrine | 857 |

24 September 2014 External T.I. 2014-0522261E5 - Shareholder benefit on leasehold improvements

Q.1

: Is the s. 15(1) benefit arising from improvements made by the corporation to shareholder-owned commercial real estate mitigated if under...

7 August 2014 External T.I. 2014-0528841E5 F - Changement à une résidence principale

A taxpayer renovates the basement of his home by adding a separate door, permitting access from the outside, in order to establish offices there...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 45 - Subsection 45(1) - Paragraph 45(1)(c) | addition of a door to an exterior wall could be considered a structural change triggering a change of use | 136 |

| Tax Topics - Income Tax Regulations - Regulation 1102 - Subsection 1102(5) | Reg. 1102(5) not applicable where door added by tenant to basement rental property | 181 |

11 March 2014 Internal T.I. 2013-0513221I7 F - Stock options

Publico determined to grant stock options to its directors and consultants, as a result of which a private corporation ("Corporation"), that had...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | s. 56(2) benefit where corporation implicitly consented to consultant's options being issued by client directly to its shareholder | 170 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(4) | implicit transfer by corporation when stock options earned by it were issued directly by its client to its shareholder | 175 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | s. 248(28) does not prevent a double income inclusion to corporation under s. 56 and shareholder under s. 15 | 226 |

| Tax Topics - Income Tax Act - Section 9 - Timing | no s. 9(1) income inclusion from consultant being granted stock options until exercise | 226 |

| Tax Topics - General Concepts - Fair Market Value - Options | stock options with no in-the-money value could have nil FMV | 134 |

| Tax Topics - Income Tax Act - Section 52 - Subsection 52(1) | s. 15 benefit due to shareholder receipt of stock options earned by corporation added to the ACB of the exercised shares | 165 |

24 April 2012 Internal T.I. 2011-0400671I7 F - Honoraires professionnels

In finding that the payment by a corporation of fees that had been incurred by its individual shareholder and that did not qualify in accordance...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Start-Up and Liquidation Costs | fees incurred by individual before intention to form a corp did not qualify as pre-incorporation expenses | 486 |

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(1) - Paragraph 40(1)(a) - Subparagraph 40(1)(a)(i) | tax planning fees paid to joint counsel qualified as a disposition expense | 143 |

16 April 2012 External T.I. 2011-0411491E5 - Taxation of distributions of a US LLC

In…2011-0411491E5, CRA commented on an interest in a United States Limited Liability Corporation (LLC) held by an Alberta Unlimited Liability...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | taxable benefit where US taxes on LLC income allocated to indirect Cdn member are paid by LLC or intermediate ULC | 161 |

7 November 2013 External T.I. 2013-0473771E5 - Shareholder of a Not-for-profit corporation

In response to a detailed submission to the contrary, CRA maintained its position under the expanded definition of "shareholder" in s. 248(1)

that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Shareholder | NPO member receiving "shareholder" benefit | 55 |

1 May 2013 Internal T.I. 2009-0321721I7 - Stock Option Recharge on Grant Date

Canco, a Canadian subsidiary of USCo, a publicly traded company, was required under Canadian GAAP to compute the fair value of stock options...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Options | use of Black-Scholes | 142 |

4 December 2013 External T.I. 2012-0465891E5 F - Primes d'assurance / Premiums

When asked whether there would be a taxable benefit where Corporation A, which had other insured employees as well, paid insurance premiums for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(a) - Subparagraph 6(1)(a)(i) | sub plan with only one employee of particular employer could be a group plan if benefits similar to those for employees in other sub plans | 178 |

29 April 2013 External T.I. 2010-0356401E5 - Stock Option Recharge on Grant Date

Under an agreement between a non-resident public company (Parentco) and its wholly-owned Canadian subsidiary (Canco), Canco reimburses Parentco...

19 May 2010 External T.I. 2010-0364131E5 F - Issuance - Discretionary shares

Upon the incorporation of Opco, X subscribed for and continued thereafter to hold all the Class A voting participating shares of Opco, whose terms...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(b) | Kieboom/s. 69(1)(b) rather than s. 15(1) where benefit conferred by shareholder rather than corporation | 185 |

| Tax Topics - Income Tax Act - Section 74.1 - Subsection 74.1(1) | application of Kiebom to consider interest in corp to have been transferred to spouse could engage s. 74.1(1) | 221 |

S4-F3-C1 - Price Adjustment Clauses

CRA will consider a price adjustment clause to represent pricing at fair market value if:

- the agreement reflects a bona fide intention of the...

2012 Ruling 2010-0391281R3 - Incentive Plan - Reimbursement Agreement

underline;">: RSU plan. Parent (which is a US public company) has for a number of years been issuing stock options and restricted stock units to...

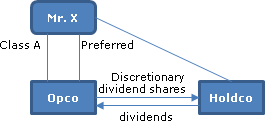

5 October 2012 APFF Roundtable Q. 13, 2012-0454181C6 F - Discretionary Dividend Shares

{kind=link}

Mr. X holds 100 Class A voting participating shares of Opco with a fair market value of $5M and nominal adjusted cost base and paid-up capital....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | general policy against conferring a benefit on a corporation | 205 |

| Tax Topics - Income Tax Act - Section 110.6 - Subsection 110.6(7) - Paragraph 110.6(7)(b) | acquisition by Holdco of discretionary dividend shares of Opco at undervalue could engage s. 110.6(7) application to Opco commons | 208 |

8 May 2012 CALU Roundtable Q. 7, 2012-0435661C6 - Shareholder Benefit - Co-Ownership Life Insurance

Holdco, and its subsidiary Opco, enter into a split-dollar insurance arrangement. They "purchase together permanent life insurance policy on the...

23 January 2012 External T.I. 2011-0409671E5 F - Propriété superficiaire

Corporation A erected, at its expense and for exclusive use in its transport business, a detached garage on the land on which the principal...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Principal Residence - Paragraph (e) | land leased to corporation for business use not part of principal residence | 160 |

| Tax Topics - Income Tax Regulations - Regulation 1102 - Subsection 1102(1) - Paragraph 1102(1)(c) | individual shareholder not entitled to claim CCA on building constructed by the corporation for use in its business even where taxpayer owns it | 160 |

| Tax Topics - General Concepts - Ownership | whether tenant had Quebec right of superficies to garage erected by it determined whether it was its property | 91 |

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(21) - Depreciable Property | building erected by corporation on shareholder’s land not depreciable property unless shareholder renounces right of accession | 223 |

7 October 2011 Roundtable, 2011-0407291C6 F - Group Life Insurance Policy

Professionals practising through a professional corporation hold a group term life insurance certificate as an insured, for which the policyholder...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Capital Dividend Account - Paragraph (d) - Subparagraph (d)(ii) | CDA addition for receipt of proceeds of policy on life of shareholder | 226 |

7 October 2011 Roundtable, 2011-0413281C6 F - Avantage à un actionnaire et assurance-vie

What is the value of the benefit under s. 15(1) where a corporation changes the beneficiary of a life insurance policy on the life of its...

11 February 2011 External T.I. 2010-0360001E5 - Shareholder benefit - single purpose corporation

Does a subsection 15(1) shareholder benefit result from the personal use and enjoyment of an airplane held by a single purpose corporation? CRA...

6 December 2011 TEI Roundtable Q. 5, 2011-0427001C6 - 2011 TEI Q#5 - Distributions from Foreign Corp.

S. 15(1) will not apply to a distribution of a share premium of a foreign affiliate if it is a pro rata distribution governed by draft s. 90(2).

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(3) | 2-step approach | 148 |

24 November 2011 External T.I. 2011-0416791E5 F - Shareholder Benefit

Opco is the beneficiary of a universal life insurance policy (the "Policy") on the life of its sole shareholder, Mr. A, who is the policyholder....

23 June 2011 External T.I. 2011-0397881E5 - 149(1)(l) Entity - Use of Land by Shareholders

In the case of a corporation to which s. 149(1)(l) applied (non-profit corporation for recreation or pleasure), use by a shareholder of corporate...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 149 - Subsection 149(1) - Paragraph 149(1)(l) | 65 |

24 January 2011 Internal T.I. 2010-0389251I7 F - Farm-out agreement and warrants

A mining exploration corporation (the "Purchaser") agreed with another mining exploration corporation (the "Vendor") to acquire an interest in the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 66.1 - Subsection 66.1(6) - Canadian exploration expense - Paragraph (j) | CEE to be incurred under simple farmout reduced by an allocation to warrants issued by farmee | 156 |

| Tax Topics - General Concepts - Fair Market Value - Options | amount allocated out of consideration to “free” warrants based on the greater of their trading and in-the-money value | 191 |

| Tax Topics - Income Tax Act - Section 66.1 - Subsection 66.1(6) - Canadian exploration expense - Paragraph (f) | application of farmout policy to situation where free warrants issued along with incurring of CEE | 214 |

8 October 2010 Roundtable, 2010-0373251C6 F - Immeuble détenu par une société

Youngman, in addressing a shareholder’s personal use of the corporation’s luxury apartment (i.e., where it was difficult to use the...

Memorandum TPM-03 "Downward Transfer Pricing Adjustments Under Subsection 247(2)," 20 October 2003

The Minister may decide not to exercise his discretion under s. 247(10) where a Canadian company requests a decrease in the transfer price of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(10) | 256 |

8 October 2010 Roundtable, 2010-0373311C6 F - Oeuvres d'artistes étrangers

Can works of art of a foreign artist that are listed personal property be held by a corporation without being subject to s. 15(1)? CRA...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Listed Personal Property | art work in corporate boardroom is not personal use property, perhaps also where decorates office | 197 |

| Tax Topics - Income Tax Regulations - Regulation 1102 - Subsection 1102(1) - Paragraph 1102(1)(e) | foreign art work decorating corporate offices is non-depreciable | 129 |

19 November 2009 External T.I. 2007-0257251E5 F - Assurance-vie

The parent corporation is the beneficiary of a life insurance policy while its subsidiary is the policyholder and pays the premiums. Does s....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 148 - Subsection 148(9) - Disposition - Paragraph (d) | disposition by operation of law if there is a new contract | 162 |

| Tax Topics - Income Tax Act - Section 148 - Subsection 148(10) - Paragraph 148(10)(d) | designation of a different beneficiary does not entail a disposition | 132 |

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Capital Dividend Account - Paragraph (d) | CDA addition to beneficiary not reduced by ACB of policy to the different policyholder - but s. 246(1) or 245(2) germane | 195 |

9 October 2009 CTF Roundtable Q. 25, 2009-0329911C6 F - assurance vie, avantage à l'actionnaire

Where Subco is the owner and pays the premiums on a life insurance policy, and the sole shareholder of Subco (Parentco) is the beneficiary, Subco...

2 June 2008 External T.I. 2008-0264161E5 F - Benefit Conferred to a Shareholder

Where the parents of the shareholder of a farming corporation have the exclusive use of a residence owned by the corporation at no charge, is a s....

8 October 2004 APFF Roundtable Q. 8, 2004-0090801C6 F - Benefit to Shareholders

In order for the taxpayers (the children) to fund their obligation to pay support to the divorced wife (Mrs. X) of their deceased father with...

12 February 2007 External T.I. 2006-0214141E5 F - Régime d'assurance salaire

A and B, who are the two 50% shareholders of AB Inc., also are the two salaried managers of AB Inc. All other employees are non-managers. It is...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(a) - Subparagraph 6(1)(a)(i) | a qualifying group disability plan could utilize individual policies, but s. 6(1)(a)(i) exclusion not available where plan restricted to the two shareholder-managers | 302 |

30 August 2004 External T.I. 2003-000135

The only significant asset of FA2 is a loan receivable of $100 owing by its parent, FA1, which is a wholly-owned foreign affiliate of Canco. When...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Accrual Property Income | 199 | |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(g.1) | 37 |

27 March 2008 External T.I. 2006-0200451E5 F - Syndicat de copropriétaires

A not-for-profit condominium syndicate, which CRA found was a corporation, proposed to distribute its land to the members in order to benefit from...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 149 - Subsection 149(1) - Paragraph 149(1)(l) | distribution of land by Quebec condominium syndicate would cause it to lose its NPO status | 65 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Corporation | condominium syndicate described in CCQ Art. 1039 is a corporation | 35 |

6 October 2006 Roundtable, 2006-0197211C6 F - Transfert de police d'ass-vie entre sociétés

CRA has indicated that where a corporation transfers an interest in a life insurance policy of which it is the owner to an individual who is its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 148 - Subsection 148(7) | s. 148(7) applicable to policy transfer between sister corps | 39 |

19 October 2006 Internal T.I. 2006-0173261I7 F - Avantage conféré par une fiducie

A home or cottage is held by a trust with Mr. X and his family as well as a corporation owned by his spouse, as beneficiaries. If that property...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 105 - Subsection 105(2) | no s. 105(2) benefit if no trust income, and benefit to beneficiary would generate a s. 104(6) deduction | 95 |

| Tax Topics - Income Tax Act - Section 54 - Principal Residence - Paragraph (c.1) - Subparagraph (c.1)(iii) | corporation as contingent beneficiary of cottage trust precludes use of principal residence exemption | 200 |

| Tax Topics - Income Tax Act - Section 105 - Subsection 105(1) | tolerance re use of trust personal use property by beneficiary or related person does not extend to unrelated person, but no benefit re payment of interest expense | 379 |

27 June 2006 Internal T.I. 2006-0180031I7 F - Contrat de rente différée - avantage imposable

The Directorate indicated that Holdco did not confer a benefit pursuant to s. 15(1) on its sole shareholder (Mr. X) by acquiring a deferred...

7 April 2006 External T.I. 2005-0152801E5 F - Remboursement de frais de scolarité

In finding that the payment by a corporation of the expenses (tuition, accommodation and travel) for Bob, its sole employee and sole shareholder,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Know-How and Training | bearing costs for its sole shareholder to get an MBA was a capital expenditure | 362 |

30 May 2006 Internal T.I. 2006-0175401I7 F - Assurance-vie donnée en garantie

A corporation acquires a universal life insurance policy on the life of its shareholder, with the amount of the insurance coverage and the cash...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 148 - Subsection 148(9) - Proceeds of the Disposition - Paragraph (b) | use of policy to secure shareholder loan is not a policy loan | 249 |

4 April 2005 External T.I. 2005-0110941E5 F - Transfert d'une police d'assurance-vie

After indicating that the acquisition by a shareholder of an interest in a corporate life insurance policy for less than the fair market value...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 148 - Subsection 148(9) - Adjusted Cost Basis | ACB of life insurance policy transferred to shareholder increased by s. 15(1) benefit | 114 |

11 April 2005 External T.I. 2005-0112321E5 F - Price adjustment clause

An estate freeze entailed the exchange by Mr. A of his common shares of Opco by way of purchase for cancellation for Class A preferred shares with...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 51 - Subsection 51(2) | CRA may accept a price adjustment clause adjusting of share consideration on s. 51 exchange if genuine attempt to establish FMV and issue of intervening share cancellation is addressed | 312 |

| Tax Topics - General Concepts - Effective Date | CRA may also accept a price adjustment clause for improving the attributes of the shares received on an exchange so as to equal the exchange price | 332 |

27 May 2003 External T.I. 2002-0176485 F - regime d'assurance-salaire

A corporation that pays premiums to a wage loss replacement plan for a shareholder/employee. CCRA indicated that this would give rise to a...

2003 Ruling 2002-0174703 - Foreign Affiliate Reorganization

A great-grandchild foreign subsidiary ("Dco") of a Canadian public corporation ("Aco") and a great-grandchild foreign subsidiary of Aco ("Fco")...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | 162 | |

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(2) - Paragraph 53(2)(b) | 166 |

30 November 2004 External T.I. 2004-0090181E5 F - Assurance maladie grave

A corporation purchases a critical illness insurance policy on the life of its sole shareholder and there is also, at an additional cost, a rider...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(1) - Paragraph 39(1)(a) - Subparagraph 39(1)(a)(iii) | no capital gain on receipt by corporation of benefit under a critical illness insurance policy or of refund of premiums | 174 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(h) | premiums paid by corporation for critical illness policy of which it is beneficiary are non-deductible pursuant to s. 18(1)(h) | 320 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Income-Producing Purpose | premiums paid by corporation for critical illness policy of which it is beneficiary are non-deductible per s. 18(1)(a) or (h) | 173 |

29 June 2004 Internal T.I. 2004-0081901I7 F - Taxable Benefit - Life Insurance Premiums

OPCO, which was the policyholder and holder of an insurance policy on the life of its sole shareholder (A), whose wife (B) was the beneficiary,...

3 June 2004 Internal T.I. 2004-0072971I7 F - Taxable Benefit - Life Insurance Premiums

Opco was the policyholder and beneficiary of a life insurance policy on the life of the individual controlling it, and Opco paid the paid the...

31 May 2004 External T.I. 2004-0055141E5 F - Vente de bien à un actionnaire

CRA rejected the apparent proposition put to it that there was no shareholder benefit where a corporation in the residential construction business...

22 January 2004 External T.I. 2003-0006191E5 F - Frais et montant reçus lors de poursuite

A broker was sued for his alleged mismanagement of the portfolios of a holding corporation, its principal shareholder and his RRSP under a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Proceeds of Disposition - Paragraph (f) | damages received for portfolio mismanagement could be proceeds under para. (f) | 87 |

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(1) - Paragraph 40(1)(a) - Subparagraph 40(1)(a)(i) | legal fees for successfully suing broker for portfolio mismanagement would reduce the resulting capital gain on receipt of the damages | 138 |

10 October 2003 Roundtable, 2003-0036865 F - TRANSFER DE POLICE D'ASSURANCE

For the first nine years of a critical illness policy on the life of one of its shareholders, the corporation has been paying the premiums on the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 148 - Subsection 148(7) | s. 148(7) inapplicable to critical illness policy | 20 |

| Tax Topics - General Concepts - Fair Market Value - Other | FMV of critical illness policy takes refundable premium amount into account | 166 |

10 October 2003 Roundtable, 2003-0035385 F - POLICE D'ASSURANCE CONTRE MALADIE GRAVE

A CCPC is the policyholder of a critical illness policy respecting its sole shareholder where either the shareholder is the beneficiary of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Income-Producing Purpose | premiums on critical illness policy are non-deductible to the corporate policyholder even if it is the beneficiary | 85 |

30 June 2003 External T.I. 2003-0182875 F - TRANSFERT DE POLICE D'ASSURANCE

In Scenario 1, a private corporation acquires (and becomes the policyholder of) a permanent life insurance policy on the life of one of its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 148 - Subsection 148(9) - Adjusted Cost Basis | ACB bump on policy distribution to shareholder equal to s. 15 benefit excess over CSV | 206 |

| Tax Topics - Income Tax Act - Section 52 - Subsection 52(1) | ACB bump on policy distribution to shareholder equal to s. 15 benefit in excess of ACB otherwise determined – even in absence of s. 52(1) | 101 |

23 April 2003 Internal T.I. 2003-0008767 F - Benefits Conferred on Shareholders

The corporation built a luxury house on land belonging to its shareholder for his exclusive benefit and use and to his specifications, with its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Personal-Use Property | house provided for use of the corporation’s shareholder (giving rise to s. 15(1) benefit) was personal-use property | 88 |

| Tax Topics - Income Tax Act - Section 46 - Subsection 46(4) | policy of s. 46(4) supported the finding of a shareholder benefit when personal-use property of corporation sold at a loss (representing luxury elements that did not add value) to its shareholder | 238 |

25 April 2003 External T.I. 2002-0171075 F - AVANTAGE-POLICE D'ASSURANCE

A corporation is the owner and policyholder of an individual life insurance policy on the life of an employee or shareholder and names the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(a) | s. 6(1)(a) benefit where employer, as policyholder, pays premiums on policy on life of employee, whose estate is the revocable beneficiary | 191 |

11 March 2003 External T.I. 2002-0179095 F - Issuance-Discretionary Shares non-Consid.

A and B, who were the equal common shareholders of Opco, each had personal holding companies (Holdco A and B) form an equally owned holding...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(b) | issuance of shares at less than FMV to joint Holdco of current shareholders could generate a deemed gain under s. 69(1)(b) | 154 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | s. 56(2) inapplicable to discretionary-dividend shares | 217 |

26 March 2003 External T.I. 2001-0105315 - INTERCORPORATE DEBTS

Respecting the situation where an interest-bearing debt owing by one wholly-owned subsidiary to another wholly-owned subsidiary is exchanged for...

3 January 2003 External T.I. 2002-0143965 - Shareholder Benefit on First Share Issue

Respecting the question as to the consequences of a corporation that had carried on business for 16 years without issuing any shares then issuing...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 52 - Subsection 52(1) | share subscription at under-value | 63 |

Income Tax Technical News, No. 25 (Archived), 30 October 2002

Dividend Reinvestment Plans

A "Dividend Reinvestment Plan" or "DRIP" is an arrangement under which the common shareholders of a public corporation...

22 February 2002 Internal T.I. 2001-0101867 - Shareholder - Loans & 15(1)

Discussion of whether s. 15(1) or 56(2) might apply to loans by corporations wholly owned by an individual to a corporation that was partly owned...

6 February 2002 External T.I. 2001-0105605 - Tax Treatment of Transaction Costs

In response to a question as to whether expenses incurred in response to a takeover bid or sale would give rise to a shareholder benefit when...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Income-Producing Purpose | 129 | |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Legal and other Professional Fees | 91 | |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(bb) | s. 20(1)(bb) not available re fees incurred by target | 54 |

10 January 2002 External T.I. 2001-0112885 F - ASSURANCE-VIE ET PRET REMBOURSE AU DECES

Regarding a life insurance policy pledged by the taxpayer’s corporation to borrow from a bank a series of amounts to be repaid only after the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 148 - Subsection 148(9) - Policy Loan | GAAR could apply where a life insurance policy is pledged for a loan that is not required to be repaid until after death | 84 |

| Tax Topics - Income Tax Act - Section 207.6 - Subsection 207.6(2) | overview of employer use of life insurance policy to fund RCA benefits | 218 |

2001 Ruling 2001-0105883 - reimbursement of stock option benefit

A Canadian controlled private corporation ("Parent") and its U.K. subsidiary ("U.K. Sub") agree that UK Sub will pay to Parent an amount equal to...

20 November 2001 External T.I. 2001-0096865 - Single Purpose Corporations

Respecting the CCRA position on single purpose corporations, it stated that "where each shareholder did not contribute their pro-rata share of the...

9 October 2001 External T.I. 2000-0034915 - REIMBURSEMENT OF STOCK OPTION BENEFIT

Where a subsidiary reimburses its parent for the difference between the fair market value of shares of the parent company on the date of exercise...

28 June 2001 External T.I. 2001-0078935 F - waiving of dividend

Regarding a situation where Dco held a minority shareholding in the corporation (Bco) which directly and indirectly held all its shares and a...

1 February 2001 External T.I. 2000-0008675 F - Avantage-société devenue imposable

A not-for-profit corporation formed under Part III of the Quebec Companies Act that has accumulated surplus will be converted to a for-profit...

16 January 2001 External T.I. 2000-0009685 F - avantage - usage par l'actionnaire

An individual acquired an aircraft solely for personal use through a wholly-owned single-purpose corporation, with the individual bearing all...

6 November 2000 Internal T.I. 2000-0050427 - PRIVATE AIRCRAFT

A company aircraft of the majority shareholder ("Mr. X") of a Canadian-controlled private corporation was used to fly Mr. X, his family and...

2000 Ruling 2000-0001853 - Waived dividends

Waiver of dividends on exchangeable shares did not result in the application of benefit provisions.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | 16 |

1999 Ruling 9902593 - STOCK OPTIONS - CASH-OUT RIGHT

Canadian employees of a Canadian subsidiary of a foreign parent had "subscription rights" to acquire unlisted ordinary shares of the foreign...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(3) - Paragraph 7(3)(b) | use of employee bond to acquire foreign parent share at initial value | 241 |

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(1) - Paragraph 7(1)(b) | cash surrender of subscription rights for unlisted shares | 266 |

2000 Ruling 2000-0001853 - Waived dividends

Ruling that s. 15(1) would not apply to a waiver of dividends on exchangeable shares.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | 17 |

5 January 2000 Internal T.I. 9931817 F - TRANSFER D'UNE POLICE D'ASSURANCE-VIE

A s. 15(1) benefit is conferred when a corporation distributes a life insurance policy to its shareholder to the extent of the excess of the...

2 December 1999 Internal T.I. 1999-0010070 - Guarantee fee

Where a U.S. subsidiary guarantees debts of its Canadian parent without charging a guarantee fee, a benefit under s. 15(1) may apply. Where s....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) | 41 |

16 September 1999 External T.I. 9913250 F - AVANTAGE À UN ACTIONNAIRE

Where a corporation incurs expenses to purify its assets, which would eventually allow some of its shareholders to access the s. 110.6 deduction,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Income-Producing Purpose | asset purification expenses incurred for business reasons of the corporation should satisfy the s. 18(1)(a) test | 66 |

1999 Ruling 9830143 - FOREIGN AFFILIATE - LOAN TO CANADIAN PARENT

An interest-free loan made by a controlled foreign affiliate (that was not resident in a designated treaty country) to its indirect wholly-owning...

14 January 1999 External T.I. 9828555 - CHANGE TO DIVIDEND RATE

Where shares bearing a non-cumulative dividend of 10% are exchanged on an s. 86 reorganization for shares bearing a non-cumulative dividend of...