Subsection 5907(1)

Paragraph 5907(1)(l)

Administrative Policy

5 June 1996 External T.I. 9618035 - INCOME OR PROFITS TAX FOR FOREIGN AFFILIATE RULES

"Income or profits tax" for purposes of the definition of "underlying foreign tax" could include Canadian income tax paid by a foreign affiliate...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Accrual Tax | 52 |

Earnings

Administrative Policy

14 March 2014 Internal T.I. 2013-0499141I7 - IRC 338(h)(10), "earnings" and safe income

After the Directorate found (at para. 232) that the earnings amounts of "US-Opco" foreign affiliates should be calculated similarly to what would...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2) | goodwill gains which accrued prior to purchase of FA and which were included under s. 55(5)(d) did not contributed to gain on Canco shares | 300 |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Exempt Earnings | no carve out for goodwill gains | 142 |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(2) - Paragraph 5907(2)(f) | "notional" deduction arising from Code s. 338(h)(10) step-up of non-purchased goodwill reversed under Reg. 5907(2)(f) rather than (b) | 453 |

5 September 2013 External T.I. 2011-0431031E5 - Guatemala's taxes

A Guatemalan tax on gross revenue was imposed at a rate (for 2013) of 5% up to a low threshold (appx. Cdn. $3,925) and 6% above under the same...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 126 - Subsection 126(7) - Business-Income Tax | 130 | |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Accrual Tax | 107 |

20 May 2011 Roundtable, 2011-0404501C6 - computation of surplus

A US LLC wholly owned by a US corporation, which has not checked the box to be treated as a corporation for US tax purposes, nevertheless has...

5 December 2003 External T.I. 2002-0165195 - Debt Forgiveness in Foreign Affiliates

Where a debt owing by a controlled foreign affiliate to its Canadian parent had financed the acquisition of shares of a U.S. subsidiary in order...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(1) - Paragraph 53(1)(c) | debt forgiveness as contribution to CFA | 100 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) - Commercial Debt Obligation | hybrid (active business/FAPI) debt is commercial debt obligation | 136 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 136 | |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(g.1) | 78 | |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(2) - Paragraph 5907(2)(f) | forgiveness gain did not relate to active business items | 123 |

8 July 1998 External T.I. 9807125 - COMPUTATION OF EXEMPT SURPLUS

A U.S. incorporated company (USco) which is a wholly-owned subsidiary of a corporation resident in Canada (Canco) is deemed to be a non-resident...

80 C.R. - Q.17

Since under the income tax laws of the U.S. and the U.K. a payment made by one Canadian foreign affiliate to another in connection with group...

Articles

Arda Minassian, Kara Ann Selby, "Computation of Surplus Accounts", 2002 Conference Report, (CTF), c. 43

Business in multiple countries (p. 43:6)

If a foreign affiliate carries on a business in multiple countries, the earnings definition may not...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(2) - Paragraph 5907(2)(j) | 111 |

Paragraph (a)

Administrative Policy

27 October 2017 Internal T.I. 2017-0694231I7 - Subsection 247(2), surplus, and FAPI

The Directorate considered that where there was a s. 247(2) transfer pricing adjustment to increase Canco’s income as a result of having...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) | s. 247(2) transfer pricing adjustment for sales undercharges to a CFA does not decrease the ES of the CFA | 166 |

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(1) - Paragraph 53(1)(c) | sale of goods at undervalue to sub does not imply a contribution of capital | 180 |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(2) | effect on surplus balances of foreign transfer-pricing adjustment might be reversed under Reg. 5907(2) | 157 |

Subparagraph (a)(i)

Administrative Policy

24 August 2016 External T.I. 2015-0592921E5 - Computation of Earnings of a Foreign Affiliate

Singco, a Singapore resident which is wholly-owned by Canco, carries on an active business through permanent establishment in each of a designated...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Earnings - Paragraph (a) - Subparagraph (a)(iii) | branch earnings in non-designated country not computed under Singapore tax law until repatriated were computed under ITA rules | 95 |

Articles

Michael Black, "Cross-Border Consolidation and the Foreign Affiliate Rules", Canadian Tax Journal (2017) 65:1, 173-89

CCCTB proposal in European Commission draft EU directive package of October 2016 (pp.175-6)

[I]ncluded in that package is a proposal to revamp the...

Subparagraph (a)(iii)

Administrative Policy

26 April 2017 IFA Roundtable Q. 9, 2017-0691201C6 - Computation of Earnings for LLCs

At the November 30, 2016 CTF Annual Conference, CRA has changed its 2009 view, and now considered that where a foreign affiliate is a disregarded...

24 August 2016 External T.I. 2015-0592921E5 - Computation of Earnings of a Foreign Affiliate

A Singapore company was not required under Singapore income tax law to compute its income from its active business activities carried on through...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Earnings - Paragraph (a) - Subparagraph (a)(i) | a Singapore company recognizing earnings from a foreign branch only on a remittance basis could not measure its “earnings” under Singapore rules | 307 |

29 November 2016 CTF Roundtable Q. 11, 2016-0669761C6 - Computation of Earnings for LLCs

At the 2011 IFA Roundtable, Q.9, CRA indicated that a disregarded U.S. LLC that is a foreign affiliate and has a single member which is a regarded...

Articles

Paul Barnicke, Melanie Huynh, "Earnings of Disregarded US LLC", Canadian Tax Highlights, Vol. 25, No. 2, February 2017, p. 5

Change in treatment of disregarded LLCs in 29 November 2016 CTF Roundtable Q. 11 (p. 5)

[R]etroactive to all FA taxation years ending after August...

Paragraph (b)

Articles

EY, "Revised EIFEL proposals", Tax Alert 2022 No. 43, 10 November 2022

Earnings not subject to EIFEL adjustments (p. 6)

- “Earnings” under para. (b) of the Reg. 5907 definition (essentially, FAPI recharacterized as...

Exempt Earnings

Administrative Policy

14 March 2014 Internal T.I. 2013-0499141I7 - IRC 338(h)(10), "earnings" and safe income

An indirect wholly-owned foreign affiliate ("FA") of Canco made an arm's length purchase of all the shares of "US Holdco," whose wholly-owned...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2) | goodwill gains which accrued prior to purchase of FA and which were included under s. 55(5)(d) did not contributed to gain on Canco shares | 300 |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Earnings | "notional" deduction arising from Code s. 338(h)(10) step-up excluded | 137 |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(2) - Paragraph 5907(2)(f) | "notional" deduction arising from Code s. 338(h)(10) step-up of non-purchased goodwill reversed under Reg. 5907(2)(f) rather than (b) | 453 |

10 March 2011 External T.I. 2008-0302851E5 - Application of subsection 96(1) to capital gains

Where Canco owns all the shares of two foreign affiliates (FA1 and FA2) which, in turn, each hold a 50% interest in a partnership, the exempt...

11 June 2001 Internal T.I. 2001-0074867 F - Définition de gains exonérés pré-96

For taxation years beginning before 1996, the wording of Reg. 5907(11) made no reference to tax treaties and Reg. 5907(11.2) did not apply to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(11.2) | Barbados exempt insurance company is deemed not to be resident in Barbados | 65 |

Paragraph (d)

Administrative Policy

17 May 2022 IFA Roundtable Q. 6, 2022-0929501C6 - Exempt Earnings and Residency Info

Canco receives a dividend from a wholly-owned foreign affiliate (“FA”) that has been carrying on an active business in a Treaty country in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(11.2) - Paragraph 5907(11.2)(a) | residence in country for Treaty purposes does not necessarily establish that its CMC is there | 186 |

24 May 2018 External T.I. 2017-0710641E5 - Interest Charge Domestic International Sales Corp

Exempt earnings of a foreign affiliate include its net earnings from an active business carried on in a designated treaty country if it is...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(11.2) | U.S. IC-DISC is “resident” of the U.S. for Treaty purposes as the U.S. asserts its jurisdiction to tax and grants benefits only on continued meeting of conditions | 395 |

| Tax Topics - Income Tax Act - Section 250 - Subsection 250(5) | whether a corp resident in the U.S. for Treaty purposes is deemed to be resident there for ITA purposes | 40 |

Articles

Joint Committee, "Guidance on International Income Tax Issues raised by the COVID-19", 11 June 2020 Joint Committee Submission

Impact of COVID travel restrictions on DTC residence of FA

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Accrual Property Income | 205 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 5 | 93 | |

| Tax Topics - Income Tax Act - Section 153 - Subsection 153(6) | Impact of COVID travel restrictions on day count tests for qualifying non-resident employee status | 67 |

Subparagraph (d)(ii)

Clause (d)(ii)(A)

Subclause (d)(ii)(A)(I)

Administrative Policy

2015 Ruling 2015-0573141R3 - Subparagraph 95(2)(a)(i)

A Canadian corporation has a U.S. business of purchasing and collecting defaulted or other higher risk debts which, for risk management and state...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(a) - Subparagraph 95(2)(a)(i) | US sub servicing the collection of both its own debt portfolios and that of a U.S. sister was a good mothership to the sister | 360 |

Exempt Surplus

Administrative Policy

23 June 1993 T.I. (Tax Window, No. 32, p. 13, ¶2608)

Where a foreign corporation with a December year-end pays a dividend in June and then becomes a foreign affiliate of a Canadian corporation in...

15 January 1992 Memorandum (Tax Window, No. 15, p. 1, ¶1675)

Where a Canadian subsidiary owns shares in its U.S. parent, a taxable dividend paid to the parent will not be included in the exempt surplus of...

A

Subparagraph (v)

Administrative Policy

2025 Ruling 2024-1030121R3 - FA Inversion

Under a sandwich structure, a Canadian Opco (Cansub) was wholly-owned by Foreign Parentco, which in turn held by both Canadian shareholders...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.1 - Subsection 212.1(1.1) - Paragraph 212.1(1.1)(a) | application to dividend-in-kind of Cansub by foreign parent to new Cdn holdco for foreign parent shareholders | 543 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Accrual Property Income - A - Paragraph (c) | A(c) exclusion for a s. 212.1(1.1) deemed dividend received by the FA on paying a dividend-in-kind of its Cansub to its Cdn Holdco | 245 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Accrual Property Income - B | para. (k) – proceeds of disposition exclusion for a s. 212.1(1.1) deemed dividend received by the FA on paying a dividend-in-kind of its Cansub to its Cdn Holdco | 245 |

Net Earnings

Administrative Policy

21 April 2015 Internal T.I. 2014-0560811I7 - FACL carryback Surplus & PAS election

In 2010, CFA paid the "2010 Dividend" to its 100% parent ("Canco"). On audit, CRA identified that CFA had realized a capital gain (giving rise to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 220 - Subsection 220(3.2) | no relief for late-filed Reg. 5901(2)(b) election | 54 |

| Tax Topics - Income Tax Regulations - Regulation 5901 - Subsection 5901(2) - Paragraph 5901(2)(b) | no relief for late-filed Reg. 5901(2)(b) election | 172 |

| Tax Topics - Income Tax Regulations - Regulation 5903.1 - Subsection 5903.1(1) | FACL carryback from transitional year | 154 |

| Tax Topics - Income Tax Regulations - Regulation 600 | no relief for late-filed Reg. 5901(2)(b) election | 54 |

15 January 1992 Memorandum (Tax Window, No. 15, p. 2, ¶1676)

The U.K. ACT is not an "income or profits tax", although the normal corporate tax payable by a foreign affiliate, before any deduction in respect...

Articles

Tim Barrett, Kevin Duxbury, "Corporate Integration: Outbound Structuring in the United States After Tax Reform", 2018 Conference Report (Canadian Tax Foundation), 18:1-76

No reduction of net earnings of LLC for US taxes paid by corporate member (p. 18:24)

[B]ecause an LLC is not liable to tax in the United States,...

Paragraph (a)

Administrative Policy

15 May 2019 IFA Roundtable Q. 10, 2019-0798781C6 - Foreign Affiliate Earnings and Foreign Transfer Pricing Adjustments

CRA had assessed a Canadian subsidiary (Canco) in a Canadian multinational group under s. 247(2) on the basis that the fees earned by a CFA...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(2) - Paragraph 5907(2)(j) | MAP settlement resulted in reduction in "earnings" - (a)(i) under Reg. 5907(1) but in increase under Reg. 5907(2)(j) | 530 |

2018 Ruling 2017-0729431R3 - Transfer Pricing Adjustment and Earnings

CRA assessed a Canadian subsidiary (Canco 1) in a Canadian multinational group under s. 247(2) on the basis that the fees earned by a sister...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(2) - Paragraph 5907(2)(f) | fictional transfer pricing adjustments did not affect the exempt surplus calculation (other than for the foreign taxes adjustment) | 579 |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) | CRA agreed under MAP to fictional transfer pricing adjustments re NR sister charging NR customer too much and Canco charging too little | 194 |

Taxable surplus

Articles

Michael Black, "Cross-Border Consolidation and the Foreign Affiliate Rules", Canadian Tax Journal (2017) 65:1, 173-89

CCCTB proposal in European Commission draft EU directive package of October 2016 (pp.175-6)

[I]ncluded in that package is a proposal to revamp the...

Underlying Foreign Tax

Administrative Policy

30 October 2014 External T.I. 2013-0488881E5 - Upstream Loan

The disproportionate election under s. (b) of the UFT definition is treated as being applicable for a s. 90(9)(a) notional dividend received by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | no double inclusion following FA creditor wind-up | 60 |

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(3) | notional s. 40(3) gain does not generate surplus | 70 |

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(6) | no double inclusion following FA creditor wind-up or for 2nd loan in series | 121 |

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(9) | notional election and double taxation issues | 1332 |

| Tax Topics - Income Tax Regulations - Regulation 5901 - Subsection 5901(1.1) | notional Reg. 5901(1.1) election | 30 |

| Tax Topics - Income Tax Regulations - Regulation 5901 - Subsection 5901(2) - Paragraph 5901(2)(a) | 90-day rule unavailable | 28 |

| Tax Topics - Income Tax Regulations - Regulation 5901 - Subsection 5901(2) - Paragraph 5901(2)(b) | notional Reg. 5901(2)(b) election | 31 |

28 May 1991 Income Tax Severed Letter 91M05057 F - Foreign Affiliate - Capital Gain on the Disposition of Property

Where a foreign affiliate realizes a capital gain on the disposition of a property that is not excluded property, the taxable portion of the gain...

88 C.R. - Q.12

Foreign tax paid in respect of a capital gain may reasonably be regarded as having been paid in respect of taxable earnings to the extent that...

A

Subparagraph (iii)

Administrative Policy

27 November 1998 External T.I. 9822835 - FOREIGN AFFILIATES - FOREIGN ACCRUAL TAX

The tax paid by a U.S. C.-Corp (which is a foreign affiliate of Canco, the Canadian taxpayer) in respect of its share of the investment income...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Accrual Tax | US tax paid by USco on income of LLC not FAT unless income distributed to USco | 291 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Accrual Property Income | 121 |

Underlying Foreign Tax Applicable

Administrative Policy

{kind=link}

Paragraph (b)

Administrative Policy

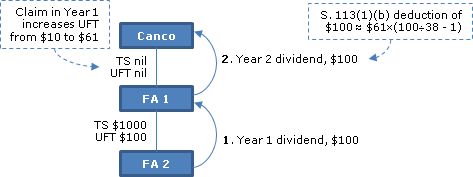

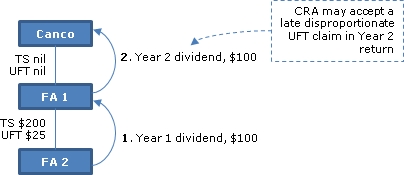

3 April 2013 External T.I. 2012-0460671E5 - Disproportionate UFT election

{kind=link}

In Year 1, FA2, which has no exempt surplus, and taxable surplus and underlying foreign tax of $200 and $25, respectively, pays a $100 dividend...

Articles

Tu Vu, "Application of Disproportionate UFT Election", Canadian Tax Focus, Vol. 11, No. 4, November 2021, p. 15

Taxable income if s. 93(1) dividend and insufficient UFT for full s. 113(1)(b) deduction (pp. 15-16)

- Suppose that Canco owns 100 shares of a...

Subsection 5907(1.03)

Administrative Policy

2022 Ruling 2020-0859851R3 - Foreign accrual tax and underlying foreign tax

Canco wholly-owns a US corporation (FA1), which (with third parties) holds the units of a US limited partnership (USLP1), whose only significant...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Accrual Tax | application of the FAT and underlying foreign tax rules to the investment of a CFA in a US private REIT (holding LLC rental properties) through tiered US partnerships | 645 |

Subsection 5907(1.091)

Administrative Policy

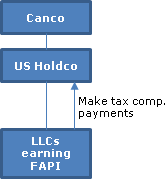

3 March 2023 Internal T.I. 2016-0662221I7 - Tax Sharing Payments made by LLCs

Two LLCs in a US consolidated group beneath Canco made tax compensation payments indirectly to the top CFA in that group in respect of the share...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1.3) | prescribed payments could be made after the taxation years in question and pursuant to an oral tax indemnity agreement | 692 |

Subsection 5907(8)

Administrative Policy

14 January 2026 Internal T.I. 2023-0990701I7 - Application of Reg. 5907(8)(a) in acquisition year

A resident individual wholly owned Canco, and also wholly owned FA1 which wholly owned FA2.

In November of a particular year, FA1 and FA2 were...

Subsection 5907(1.1)

Administrative Policy

22 November 1991 Memorandum (Tax Window, No. 13, p. 9, ¶1608)

Provided that the primary and secondary affiliates are going concerns and the intercompany account has been charged with a number of offsetting...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(2) - Paragraph 5907(2)(j) | 21 |

Subsection 5907(1.3)

Administrative Policy

22 February 2024 External T.I. 2016-0667251E5 - Compensatory payments made to an LLC

The taxpayer, a corporation resident in Canada, wholly owns a “C” corporation resident in the U.S. (“Holdco”), which earns foreign accrual...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1.5) | compensatory payments made by a US C-corp to LLC subsidiary which had no FAPLs were denied under Reg. 5907(1.4), but might be reinstated under Regs. 5907(1.5) and (1.6) | 365 |

3 March 2023 Internal T.I. 2016-0662221I7 - Tax Sharing Payments made by LLCs

Two LLCs in a US consolidated group beneath Canco made tax compensations indirectly to the top CFA in that group in respect of the share of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1.091) | ordering of surplus computation | 243 |

8 April 2004 Internal T.I. 2003-0037291I7 - US LLC and Regulation 5907(1.3)

{kind=link}

A wholly-owned US C-corp subsidiary (US Holdco) of a taxable Canadian corporation wholly-owned two LLCs (US LLC1 and US LLC2), which earned only...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Dividend | 82 | |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Accrual Tax | no deduction for LLC sub income unless distributed | 243 |

Paragraph 5907(1.3)(a)

Administrative Policy

1 February 2018 Internal T.I. 2016-0671921I7 - R&D Services - 95(2)(b) vs 247(2) & 95(3)(b), (d)

Four U.S.-resident controlled foreign affiliates of a Canadian public corporation (“Canco”), namely, CFA1 (wholly-owned by Canco), and CFA2,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(b) - Subparagraph 95(2)(b)(i) - Clause 95(2)(b)(i)(A) | provision of services for fee by CFA to Canco on arm’s length terms did not oust s. 95(2)(b)(i)(A) | 173 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(3) - Paragraph 95(3)(d) | R&D services of CFAs not part of M&P process | 192 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(3) - Paragraph 95(3)(b) | R&D services of CFAs not immediately related to the sale of goods by Canco | 215 |

Articles

Michael Black, "Cross-Border Consolidation and the Foreign Affiliate Rules", Canadian Tax Journal (2017) 65:1, 173-89

CCCTB proposal in European Commission draft EU directive package of October 2016 (pp.175-6)

[I]ncluded in that package is a proposal to revamp the...

Subsection 5907(1.5)

Administrative Policy

22 February 2024 External T.I. 2016-0667251E5 - Compensatory payments made to an LLC

A corporation resident in Canada wholly owns a US “C” corporation (“Holdco”), which earns foreign accrual property income (“FAPI”) and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1.3) | compensatory payments made by a US C-corp to LLC subsidiaries were FAT pursuant to Regs. 5907(1.3) and (1.5) | 315 |

6 February 2015 External T.I. 2014-0542281E5 - Foreign affiliate - prescribed foreign accrual tax

Under the income tax law of "Country X" FA2, its sister, FA3 and FA1, which is the parent of FA2 and FA2 and the wholly-owned subsidiary of Canco,...

Subsection 5907(1.6)

Articles

Adam Freiheit, "Reinstated Foreign Accrual Tax and the Multi-Period Perspective", Canadian Tax Journal, (2015) 63:2, 521-42, p. 521.

General reduction under Reg. 5907(1.4) (p. 523)

[R]egulation 5907(1.3) can prescribe the particular FA's tax compensation payments to other...

Subsection 5907(2)

Administrative Policy

27 October 2017 Internal T.I. 2017-0694231I7 - Subsection 247(2), surplus, and FAPI

The Directorate considered that where there was a s. 247(2) transfer pricing adjustment to increase Canco’s income as a result of having...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) | s. 247(2) transfer pricing adjustment for sales undercharges to a CFA does not decrease the ES of the CFA | 166 |

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(1) - Paragraph 53(1)(c) | sale of goods at undervalue to sub does not imply a contribution of capital | 180 |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Earnings - Paragraph (a) | surplus could be adjusted by transfer-pricing adjustment | 140 |

Paragraph 5907(2)(f)

Administrative Policy

2019 Ruling 2018-0762581R3 - Foreign Affiliate Reorganization

Background

The Taxpayer, a Canadian-resident corporation, wholly-owns CFA1 and CFA2, each of which carries on an active business in Foreign...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(2.1) | Reg. 5907(5.1) applicable to pre-wind-up transfer on a foreign tax law rollover basis | 164 |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | no s. 15(1) application to sale of assets of CFA2 to CFA1 at NBV preliminarily to wind-up | 80 |

2018 Ruling 2017-0729431R3 - Transfer Pricing Adjustment and Earnings

Background and MAP agreement

Canco 1, which was an in direct wholly-owned subsidiary of ACo (a Canadian public corporation), was reassessed by CRA...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) | CRA agreed under MAP to fictional transfer pricing adjustments re NR sister charging NR customer too much and Canco charging too little | 194 |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Net Earnings - Paragraph (a) | MAP downward adjustment to foreign income taxes increased net earnings | 253 |

6 May 2014 May CALU Roundtable, 2014-0523341C6 - CALU - Insurance Death Benefit received by FA

Mr. X, a Canadian resident, owns 100% of Canco which owns 100% of the shares (having a low ACB) of Foreignco, which is required by the income tax...

14 March 2014 Internal T.I. 2013-0499141I7 - IRC 338(h)(10), "earnings" and safe income

An indirect wholly-owned foreign affiliate ("FA") of Canco made an arm's length purchase of all the shares of "US Holdco," whose wholly-owned...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2) | goodwill gains which accrued prior to purchase of FA and which were included under s. 55(5)(d) did not contributed to gain on Canco shares | 300 |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Earnings | "notional" deduction arising from Code s. 338(h)(10) step-up excluded | 137 |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Exempt Earnings | no carve out for goodwill gains | 142 |

5 December 2003 External T.I. 2002-0165195 - Debt Forgiveness in Foreign Affiliates

The U.S. subsidiary ("CFA1") of Canco has non-interest bearing loans payable by it to Canco. The proceeds of those loans had been used by CFA1 to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(1) - Paragraph 53(1)(c) | debt forgiveness as contribution to CFA | 100 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) - Commercial Debt Obligation | hybrid (active business/FAPI) debt is commercial debt obligation | 136 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 136 | |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(g.1) | 78 | |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Earnings | 63 |

Articles

Marc André Gaudreau Duval, Michael N. Kandev, "Foreign Affiliate Issues in Troubled Times", International Tax (Wolters Kluwer CCH), No. 112, June 2020, p. 1

Questionable CRA position that forgiveness does not increase surplus (p. 4)

2002-0165195 … provides that the "exempt earnings" or "taxable...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(g.1) | 338 | |

| Tax Topics - Income Tax Act - Section 91 - Subsection 91(4) | 95 | |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(27) | 79 |

Paragraph 5907(2)(j)

Administrative Policy

15 May 2019 IFA Roundtable Q. 10, 2019-0798781C6 - Foreign Affiliate Earnings and Foreign Transfer Pricing Adjustments

Parent (a Canadian-resident parent of a multinational group) and CFA (resident in a designated treaty country, Country A, and earning active...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Net Earnings - Paragraph (a) | MAP Settlement reduced net earnings when foreign country reassessed to implement income reduction | 310 |

26 May 2016 IFA Roundtable Q. 8, 2016-0642041C6 - s. 95(2)(a)(ii)(B) and borrowing to return capital

Where FA1 borrows $350,000 from a sister (FA3) to make a capital distribution to its Canadian shareholder (Canco) on its Class A common shares,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(a) - Subparagraph 95(2)(a)(ii) - Clause 95(2)(a)(ii)(B) | tracing approach to determining whether interest on money borrowed to return capital is considered for s. 95(2)(a)(ii)(B) to be deductible in computing exempt earnings | 496 |

28 May 2015 IFA Roundtable Q. 11, 2015-0581571C6 - IFA 2015 Q11: Application of clause 95(2)(a)(ii)(B)

"Borrower FA," which exclusively carries on an active business, borrows money from "Lender FA" to pay a dividend in an amount not exceeding its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(a) - Subparagraph 95(2)(a)(ii) - Clause 95(2)(a)(ii)(B) | interest on borrowing to distribute accumulated profits | 248 |

6 March 1995 Internal T.I. 9412216 - ADJUSTMENTS IN THE COMPUTATION OF EXEMPT SURPLUS

Interest paid on overdue taxes must be deducted under Regulation 5907(2)(j) in computing the earnings of a foreign affiliate.

93 C.M.TC - Q. 2

Discussion of treatment of interest paid by one U.S. foreign affiliate to another where only part of the interest paid is deductible under s....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Paragraph 95(2)(a) (historical) | 34 |

20 May 1993 T.I. (Tax Window, No. 31, p. 3, ¶2509)

Where funds are lent by FA1 to a second foreign affiliate (FA2) which carries on business in the U.S., and due to the application of the excess...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Paragraph 95(2)(a) (historical) | 154 |

22 November 1991 Memorandum (Tax Window, No. 13, p. 9, ¶1608)

In the absence of persuasive evidence, charitable donations, political donations and penalties will not be considered to be deductible.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1.1) | 50 |

Finance

16 May 2018 IFA Finance Roundtable, Q.6

After indicating that, in the context of s. 95(2)(a)(ii), interest paid by and to a foreign affiliate whose deductibility was denied under Code s....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(a) - Subparagraph 95(2)(a)(ii) - Clause 95(2)(a)(ii)(B) | the expanded U.S. earnings stripping rule should not adversely affect the operation of s. 95(2)(a)(ii) | 152 |

Articles

Arda Minassian, Kara Ann Selby, "Computation of Surplus Accounts", 2002 Conference Report, (CTF), c. 43

The underlying principle of the regulation 5907(2) adjustments is to determine the amount of assets available to repatriate surplus. Permanent...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Earnings | 248 |

Subsection 5907(2.01)

Administrative Policy

22 April 2015 External T.I. 2014-0550451E5 - Interpretation of paragraph 5907(2.01) of the Regulations.

Does "consideration received" in Reg. 5907(2.01)(a) include any liabilities assumed by a foreign affiliate (the "Receiving Affiliate") on a...

Articles

Samantha D’Andrea, "Packing and Unpacking Proposed Amendments", International Tax Highlights, Vol. 1, No. 2 November 2022, p. 6

Current pack and sale transaction rule (p. 6)

- Reg. 5907(2.01) overrides the non-recognition rules in Regs. 5907(5.1) and 5907(2)(f ) and (j), so...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(3.3) | 191 |

Raj Juneja, Pierre Bourgeois, "International Tax Issues That Get in the Way of Doing Business", 2019 Conference Report (Canadian Tax Foundation), 36:1 – 42

Need to avoid assumption of liabilities on the drop-down transaction in a “pack and sale” transaction

- Reg. 5907(2.01) to some extent...

Subsection 5907(2.02)

Articles

Gwendolyn Watson, "The Foreign Affiliate Surplus Reclassification Rule", Canadian Tax Journal (Canadian Tax Foundation) (2019) 67:4, 1233-66

Example of what the 1992 Auditor General’s Report had in mind as conversion of taxable surplus into exempt surplus (pp. 1242-1243)

Suppose that...

Paul Barnicke, Melanie Huynh, "Exempt Earnings Anti-Avoidance", Canadian Tax Highlights, (Canadian Tax Foundation), Vol. 23, No. 12, December 2015, p. 5

Application of rule to non-rollover reorgs, cf. fresh start rule (p. 5)

The main target of this anti-avoidance rule may be intercompany...

Jenny Li, "The Interaction of the Fresh Start and Surplus Reclassification Rules", International Tax, Wolters Kluwer CCH, April 2014, No. 75, p. 8.

Two conditions under Reg. 5907(2.02) (p. 9)

[T]he "surplus reclassification rule". [fn 5: Regulation 5907(2.02).]…rule reclassifies an amount of...

Subsection 5907(2.03)

Administrative Policy

28 May 2025 IFA Roundtable Q. 6, 2025-1052631C6 - Earnings of a disregarded US LLC

A US LLC, which was formed in 2017 by a regarded US corporation, acquired and used appreciable assets in carrying on its active business in the US...

22 January 2013 External T.I. 2012-0460121E5 - Computation of "earnings" of a foreign affiliate

In taxation year X, the tax regime in Forland changes so that FA ceases to be required under the income tax law of Forland to compute its income...

Articles

Nakul Kohli, Simon Townsend, "Computing UCC for Newly Acquired LLCs", Canadian Tax Focus, Vol. 13, No. 1, February 2023, p. 9

Whether maximum CCA should be treated as having been claimed for pre-acquisition taxation years of an LLC (p. 9)

- US LLC acquired depreciable...

Michael W. Colborne, "Regulation 5907(2.03) and Offshore Metal Streams", Resource Sector Taxation, Volume IX, No. 2, 2013, p. 647.

Description of offshore metal streams transactions (pp. 647-8)

While a detailed description of offshore metal streams transactions is beyond the...

Subsection 5907(2.1)

Administrative Policy

8 October 2010 Roundtable, 2010-0373661C6 F - Calcul de surplus et NIIF

Could the financial statements prepared in accordance with IFRS by a subsidiary of a Canadian public corporation be used with respect to the...

2019 Ruling 2018-0762581R3 - Foreign Affiliate Reorganization

In order to wind-up CFA2 into CFA1 (which is directly held by Canco), CFA2 will first distribute its retained earnings and then sell its assets at...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(2) - Paragraph 5907(2)(f) | Reg. 5907(2)(f) does not apply where inventory is transferred on a foreign rollover basis | 361 |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | no s. 15(1) application to sale of assets of CFA2 to CFA1 at NBV preliminarily to wind-up | 80 |

Articles

Albert Baker, David Bunn, "FAs and the Repeal of the ECP Regime", Canadian Tax Highlights, Vol. 24, No. 9, September 2016, p. 4

Repeal of ECP regime will affect the consequences of the election (p. 4)

Assume for instance that a US business is acquired by an FA of a Canadian...

Paul Dhesi, Korinna Fehrmann, "Integration Across Borders", Canadian Tax Journal, (2015) 63:4, 1049-72

Advantage of book depreciation election (p.1071)

[A]n election is available under regulation 5907(2.1) to use book depreciation rather than tax...

Subsection 5907(2.6)

Administrative Policy

1 March 1991 Memorandum (Tax Window, No. 2, p. 18, ¶1185)

The election cannot be filed late.

Subsection 5907(2.7)

Administrative Policy

27 January 2017 External T.I. 2013-0482351E5 - Clause 95(2)(a)(ii)(D)

CRA indicated that where a loan from one controlled foreign affiliate (FA Finco) of Canco to a second CFA of Canco (FA Holdco) meets the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(a) - Subparagraph 95(2)(a)(ii) - Clause 95(2)(a)(ii)(D) | s. 95(2)(a)(ii)(D) can recharacterize a loan prepayment penalty as active business income | 460 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(9.1) | s. 18(9.1) applied where loan prepayment penalty was equal to PV of interest thereon | 180 |

25 April 1995 External T.I. 9429875 - 6363-1 FOREIGN AFFILIATES DEEMED ABI

Where one U.S. subsidiary ("B") of a Canadian corporation lends money on an interest-bearing basis to a second U.S. subsidiary ("C") of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(a) - Subparagraph 95(2)(a)(ii) - Clause 95(2)(a)(ii)(B) | 72 |

Subsection 5907(5)

Articles

Philippe Montillaud, Grant J. Russell, "Foreign Accrual Tax and Flow-through Entities", International Tax Planning, Volume XVIII, No. 4, 2013, p. 1280

Application of s. 93(2.01) stop-loss rule to DLAD capital loss (p. 1282)

Regulation 5907(5) requires that capital gains and losses for surplus...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 91 - Subsection 91(4.5) | 200 | |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(e) | 389 |

Subsection 5907(5.1)

Articles

Melanie Huynh, Eric Lockwood, "Foreign Accrual Property Income: A Practical Perspective", International Tax Planning, 2000 Canadian Tax Journal, Vol. 48, No. 3, p. 752.

Subsection 5907(6)

Administrative Policy

10 October 2014 APFF Roundtable Q. 24, 2014-0538181C6 F - 2014 APFF Roundtable, Q. 24 - Surplus accounts calculation

Reg. 5907(6) was amended for taxation years commencing after 18 December 2009 to eliminate a prohibition against maintaining surplus accounts of a...

Brian Darling, "Revenue Canada Perspectives" in Income Tax and Goods and Services Tax Considerations in Corporate Financing, 1992 Corporate Management Tax Conference Report (Canadian Tax Foundation, 1993), 5

1-20, question 7, at 5:13:

[w]hat is reasonable in the circumstances can be determined on a case-by-case basis. There are no hard-and-fast rules....

Subsection 5907(10)

Administrative Policy

The Queen v. Old HW-GW Ltd., 93 DTC 5199 (FCA)

Because Puerto Rico was a country distinct from the United States for purposes of paragraphs (b) and (c) of Regulation 5907(10), it followed given...

Subsection 5907(11)

Administrative Policy

1 March 2023 External T.I. 2023-0990821E5 - Definition of Designated Treaty Country

The territorial scope of the income tax Treaty between Country A and Canada specified that the term “Country A” did not encompass its overseas...

1 May 2009 CLHIA Roundtable Q. 4, 2009-0316641C6 - CLHIA Round Table Question #4 - TIEAs

In order for income from an active business carried on by a foreign affiliate to qualify as 'exempt earnings', the affiliate must be resident in a...

7 June 1991 T.I. (Tax Window, No. 4, p. 31, ¶1285)

St. Vincent includes the Grenadine Islands of the Bequia, Mustique, Canouan, Mayreau, Union Island and associated islets which are under the...

Articles

Nathan Boidman, "Canada's Two-Faced TIEAs - Netherlands Antilles Trumps Bermuda", Tax Notes International, Vol. 55, No. 12, September 21, 2009, p. 1023.

Subsection 5907(11.2)

Administrative Policy

24 May 2018 External T.I. 2017-0710641E5 - Interest Charge Domestic International Sales Corp

A Canadian resident public corporation (“Canco”) indirectly owns all of the issued and outstanding shares of a U.S. resident subchapter C...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Exempt Earnings - Paragraph (d) | CMC of FA must be in the DTC and it must be liable to tax therein (albeit, may be conditionally exempted) | 233 |

| Tax Topics - Income Tax Act - Section 250 - Subsection 250(5) | whether a corp resident in the U.S. for Treaty purposes is deemed to be resident there for ITA purposes | 40 |

2013 Ruling 2013-0477871R3 - 5900(1)(a) and dividends from foreign affiliate

{kind=link}

Background

A non-resident subsidiary (ForeignHoldco) of a taxable Canadian corporation (Parent) made a non-interest-bearing loan (the Loan) to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(14) | repayment by set-off against dividend | 91 |

11 June 2001 Internal T.I. 2001-0074867 F - Définition de gains exonérés pré-96

The Directorate noted that, for the purposes of the Barbados-Canada Convention, a corporation resident in Barbados that qualifies as an "exempt...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Exempt Earnings | “resides” in the pre-1976 exempt earnings definition referenced central management and control | 71 |

10 November 1997 External T.I. 9711175 - FOREIGN AFFILIATES - INVESTMENT BUSINESS

A Barbados corporation that had International Business Corporation status in Barbados and that was ineligible for any tax benefit under the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Investment Business | 66 |

1997 A.P.F.F. Round Table , Q. 3.5, No. 9M19020

"Under the IBC Act, a corporation that is not incorporated under the laws of Barbados in which it has a branch that qualifies as an IBC, is...

27 October 1997 External T.I. 9704705 - FOREIGN AFFILIATES - RESIDENCY

A foreign affiliate ("USCO") that was incorporated in the U.S. but operates in Mexico through a branch and has its central management and control...

17 February 1997 External T.I. 9617535 - BARBADOS ENCLAVE ENTERPRISES

The ten-year tax holiday for Barbados Enclave Enterprises would not, by itself, disqualify them from being considered as being resident in Barbados.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 4 | 63 |

18 March 1996 External T.I. 9600675 - treaty residence - barbados insurance companies

A foreign affiliate incorporated in Barbados and licensed under the Exempt Insurance Act, 1983 will not be considered to be "liable to taxation"...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 4 | 73 |

1996 Corporate Management Tax Conference Round Table, Q. 3

Because the term "resident in a designated treaty country" is not defined, a company must be resident in a designated treaty country under...

Paragraph 5907(11.2)(a)

Administrative Policy

17 May 2022 IFA Roundtable Q. 6, 2022-0929501C6 - Exempt Earnings and Residency Info

In order for the net earnings of a foreign subsidiary (FA) from an active business to be included under para. (d) of the Reg. 5907(1) definition...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Exempt Earnings - Paragraph (d) | exempt surplus calculations must be supported by records showing that the FA’s CMC was exercised in a Treaty country | 208 |

13 June 2007 External T.I. 2007-0226261E5 F - Convention Émirats Arabes Unis

Canco incorporated a wholly-owned subsidiary in Dubai, in the United Arab Emirates (Dubai Co), whose management and control, and the sole...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 4 | meaning of “substantially all” in UAE Convention informed by its meaning under ITA | 280 |

| Tax Topics - Treaties - Income Tax Conventions - Article 3 | undefined term in Convention informed by its domestic interpretation by CRA | 36 |

Paragraph 5907(11.2)(b)

Articles

Tina Korovilas, Drew Morier, "Non-Corporate Vehicles in the Foreign Affiliate Context", 2018 Conference Report (Canadian Tax Foundation), 20:1 – 114

LLCs can generate exempt earnings (pp. 20:10-11)

[T]he fundamental requirement—established in paragraph (d) of the “exempt earnings”...

Subsection 5907(13)

Administrative Policy

22 August 2025 External T.I. 2019-0826681E5 - Immigration of a Controlled Foreign Affiliate

CFA1 (incorporated in Country A) wholly owned CFA2 (incorporated in Country B) and was wholly owned by Canco.

Pursuant to s. 128.1(1)(b), at the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 91 - Subsection 91(4) | no FAT generated to Canco when its sub (CFA1) holding the shares of CFA2 with an accrued gain, is continued to Canada, nor when CFA1 subsequently sells CFA2 | 339 |

| Tax Topics - Income Tax Act - Section 128.1 - Subsection 128.1(1) - Paragraph 128.1(1)(b) | gain on the shares of CFA2 (sub of CFA1) on the continuance of CFA1 (a sub of Canco) to Canada could be taxed again when CFA1 actually disposes of the CFA2 shares | 259 |

3 October 2000 External T.I. 1999-001556

In a situation where a foreign affiliate continues into Canada, the Agency indicated that although s. 128.1(1)(b) "may deem certain dispositions...