Subsection 107.4(1) - Qualifying disposition

Administrative Policy

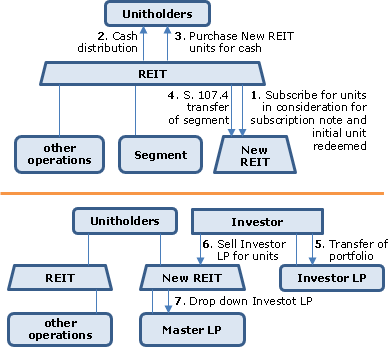

2021 Ruling 2021-0894161R3 - Qualifying Disposition - REIT spinout

Background

The REIT is an open unit trust whose units are redeemable by their holders and which qualifies as a mutual fund trust and real estate investment trust. It is the sole limited partner of a limited partnership (“Master LP”), and is the sole beneficiary of the inter vivos trust (“GP Trust”) that is the general partner.

Master LP holds all the units of a subsidiary trust (the “** Trust”), which directly and through subsidiary partnerships holds rental properties. Certain subsidiary partnerships have exchangeable Class B units.

The REIT recently settled and subscribed for the initial unit of the “New REIT,” which will have similar attributes to the REIT other than having two series of units: Series A voting units, which are expected to be listed; and Series B non-voting units, which will be economically equivalent to and exchangeable for the Series A units.

See also H&R REIT spin-off of Primaris REIT.

Proposed Transactions

The lengthy proposed transactions include the following:

- On the day before the effective date of the Plan of Arrangement, the ** Trust will pay a distribution in kind equal, to its undistributed taxable income for its taxation year ending by virtue of ss. 249(4) and 251.2(6), through the issuance of additional units.

- The REIT will assume the liabilities of Master LP as a contribution of capital, and Master LP will be wound up under s. 98(3), with the resulting undivided interest received by GP Trust being distributed on its winding up in turn to the REIT.

- The REIT will transfer certain directly held properties (the “Legacy Transferred Properties”), to a newly formed limited partnership (“New LP”, with a unit trust wholly-owned by the REIT as the general partner), on an s. 97(2) rollover basis for consideration including the assumption of liabilities and additional partnership interests in New LP.

- The REIT will transfer assets including its units of New LP and the GP thereof to a newly formed partnership (“New Master LP”, with a unit trust wholly-owned unit by the REIT as the general partner (“New Master GP”),) on an s. 97(2) rollover basis and for consideration including the assumption of liabilities and intercompany payables, the issuance of a “New Master LP Note”, and additional partnership interests in New Master LP. Under the transfer agreement, New Master LP will agree to indemnify the REIT and its affiliates in respect of certain guarantees provided by the REIT and its affiliates in respect of the Segment properties (transferred in 8 below) and the REIT will agree to indemnify New Master LP and its affiliates in respect of certain guarantees provided by ** Trust and its subsidiaries in respect of properties that will continue to be held directly or indirectly by the REIT following completion of the Arrangement, in each case, to the extent that such guarantees are not released.

- The REIT will subscribe for additional units of New REIT, equal in number to the number of outstanding REIT units, in consideration for the issuance to the New REIT of the Second Subscription Note, and the initial unit will be redeemed.

- The REIT will make a cash distribution to its unitholders, with the amount thereof paid to a depositary and with the applicable withholding made pursuant to s. 218.3(2).

- The REIT will sell its units of New REIT to the REIT unitholders for a cash sale price satisfied through the payment by them of the cash in the above step. At the time of the sale, essentially the only asset of New REIT will be the Second Subscription Note.

- The REIT will transfer its indirect interest in a particular business segment (the “Segment”) to New REIT by transferring its limited partnership interest in New Master LP, the units of the new Master GP Trust, its remaining limited partnership interest in the New LP, the units of ** Trust, and certain other assets to the New REIT for no consideration (the “REIT Qualifying Disposition”) - with no s. 107.4(3)(a)(i) election made so that the assets are transferred their cost amount. The value of the Segment and the assets retained by the REIT will be such that each of the REIT and the New REIT will have at least 150 unitholders each with a block of units with a fair market value of at least $500.

- The REIT will subscribe for a number of exchangeable units of New Master LP equal to the number of New REIT units which would be required to be delivered to the holders of the existing Class B exchangeable units on the exchange of their units for REIT units and units of the New REIT. The subscription price payable by the REIT for such units will be paid by way of set-off against the amount owing to the REIT by New Master LP under the New Master LP Note. New REIT will simultaneously issue an equal number of special voting units to the REIT for no consideration, with the REIT agreeing to vote them as directed by the holders of the Class B exchangeable units.

- The sole trustee of New REIT will be replaced by the desired board of individual trustees.

- The Investor, which is exempt from Part I tax, will transfer its beneficial interest in the Investor Properties, being a portfolio of properties owned by it, to a limited partnership formed by it (“Investor LP”), in consideration for the assumption of associated liabilities, the issuance of a note (the “Investor LP Note”), and additional partnership units.

- The Investor will transfer its interest as limited partner in Investor LP and its interest in the general partner thereof to New REIT in consideration for Series A voting units and Series B non-voting units.

- New REIT will transfer most of its limited partnership interest in Investor LP and its interest in the general partner thereof to New Master LP in consideration for additional limited partnership units of New Master LP.

- Shortly following the effective date of the Plan of Arrangement, Investor LP will repay the Investor LP Note to the Investor using the proceeds from one or more secured and/or unsecured financings of the Investor Properties.

- The New REIT will make the s. 132(6.1) election when filing its first tax return.

Purpose of transactions

The separation of the Segment into New REIT is expected to maximize unitholder value by permitting the REIT and New REIT to pursue independent objectives and financings. New REIT’s growth strategy as a separate public entity will include the Investor’s investment in it.

Rulings

The REIT Qualifying Disposition will constitute a qualifying disposition within the meaning of s. 107.4(1), so that the s. 107.4(3) rules will apply to the REIT, the New REIT, and the unitholders in respect of all such dispositions.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(2) | REIT spin-off transaction to new REIT likely accomplished through sideways transfer described in s. 107.4(2) | 164 |

| Tax Topics - Income Tax Act - Section 132 - Subsection 132(6) - Paragraph 132(6)(b) | indemnity given in connection with REIT spin-off transaction was on-side s. 132(6)(b) | 101 |

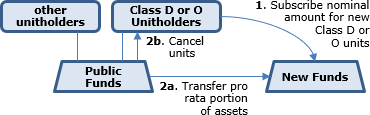

2018 Ruling 2018-0778961R3 - Partial transfer to new funds

Background

In connection with an arm’s length acquisition transaction, apparently of the business of managing (exchange-listed mutual fund trust) Public Funds, as well as pooled-fund trusts (some of which are mutual fund trusts), the proposed transactions allow the “Exchanging Unitholders” (who are holders of Series D Units or Series O Units of some of these Public Funds (Participating Public Funds) and are members of a redacted group to become investors in corresponding New Funds and thereby continue to have their investments managed by the [previous managers], rather than remaining as investors in the Participating Public Funds and having their investments managed by [the new managers].

Proposed transactions

- The New Funds will be formed with the same unit structure and investment objectives as the corresponding Participating Public Funds and with Series D or O Units being issued to the Exchanging Unitholders for nominal consideration that constitutes the only corpus of such trusts.

- Any undistributed income (including net taxable capital gains) of the Participating Public Funds will be made payable to their unitholders.

- Effective after the closing of trading on the Effective Day, each Participating Public Fund will transfer the “Transfer Percentage” (the percentage of the net asset value of the Participating Public Funds represented by the Exchanging Unitholders’ Units) of each of its properties to its corresponding New Fund. The corresponding New Fund will issue Series D and/or Series O Units (as the case may be) to each such Exchanging Unitholder, such that the Net Asset Value of the New Fund Units issued to each Exchanging Unitholder will equal the Net Asset Value of the Exchanging Unitholder’s Units of the corresponding Participating Public Fund immediately before. Also at that time, the Series D and/or Series O Units held by Exchanging Unitholders in the Participating Public Fund will be cancelled for no consideration.

- If and as necessary, each such Participating Public Fund may take advantage of s. 107.4(2.1) of the Act to avoid the need to transfer a fractional share to its corresponding New Fund.

- Certain investors in the [Public Funds] will dispose of their Units in exchange for cash or in kind consideration.

- The Initial Unit (as reduced or subdivided as the case may be, so as to have the same per unit NAV as the newly issued units) for each of the New Funds will be redeemed for an amount equal to its subscription price, i.e. for nominal consideration.

- Where particular New Funds [distinct from those referred to above?] meet the distribution requirements to be mutual fund trusts, the New Fund will effect a s. 132.2 transfer of all its property to the corresponding Exchanging Pooled Fund (also a mutual fund trust) in consideration for units of such transferee, with such units being used to redeem all of the Units of the (New Fund) transferor, and with a joint s. 132.2 election being made. (If the New Fund does not meet such distribution requirement, the s. 132.2 transferor and transferee instead will be the Exchanging Pooled Fund and new Fund, respectively.) In either case, each such transferor will then be terminated.

Rulings

That each transfer of the Transfer Percentage of a property by a Participating Public Fund to its corresponding New Fund will be a “qualifying disposition” within the meaning of subsection 107.4 (1), so that ss. 107.4(3)(a) and (j) will apply. Rulings re subsequent s. 132.2 merger transactions.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(2.1) | use of s. 107.4(2.1) in transfer of portion of MFT to a new MFT | 223 |

2017 Ruling 2016-0625301R3 - Merger of two related segregated fund trusts

Background

The Taxpayer, an insurance company, established two segregated funds (Fund 1 and 2), which used portions of the premiums paid by Fund 1 Policyholders and Fund 2 Policyholders before that time under the terms of their policies to invest in mutual fund trust units. The deemed trusts under s. 138.1(1)(a) respecting Fund 1 and Fund2 are referred to as Trust 1 and Trust 2.

From a commercial law perspective, the Taxpayer is the legal and beneficial owner of each of the properties in Fund 1 and Fund 2, notwithstanding that the Taxpayer allocates such properties, for accounting and administrative purposes, to Fund 1 and Fund 2. However, pursuant to paragraph 138.1(1)(b), for the purposes of Part I of the Act, property that has been allocated to Fund 1 or Fund 2 that remains part of Fund 1 or Fund 2, as the case may be, is deemed to be property of Trust 1 or Trust 2, as applicable, and not property of the Taxpayer.

Proposed transactions

Although all the Fund 1 and Fund 2 properties will continue to be legally and beneficially owned by the Taxpayer, a combination of the two Funds will be effected by the Taxpayer changing the allocation of properties for accounting and administrative purposes, so that all of the properties in Fund 1 will be allocated to Fund 2, with no consideration being paid. Given the different Fund sizes, the number of notional units held by a Fund 1 Policyholder and Fund 2 Policyholder may change. However, each policyholder will have the same economic entitlement as before, and the income which is allocated to each policyholder, which was the same for both Fund 1 Policyholders and Fund 2 Policyholders prior to the combination, will remain the same following the transaction.

Rulings

The reallocation of the properties in Fund 1 to Fund 2 will result in Fund 1 ceasing to exist and Fund 2 as continuing to exist for s. 138.1(1)(a) purposes and be considered to be a transfer by Trust 1 of all of its property to Trust 2 for the purpose of s. 107.4, with s. 107.4(3)(j) applying to deem each of the Fund 1 Policyholders to have disposed of their capital interests in Trust 1 for proceeds equal to the cost amount of such capital interests immediately before the disposition and to have acquired capital interests in Trust 2 at a cost equal to the amount determined by subparagraph 107.4(3)(j)(ii).

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 138.1 - Subsection 138.1(1) - Paragraph 138.1(1)(a) | reallocation by insurer of securities held for one segregated fund to being held for the second segregated fund effected their transfer to the second fund viewed as a deemed trust | 125 |

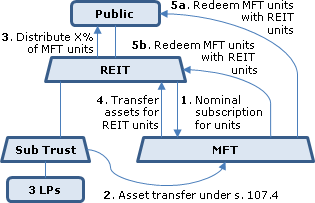

2013 Ruling 2013-0492731R3 - qualifying disposition -mutual fund trust

Current structure

The Fund is an open-end mutual fund trust, whose units trade on an exchange. It owns all the units of Sub Trust (a resident open-end "holding company" unit trust) which, in turn, holds all the Class A units of three subsidiary LPs (the LPs) and all the shares of their general partners (the GPs). Third parties hold the other units (of different classes) of the three LPs including exchangeable units. The LPs principally hold real estate (so that the Fund may be a REIT).

Proposed transactions

- All amounts owed by Sub Trust to the three LPs or the Fund or amounts owed by them to Sub Trust will be repaid in cash or by the issuance of additional units of the debtor.

- MFT will be settled with nominal cash consideration by a Canadian third-party settlor in exchange for one MFT unit. MFT's declaration of trust will have substantially the same terms as for Sub Trust, and its Canadian-resident trustee will not be a director of any of the GPs.

- The Fund will subscribe nominal cash consideration for units of MFT.

- Immediately before the "transfer time" (as defined in the "qualifying exchange" definition) for the assets in 6 below, Sub Trust will transfer its assets (namely Class A units of the three LPs, shares of the related GPs and cash) to MFT for no consideration, and Sub Trust will be wound up. MFT will file an election so that para. (f) of the definition of "disposition" in s. 248(1) will not apply to the transfer. Sub Trust will not make the (non-cost amount) election in s. 107.4(3)(a)(i).

- The Fund will distribute a certain number of its MFT Units to its unitholders on a pro-rata basis as a distribution of capital so that MFT can qualify as a mutual fund trust (and for purposes of satisfying the requirements of Reg. 4801, the MFT unitholders will include groups of unitholders that collectively meet such requirements, as determined under Regs. 4803(3) and (4).) The Fund will remit the required withholding under s. 218.3(2). Prior to its winding-up in 9 below, MFT will file an s. 132(6.1) election to be deemed to have been a "mutual fund trust" from the beginning of its first taxation year.

- MFT will transfer its assets (the same as in 4) to the Fund in consideration for the Fund units having a fair market value equal to the transferred assets.

- Immediately after the transfer time in 6, MFT will redeem all of the issued and outstanding MFT Units held by the Fund and the MFT unitholders (except for one MFT Unit which the Fund will continue to hold until 9), in consideration solely for Fund units. The Fund Units so received by the Fund will be cancelled upon receipt.

- The number of outstanding the Fund units will be consolidated back to the previous number (pursuant to a clause previously added to the Declaration of Trust providing for this to occur automatically).

- Subsequent to the filing of the ss. 132.2 and 132(6.1) elections, MFT will be wound up –with its one outstanding unit cancelled for no consideration.

Rulings

include:

- The transfer in 4 will be a "qualifying disposition" to which s. 107.4(3) will apply.

- Provided that at the transfer time in 6 each of MFT and the Fund is a mutual fund trust, the property so transferred has an aggregate FMV equal to at least 90% of the FMV of all property owned by MFT, and MFT and the Fund jointly elect in accordance with s. 132.2(1), transactions 6 and 7 will constitute a "qualifying exchange."

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 132 - Subsection 132(6) | MFT's trustee not to be a director of a sub | 119 |

| Tax Topics - Income Tax Act - Section 132.2 - Subsection 132.2(1) - Qualifying Exchange | elimination of REIT subtrust through s. 107.4 transfer to new "in house" MFT and s. 132.2 merger of MFT into REIT | 97 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | no disposition on MFT units consolidation back to the previous number, occurring outside a Plan of Arrangement | 107 |

2013 Ruling 2013-0488351R3 - Conversion of a MFC to a MFT

The same (mutual fund corporation) taxpayer as for 2013 Ruling 2011-0395091R3 (immediately below) obtained essentially the same rulings for transactions which now reflected its acquisition of "Target" trust before the implementation of the merger of the taxpayer under s. 132.2 into REIT #1 (the internally-created replacement mutual fund trust) and the elimination of various subtrusts using s. 107.4 (or s. 248(1) – non-disposition) transfers and the s. 132.2 merger rules. To reflect the inclusion of Target in the starting structure, after the non-disposition transfers of four predecessor subtrusts to a new subtrust, that new subtrust, in turn, will effect a s. 107.4(3) transfer of all its property to Target, so that the transferor trust ceases to exist. Accordingly, the s. 107.4(3) transfer to REIT#2 will be by Target rather than Trust A. Furthermore, there will be similar transactions (involving "REIT#4" and "Target Operating Trust") for the elimination of a subtrust of Target.

See summary under s. 132.2 – qualifying exchange.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 132.2 - Subsection 132.2(1) - Qualifying Exchange | conversion of MFC to MFT and subtrust elimination | 178 |

| Tax Topics - Income Tax Act - Section 21 - Subsection 21(1) | election of GP to capitalize loss before elimination of subtrust | 204 |

2013 Ruling 2011-0395091R3 - MFC to MFT Conversion

Background

Taxpayer, which is a listed mutual fund corporation, wishes to convert to a mutual fund trust (so that following the conversions transactions its remaining assets will be nominal) and to eliminate subsidiary (non-personal trust) subtrusts.

Transactions

Taxpayer will settle a subtrust with modest assets, and distribute the units of the subtrust to its public shareholders, who thus will now hold assets of a "good" mutual fund trust ("REIT #1"), albeit with nominal assets. Next, Taxpayer will merge into REIT #1 under s. 132.2, so that REIT #1 is now the successor to substantially all its assets. In order to get rid of a subtrust which now is an asset of REIT #1 (and which was the result of an earlier s. 248(1) – disposition, (f) consolidation of four predecessor subtrusts into one), there will be s. 107.4 transfers of all its assets to a new subtrust ("REIT #2"), followed by a distribution of its units by REIT #1 to the REIT #1 unitholders. REIT #2 then will be merged into REIT #1 under s. 132.2. The same steps will then be repeated for a lower-tier subtrust.

Ruling

that such s. 107.4 transfers will be a qualifying disposition under s. 107.4(1).

See detailed summary under s. 132.2 – qualifying exchange.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 132.2 - Subsection 132.2(1) - Qualifying Exchange | 1059 | |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | deductible interest on internal assumption (no release) | 159 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition - Paragraph (f) | consolidation of 4 subtrusts into 1 using (f) | 178 |

17 October 2012 Ruling 2011-0428321R3 - qualifying disposition -mutual fund trust

Various mutual fund trusts (the "Funds") have several classes of outstanding units.

The sole difference among the various classes of Units is the management fee that is borne by the Fund [sic?] with respect to each class of Units....[I]t has been decided that it is preferable that the Class XXX unitholders of the Funds (the "Exchanging Unitholders"), rather than continuing to be unitholders of that Fund, become unitholders of a newly established unit trust (a "New Fund") in which the Exchanging Unitholders will, immediately after the Proposed Transactions occur, be the only unitholders.

Accordingly, and following a distribution by Funds to the unitholders of all income realized up to the Valuation Date for the reorganization, the Trustee of each Fund will transfer to the corresponding New Fund a percentage of each asset held by the Fund equal to the Transfer Percentage for the Fund (being the proportionate NAV of the Fund attributable to the Exchanging Unitholders for the Fund). However:

If and as necessary, a Fund will take advantage of the provisions of subsection 107.4(2.1) to avoid the need to transfer a fractional share to the New Fund where this would not be feasible. The New Fund will issue to each Exchanging Unitholder in respect of that New Fund such number of New Units of the New Fund as have a fair market value equal to the fair market value of that Exchanging Unitholder's Exchange Units of the Fund...[and] the Exchange Units of each Exchanging Unitholder of the Fund will be surrendered to the Fund by the Exchanging Unitholders.

Rulings that: the asset transfers by a Fund will be a "qualifying disposition;" the proceeds of disposition to a Fund and the asset cost to a New Fund will be determined under ss. 107.4(3)(a) and (b); and that s. 107.4(3)(j) will apply in respect of the cancellation of the Exchange Units and the receipt of New Units by the Exchanging Unitholders.

Paragraph 107.4(1)(a)

Administrative Policy

9 April 2020 External T.I. 2014-0527261E5 F - Beneficial ownership discretionary power of trustees

An individual resident in Canada settles and contributes capital property to a trust governed by the Civil Code of Québec (the "C.C.Q.") under which the settlor is one of the two trustees and under the terms of which no person other than the settlor can, before that individual’s death, receive any part of the income or capital, but with discretion accorded to the trustees as to whether or not to distribute the income and capital to the beneficiary, and with any undistributed income reinvested in the trust. On death, the trust property would go to the settlor's estate by virtue of the terms of the C.C.Q.

Does the according by the trust indenture to the trustees of the discretion to distribute income and capital to the beneficiary prevent s. 107.4(1)(a) from being satisfied? CRA responded:

Having regard to paragraph 248(3)(e) and subsection 248(25), it is reasonable to consider that the transfer of property to a trust governed by the C.C.Q. of which the transferor is the sole beneficiary does not result in a change in beneficial ownership for the purposes of paragraph 107.4(1)(a).

Thus, a discretion accorded to the trustees, under the terms of the trust indenture, as to when they may distribute capital and income to the beneficiary would not, in and of itself, affect the determination of whether or not there is a change in beneficial ownership as long as the individual is, as a result of the transfer of the property to the trust, the sole person beneficially interested in the trust within the meaning of subsection 248(25).

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(1) - Paragraph 107.4(1)(i) | discretion of trustees to retain capital or income rather than distribute to the sole current beneficiary precluded s. 73(1.01)(c)(ii) application and satisfied s. 107/4(1)(i) | 291 |

| Tax Topics - General Concepts - Ownership | discretion of trustee to accumulate rather than distribute income to sole beneficiary did not detract from beneficial ownership | 269 |

| Tax Topics - Income Tax Act - Section 73 - Subsection 73(1.01) - Paragraph 73(1.01)(c) - Subparagraph 73(1.01)(c)(ii) | "right to receive" all the income not satisfied where trustees' discretion to accumulate income | 233 |

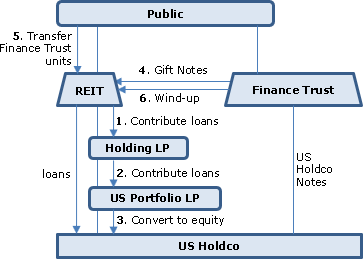

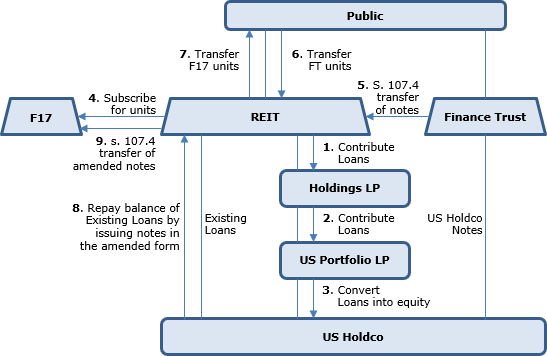

2018 Ruling 2018-0752811R3 - Transfer of Debt as Qualifying Disposition

Current Structure

The units of the REIT (a real estate investment trust) are stapled to those of Finance Trust (a portfolio investment entity and a mutual fund trust), so that they trade on a stock exchange together. Finance Trust (along with the REIT) holds notes (the "US Holdco Notes") of the indirect U.S. commercial real estate subsidiary of the REIT (“U.S. Holdco”). Finance Trust qualifies as a fixed investment trust for Code purposes, so that its unitholders are treated as if they held such notes directly. The REIT holds US Holdco through a 2-tier subsidiary LP structure (i.e., holding Holdings LP which in turn holds US Portfolio LP.)

Purposes

As a result of US tax reform, Finance Trust no longer serves a purpose as adverse US tax consequences are no longer suffered by US Holdco on interest paid to the REIT. The proposed transactions allow for the US Holdco Notes to be transferred out of Finance Trust prior to its termination, and (in transactions not described below) also permit the US Holdco Notes to be refinanced to reflect current commercial arm’s length interest rates.

Proposed Transactions

A portion of the existing loans will be contributed by the REIT to Holdings LP, and by Holdings LP to US portfolio LP. An equity conversion option will be added to their terms and US portfolio LP will then convert them into equity on exercise of that option.

Finance Trust will transfer all of the US Holdco Notes held by it (being most of its property) to the REIT for no consideration (the “Disposition”). At the time of transfer, the beneficiaries of the REIT will be identical to, and will hold their units in the same proportions as, the beneficiaries of Finance Trust. The REIT will purchase all of the outstanding Finance Trust Units from the Finance Trust Unitholders for their nominal value, and Finance Trust will redeem all of the Finance Trust Units and will be terminated.

Ruling

The Disposition will constitute a “qualifying disposition” within the meaning of s. 107.4(1), such that the rules in s. 107.4(3) will apply to the REIT, Finance Trust and their respective unitholders in respect of the Disposition.

2017 Ruling 2017-0720591R3 - Re-org of a stapled commercial trust structure

Current Structure

The units of the REIT (a real estate investment trust) are stapled to those of Finance Trust (a portfolio investment entity and a mutual fund trust), so that they trade on a stock exchange together. Finance Trust holds notes of the indirect U.S. commercial real estate subsidiary of the REIT (“U.S. Holdco”). Finance Trust qualifies as a fixed investment trust for Code purposes, so that its unitholders are treated as if they held such notes directly. This avoids the U.S. earnings stripping limitations on the level of permitted interest deductions by U.S. Holdco. However, subsequently to this structure being implemented, U.S. acquisitions by U.S. Holdco were funded with loans from REIT, which are subject to the earnings stripping rules. Each unit of the REIT and of Finance Trust (and of F17 Trust described below) represents an equal undivided beneficial interest in the property of the trust.

Proposed Transactions

In order that much of this additional debt can access the benefits of the stapled structure, the REIT and Finance Trust are proposing that Finance Trust first make a s. 107.4 transfer of its notes of U.S. Holdco to the REIT. Following the replacement of those notes and some of the newer debt with amended notes, and the transfer to the unitholders of units of a new fixed investment trust with nominal assets (the “F17 Trust”) in consideration for the nominal cash received by them for the transfer of their units of Finance Trust to the REIT (whose ACB will have been reduced under s. 107.4(3)(l)), the amended notes will be transferred by the REIT under s. 107.4 to the F17 Trust. Finance Trust then will redeem all its units. Thus, there will be a replacement stapled structure similar to what was there before, except that the new Finance Trust (F17 Trust) will hold more U.S. Holdco debt.

Ruling

The disposition of the Finance Trust loans to the REIT and of the amended loans to F17 Trust will constitute “qualifying dispositions” under s. 107.4(1), such that the rules in s. 107.4(3) will apply to the REIT, Finance Trust, F17 Trust, and their respective unitholders in respect such dispositions.

See also H&R REIT summary.

14 March 2012 External T.I. 2011-0423291E5 F - Fiducie pour soi-même sans limite d'âge

Two spouses (Mr. X and Ms. X) and their two adult children wish to contribute their jointly owned shares of Holdco to a newly-settled protective trust.

Can the transfer of the Holdco shares by the the four family members, to the extent that it cannot occur tax-free pursuant to subsection 73(1), be made pursuant to subsection 107.4(3)?

A "qualifying disposition" is defined in subsection 107.4(1) and in order for the transfer of property to be a qualifying disposition, the following conditions must be met:

i) there is a change in the legal title but not in the beneficial ownership of the property;

ii) the disposition is not made by a person resident in Canada to a non-resident trust;

iii) immediately after the disposition no person other than the contributor has an absolute or contingent right of any kind in the trust;

iv) the proceeds are not determined under any other provision of the Act (leaving aside sections 69 and 73);

v) subsection 73 (1) does not apply even if some of the conditions in subsection 73(1) are not satisfied.[A] qualifying disposition of the trust would not be possible because conditions (i) and (iii) would not be met.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 73 - Subsection 73(1.01) - Paragraph 73(1.01)(c) - Subparagraph 73(1.01)(c)(ii) | joint protective trust would not satisfy s. 73(1.01)(c)(ii) | 180 |

| Tax Topics - Income Tax Act - Section 73 - Subsection 73(1.01) - Paragraph 73(1.01)(c) - Subparagraph 73(1.01)(c)(iii) - Clause 73(1.01)(c)(iii)(A) | two spouses separate from their children can create a joint spousal or common-law partner trust | 156 |

| Tax Topics - Income Tax Act - Section 108 - Subsection 108(1) - Testamentary Trust | tainting effect of joint spousal or common-law partner trust on subsequent testamentary trust | 211 |

2004 Ruling 2003-0053981R3 - XXXXXXXXXX

Proposed transactions

- The Fund, which is an exchange-traded mutual fund trust, will for nominal consideration subscribe for one Trust Unit of a unit trust (the “Trust”) that was settled by a third party, and redeem the initial Trust Unit held by that third party for its cash subscription price.

- The Fund will transfer all of the Partnership Units of a partnership to the Trust for one or more Trust Units. This transfer will occur in one day. The Fund will not make the election in s. 107.4(3)(a)(i) and the Trust will not make the election in s. 107.4(3)(c)(ii)(B). Following this transfer, the Fund will continue to directly own 100% of the Trust Units and will indirectly own 100% of the Partnership Units. The Partnership Units acquired by the Trust will not be used to fund a distribution by the Trust. The value of the beneficial ownership of each holder of a Fund Unit under the Fund in the Partnership Units at the commencement of the transfer this transfer will be the same as the value of such holder's beneficial ownership under the Fund and the Trust in the Partnership Units at the completion of the transfer.

Ruling

The transfer of the Partnership Units from the Fund to the Trust will be a "qualifying disposition" pursuant to s. 107.4(1).

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | elimination of MFT corporate sub through creation of MFC and 132.2 merger | 160 |

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(1) - Paragraph 107.4(1)(h) | immediate refinancing of drop-down subsidiary trust of MFT did not offend policy of para. (h) | 234 |

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(3) - Paragraph 107.4(3)(m) | units must be received on drop-down of LP to new subtrust (thereby ousting s. 107.4(2)(a)), in order to receive outside basis under s. 107.4(3)(m) | 241 |

22 April 2002 External T.I. 2002-0117135 F - Appl. de 107.4(1)a) à une fiducie du CcQ

Would s. 107.4(1)(a) be satisfied where a transferor transfers ownership of property to a Quebec trust of which he is the sole beneficiary? CCRA responded:

[T]he transferor of the property will therefore be considered, under paragraph 248(3)(f), to have beneficial ownership of the property immediately before its transfer to the trust. Since he is a beneficiary of the trust, the transferor will also be considered to have beneficial ownership of the property after its transfer, pursuant to paragraph 248(3)(f) and subsection 248(25). Consequently, to the extent that the transferor is the sole beneficiary of the trust within the meaning of subsection 248(25) when the property is transferred to the trust, the transfer will not have the effect of changing the beneficial ownership of the transferred property, thereby satisfying the condition set out in paragraph 107.4(1)(a).

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107 - Subsection 107(4.1) | s. 107(2.1) applicable to distribution by personal trust of property to beneficiary other than the settlor | 46 |

Articles

Geraint Thomas, Alastair Hudson, "Chapter 7: The Nature of a Beneficiary’s Interest", The Law of Trusts,” Oxford University Press, 2004

Under some trusts the beneficiary has rights in rem against the trust property (p. 173)

7.01 The debate on the nature of a beneficiary's interest under a trust, and specifically whether a beneficiary's rights are rights in personam against the trustee or rights in rem against the trust property, has a long history and remains controversial. It is certainly the case that a beneficiary has a right in personam to insist upon and compel the due and proper administration of the trust by the trustee and to require the trustee to account for his stewardship of trust assets. However, it also seems clear that, at least in relation to certain kinds of trust, such as a bare trust, a beneficiary has rights in rem, in that he can compel the trustee to transfer the legal title to him. Moreover, as a general rule, a beneficial interest under a ‘fixed’ trust, ie a defined, limited interest (be it vested or contingent, in possession or in remainder), clearly possesses many of the characteristics of ‘property’. [fn. 2: Tinsley v. Milligan, [1994] AC 340, 371] The beneficiary can alienate such an interest by assignment of otherwise; and he can declare (sub-)trusts of that interest. In addition, a beneficiary—including an object of a discretionary trust who has no right to compel the trustee to pay him any trust income or capital, who is dependent on the exercise of the trustees' discretion in his favour, and who cannot, therefore, be said to have an equitable proprietary interest as such—may still trace the trust assets into the hands -of third parties (unless that third party is ‘equity's darling’ or otherwise protected).

Title of equitable owner (beneficiary) not quite as absolute as that of legal owner (p. 174)

7.02 ... [T]he position in equity was that a person who took the trust property without giving value in exchange (a donee, heir, or executor) took it with all its attaching burdens, equitable and legal; and that even someone who had given value would be bound if, before the conveyance, he knew of (ie had notice of) the existence of the trust. The ‘polar star of equity’ thus became: legal rights are good against all the world; equitable rights are good against all persons except , a bona fide purchaser of the legal estate for value without notice (ie ‘equity's darling’) and those claiming under such a purchaser. The title of the equitable owner became almost, but not quite, as absolute and indefeasible as the title of a legal owner. The beneficiary's rights clearly became much more than rights in personam enforceable only against the trustee: they are rights enforceable against virtually all third parties, so at worst they are hybrid rights.

Equitable interest in real estate trust had the quality of real estate (p. 177)

7.08 Equitable interests were modelled ‘into the shape and quality of real estate’ [fn: 27: Burgess v Wheate (1759) 1 Eden 177, 249.] A beneficiary under a fixed trust has an equitable, proprietary interest and, as such, it possesses the usual characteristics of property. Thus, the beneficiary may use or enjoy it or its fruits, charge it or assign it to another. The nature and extent of the beneficiary s rights will depend on the nature and extent of the interest itself, for example whether it is limited or absolute, determinable or conditional, and so forth. Subject to this, however, a restraint on the alienation of an equitable interest is generally as ineffective as one imposed on a legal interest.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Ownership | 1015 |

Paragraph 107.4(1)(h)

Administrative Policy

2004 Ruling 2003-0053981R3 - XXXXXXXXXX

A publicly-trade mutual fund trust (the "Fund") eliminated a corporate subsidiary ("Holdings") by incorporating a subsidiary ("MFC") with a modest value, distributing interests in MFC to its unitholders as a capital distribution in order that MFC would qualify as a mutual fund corporation, transferring Holdings to MFC on a s. 85(1) rollover basis in consideration for MFC shares, having MFC amalgamate with Holdings to form MFC Amalco, and then having MFC Amalco merge into the Fund in accordance with s. 132.2 so that the Fund acquired the assets of MFC Amalco, principally, units in a subsidiary LP.

Following these transactions, the Fund will transfer all of such LP units to a newly settled unit trust (the "Trust") for one or more Trust Units, so that following this transfer it will continue to own directly 100% of the Trust Units and indirectly own 100% of the LP units. The Trust will then use proceeds of a daylight loan to distribute cash proceeds to the Fund as a return of capital and the Fund will lend those proceeds to the Trust.

Ruling that the transfer of the LP units from the Fund to the Trust will be a “qualifying disposition” and that s. 245(2) will not apply. The CRA summary indicates that the refinancing of the Trust is not offensive as regards the qualifying disposition rules.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(1) - Paragraph 107.4(1)(a) | qualifying drop-down of partnership units to subsidiary unit trust where s. 107.4(2)(a) was ousted due to units issuance | 246 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | elimination of MFT corporate sub through creation of MFC and 132.2 merger | 160 |

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(3) - Paragraph 107.4(3)(m) | units must be received on drop-down of LP to new subtrust (thereby ousting s. 107.4(2)(a)), in order to receive outside basis under s. 107.4(3)(m) | 241 |

Paragraph 107.4(1)(i)

Administrative Policy

9 April 2020 External T.I. 2014-0527261E5 F - Beneficial ownership discretionary power of trustees

An individual resident in Canada settles and contributes capital property to a Quebec trust under which the settlor is one of the two trustees and under the terms of which no person other than the settlor can, before that individual’s death, receive any part of the income or capital, but with discretion accorded to the trustees as to whether or not to distribute the income and capital to the beneficiary, and with any undistributed income reinvested in the trust. On death, the trust property would go to the settlor's estate. Does the discretion of the trustees to distribute income and capital to the beneficiary result in the condition in s. 107.4(1)(i) being satisfied?

After noting that the relevant requirement was that in s. 73(1.01)(c)(ii) that, after transferring the capital property to the trust, the “individual is entitled to receive all of the income of the trust that arises before the individual’s death and no person except the individual may, before the individual’s death, receive or otherwise obtain the use of any of the income or capital of the trust,” CRA stated:

"[T]he right to receive" all of the trust income in subparagraph 73(1.01)(c)(ii) means that the right to require payment of trust income must belong solely to the beneficiary and that, under the terms of the relevant trust indenture, the trustees may not restrict the payment of all or part of the trust income.

…[W]here the Trust Indenture accords the Trustees the discretion as to the distribution of the income of the trust, the condition set out in paragraph 73(1.01)(c)(ii) would not be satisfied. Consequently, the requirement in paragraph 107.4(1)(i) would be satisfied … .

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(1) - Paragraph 107.4(1)(a) | discretion of trustees to retain capital or income rather than distribute to the sole current beneficiary does not preclude the latter being the beneficial owner | 277 |

| Tax Topics - General Concepts - Ownership | discretion of trustee to accumulate rather than distribute income to sole beneficiary did not detract from beneficial ownership | 269 |

| Tax Topics - Income Tax Act - Section 73 - Subsection 73(1.01) - Paragraph 73(1.01)(c) - Subparagraph 73(1.01)(c)(ii) | "right to receive" all the income not satisfied where trustees' discretion to accumulate income | 233 |

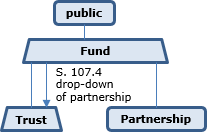

Subsection 107.4(2) - Application of paragraph (1)(a)

Administrative Policy

2021 Ruling 2021-0894161R3 - Qualifying Disposition - REIT spinout

CRA ruled on a transactions for the spin-off by an existing REIT of a portion of its operations (the “Segment”) to a newly formed REIT.

In addition to numerous transactions to properly package the Segment, the Plan-of-Arrangement transactions included the REIT settling the New REIT, subscribing a modest amount (in the form of a REIT note issued by it to New REIT) in consideration for New REIT units equal in number to the number of outstanding REIT units, distributing a modest amount of cash to a depositary for its unitholders, and selling its units of the New REIT to the unitholders for such cash.

The REIT was then to transfer the Segment to New REIT in a gratuitous transfer that apparently was intended to qualify as a “sideways” transfer in accordance with s. 107.4(2), with CRA ruling that the transfer would be a “qualifying disposition” under the definition in s. 107.4(1), so that the rollover rules in s. 107.4(3) could apply.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(1) | use of s. 107.4(1) to effect the spin-off by a REIT of a portion of its operations to a new REIT | 1191 |

| Tax Topics - Income Tax Act - Section 132 - Subsection 132(6) - Paragraph 132(6)(b) | indemnity given in connection with REIT spin-off transaction was on-side s. 132(6)(b) | 101 |

Paragraph 107.4(2)(a)

Administrative Policy

2017 Ruling 2016-0660321R3 - Reorg of REIT to simplify multi-tier structure

Overview

A Canadian REIT (the “Fund”) holds the units and notes of a subsidiary unit trust (“Sub-Trust”), whose principal asset is most of the partnership interests, other than exchangeable LP units, in a subsidiary LP (“Partnership”).

Steps relating to elimination of Sub-Trust

The Fund eliminates Sub-Trust by setting up a unit trust (“MFT”), transferring the Sub-Trust assets to MFT under s. 107.4, distributing just enough units of MFT to its unitholders for MFT to qualify as a mutual fund trust, and then instigating a s. 132.2 merger of MFT into the Fund. In particular:

- After the settling of MFT, which has redeemable retractable units, by a Canadian-resident third party, the Fund subscribes for MFT units for nominal cash consideration and the unit of the settlor is redeemed.

- Sub-Trust will transfer all its assets including the Class A LP Units and the GP I shares of Partnership, to MFT for no consideration, with no s. 107.4(3)(a)(i) election being made and with MFT electing under (f)(v) of “disposition” in s. 248(1) that para. (f) thereof not apply.

- Fund will distribute a certain number of its MFT Units to the Fund Unitholders in accordance with applicable securities’ laws (with s. 218.3(2) withholding being made) such that MFT will qualify as a mutual fund trust (and with a s. 132(6.1) election made before the winding-up of MFT in 7 below).

- The Declaration of Trust of the Fund will be amended to provide for inter alia the consolidations in 6 below.

- Pursuant to a transfer agreement between the Fund, MFT and an agent for the MFT Unitholders, MFT will transfer its assets to the Fund at the “MFT Transfer Time” in consideration for Fund Units being issued to the MFT Unitholders in payment of the redemption proceeds for their Units; and immediately after the MFT Transfer Time, MFT will redeem all of the MFT Units held by the Fund and the MFT Unitholders except for one MFT Unit which the Fund will continue to hold until the winding-up of MFT in 7 below. In due course, a joint s. 132.2 joint election will be filed.

- Immediately thereafter the outstanding Fund Units are consolidated so as to result in the same number as before.

- Ultimately, MFT will be wound up.

Ruling

The asset transfer in 2 will be a “qualifying disposition” within the meaning of s. 107.4(1), such that the rules in s. 107.4(3) will apply to Sub-Trust and MFT in respect of such transfer.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 132.2 - Subsection 132.2(1) - Qualifying Exchange | use of the s.132.2 merger and a renunciation of most of the units otherwise issuable on the merger in order to eliminate a REIT corporate subsidiary held through an LP and a sub-trust | 1006 |

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(3) | drop down of LP 1 into LP 2 followed by immediate s. 98(3) wind-up of LP 1 into LP 2 and GP of LP1, followed by immediate taxable sale by GP to LP 2 | 146 |

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | no taxable benefit where wholly-owned partnership renounces the right to receive units of its “parent” REIT | 325 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | no disposition of partnership interests or property on conversion of general to limited partnership or adding right of renunciation of a MFT unitholder | 165 |

| Tax Topics - Income Tax Act - Section 132.2 - Subsection 132.2(3) - Paragraph 132.2(3)(g) - Subaragraph 132.2(3)(g)(vi) - Clause 132.2(3)(g)(vi)(C) - Subclause 132.2(3)(g)(vi)(C)(I) | renunciation by subsidiary partnership of transferee MFT of units that otherwise would be issuable on the redemption of its incestuous holding in transferor MFC | 245 |

2003 Ruling 2003-000498C - Qualifying disposition from trust to Sub

Current structure

The Fund, which is an exchange-listed mutual fund trust, holds shares and debt (the Corporation Shares and the Corporation Notes) of an operating subsidiary, and holds a general partnership interest through a sub trust (the trust).

Proposed transactions

The Fund will transfer the Corporation Shares and the Corporation Notes to the Trust for no consideration. This transfer will take place in one day. It will not make a s. 107.4(3)(a)(i) election and the Trust will not make a s. 107.4(3)(c)(ii)(B) election. There will be no transfer of property to the Trust as consideration for the acquisition of a capital interest in the Trust where the particular property can reasonably be considered to have been received by the Trust in order to fund a distribution. The value of each beneficiary's beneficial ownership under the Fund in the Corporation Shares and Corporation Notes at the commencement of this transfer will be the same as the value the beneficiary's beneficial ownership under the Fund and the Trust in the Corporation Shares and Corporation Notes at the completion of the transfer.

Ruling

S. 107.4(2)(a) will apply so that for purposes of s. 107.4(1)(a), and the transfer will not result in any change in beneficial ownership of the transferred Corporation Shares and the Corporation Notes.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(3) - Paragraph 107.4(3)(m) | no increase to ACB of subtrust units where dropdown to the subtrust for no consideration | 55 |

Subsection 107.4(2.1)

Administrative Policy

2018 Ruling 2018-0778961R3 - Partial transfer to new funds

In connection with an arm’s length acquisition transaction, apparently of the business of managing exchange-listed mutual fund trusts, holders of Series D or O Units of some of such funds (the Participating Public Funds) wish to become investors in corresponding “New Funds” and thereby continue to have their investments managed by the previous managers, rather than remaining as investors in the Participating Public Funds and having their investments managed by the new managers.

CRA provided s. 107.4 rollover rulings respecting a transfer of a proportionate part (the “Transfer Percentage”) of each security holding of each Participating Public Fund (based on the percentage of the NAV of the Participating Public Fund attributable to the units of the Series D or O Unitholders) to the corresponding New Fund (held by the Series D or O Unitholders) for no consideration, with the Series D or O Units in the Participating Public Fund being cancelled for no consideration.

[F]or each class of identical securities held by a Participating … Public Fund, [it] will transfer the Transfer Percentage of such securities to its corresponding New Fund. If and as necessary, each such Participating … Public Fund may take advantage of the provisions of subsection 107.4(2.1) of the Act to avoid the need to transfer a fractional share to its corresponding New Fund.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(1) | use of s. 107.4 transfers to split up ETFs | 599 |

Subsection 107.4(3) - Tax consequences of qualifying dispositions

Administrative Policy

20 March 2013 External T.I. 2013-0474861E5 - Subparagraph 107.4(3)(a)(i) election

There is currently no prescribed form available for the subparagraph 107.4(3)(a)(i) election. In place of a prescribed form, the transferor trust should attach a letter, setting out the details of the election to the T3 Trust Income Tax and Information Return for the taxation year that includes the time of the qualifying disposition. The election should be filed on or before the filing due date of the transferor's T3 Trust Income Tax and Information Return.

7 December 2000 External T.I. 2000-0032685 - QUALIFIED DISPOSITION SEGREGATED FUNDS

If a policyholder does not realize any disposition of an interest in a segregated fund contract (viewed as analogous to a capital interest in a trust) by virtue of a variation of the contract that occurs in connection with a qualifying disposition, s. 107.4(3)(k) would apply to add policyholder's cost base in the transferor to its basis, if any, in the transferee trust. Similarly, if a policyholder, in connection with a variation of a contract that occurs in connection with a qualifying disposition, should dispose of an interest in the segregated fund contract, s. 107(3)(j) would provide a rollover to the policyholder.

Paragraph 107.4(3)(m)

Administrative Policy

2004 Ruling 2003-0053981R3 - XXXXXXXXXX

The Fund, which is an exchange-traded mutual fund trust, will for nominal consideration subscribe for one Trust Unit of a unit trust (the “Trust”) that was settled by a third party, and redeem the initial Trust Unit held by that third party for its cash subscription price.

The Fund will transfer all of the Partnership Units of a partnership to the Trust for one or more Trust Units. This transfer will occur in one day. The Fund will not make the election in s. 107.4(3)(a)(i) and the Trust will not make the election in s. 107.4(3)(c)(ii)(B). Following this transfer, the Fund will continue to directly own 100% of the Trust Units and will indirectly own 100% of the Partnership Units.

CRA ruled that the transfer of the Partnership Units from the Fund to the Trust will be a "qualifying disposition" pursuant to s. 107.4(1). In its summary, CRA stated:

The Fund will acquire one or more units of the Trust in exchange for the limited partnership units and 107.4(3)(m) will deem the cost of the additional units to be the Fund's tax cost of the limited partnership units so transferred. If the Fund had not acquired any additional units … the contribution to the Trust would not increase the Fund's ACB of its capital interest in the Trust, notwithstanding that it would increase the FMV of its capital interest in the Trust.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(1) - Paragraph 107.4(1)(a) | qualifying drop-down of partnership units to subsidiary unit trust where s. 107.4(2)(a) was ousted due to units issuance | 246 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | elimination of MFT corporate sub through creation of MFC and 132.2 merger | 160 |

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(1) - Paragraph 107.4(1)(h) | immediate refinancing of drop-down subsidiary trust of MFT did not offend policy of para. (h) | 234 |

2003 Ruling 2003-000498C - Qualifying disposition from trust to Sub

On a transfer by a mutual fund trust (the "Fund") of shares and notes of a subsidiary to a subsidiary trust (the "Trust") of the Fund for no consideration, no amount would be added pursuant to s. 107.4(3) by virtue of such disposition to the cost of the Trust units owned by the Fund.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(2) - Paragraph 107.4(2)(a) | s. 107.4(2)(a) applies where drop-down by MFT of corporate sub to sub trust for no consideration | 245 |

Subsection 107.4(4)

Administrative Policy

17 March 2003 External T.I. 2002-0130685 F - Limite inférieure - JVM Participation

In response to 10 conceptual questions regarding s. 107.4(4), CCRA noted inter alia:

- “the primary purpose of subsection 107.4(4) was to provide special rules that arise where all or part of an interest in a trust arising from a rollover described in new subsection 107.4(3) is subsequently disposed of” so that “the proceeds of disposition of the interest are deemed not to be less than the fair market value of the net assets of the trust related to the interest.”

- the rule in s. 107.3(4) applies throughout the Act;

- it can extend to a disposition of an interest by a resident beneficiary to a non-resident trust or by a non-resident beneficiary to a resident trust.

- it extends to various types of trusts such as both business and personal trusts, and trusts to which s. 75(2) applies by virtue of s. 107(4.1);

- s. 107.4(4) is not relevant to the application of ss. 107(2) and 107(2.1) since the fair market value of the capital interest is not required for the purposes of those provisions.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 108 - Subsection 108(1) - Trust - Paragraph (g) | meaning of vested indefeasibly | 56 |