See Also

Lohas Farm Inc. v. The Queen, 2019 TCC 197

A grey marketer (Lohas) of newly-released iPhones purchased them in Vancouver-area Apple stores for export to Hong Kong and Taiwan, where those...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Agency | buyers made purchases of iPhones as agents for a grey market reseller | 450 |

| Tax Topics - General Concepts - Onus | no burden of displacing an assumption as to a factual matter which the taxpayer could not be reasonably expected to know | 286 |

| Tax Topics - Excise Tax Act - Regulations - Input Tax Credit Information (GST/HST) Regulations - Section 3 - Paragraph 3(c) - Subparagraph 3(c)(ii) | missing names in receipts issued by vendor were cured by memo maintained by the purchaser | 205 |

Subsection 169(1) - General Rule for Credits

Cases

Amex Bank of Canada v. Canada, 2026 FCA 31

CRA denied the input tax credit (“ITC”) claims of Amex for its 2002 to 2012 taxation years for GST/HST paid on expenses arising in connection...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 181 - Subsection 181(5) | no ITC for redemption of travel miles under card program since the redemption payments occurred in the course of a credit-generating activity | 220 |

| Tax Topics - Excise Tax Act - Section 141.01 - Subsection 141.01(4) | free supply of card loyalty rewards promoted credit supply by card issuer rather than taxable supplies | 193 |

Northbridge Commercial Insurance Corporation v. Canada (the King), 2025 FCA 83

The Federal Court of Appeal had previously allowed the appeal of Northbridge from a Tax Court finding that it was making only exempt supplies in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Schedules - Schedule VI - Part IX - Section 2 | zero-rating of insurance supplies under s. VI-IX-2 could be determined on a global basis for ITC purposes | 218 |

| Tax Topics - Excise Tax Act - Section 141.02 - Subsection 141.02(1) - Direct Input | whether head office rent was a direct input or non-attributable input was under dispute/ classification of inputs in hands of Tax Court | 378 |

President's Choice Bank v. Canada (the King), 2024 FCA 135

Goyette JA contrasted s. 169(1) “which provides a formula that only awards ITCs to the extent that a good or service was used in the course of a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 181 - Subsection 181(5) | loyalty point redemption payments made in the course of a financial business could generate ITCs if also in the course of a commercial activity | 562 |

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Commercial Activity | commercial activity of corporation can be at a loss | 144 |

Canada v. General Motors of Canada Limited, [2009] GSTC 64, 2009 FCA 114

The Appellant (a car manufacturer) was the administrator of various defined benefit pension plans for its unionized employees. It was the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 169 - Subsection 169(1) | 99 | |

| Tax Topics - Excise Tax Act - Section 267.1 - Subsection 267.1(2) | administrator of pension trust was not a trustee, and not subject to s. 267.1 | 51 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(1) | administrator of pension trust was not a trustee | 41 |

Haggart v. Canada, 2003 FCA 446

GST on legal services supplied to the applicant to enable him and his company to obtain damages from a bank for wrongfully calling in a loan to...

London Life Insurance Co. v. Canada, [2000] GSTC 111 (FCA)

Under the terms of its leases, the Appellant, whose principal buisness was providing exempt financial services, undertook leasehold improvements...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Improvement | 108 | |

| Tax Topics - Excise Tax Act - Section 141.01 - Subsection 141.01(2) | leasehold construction services were acquired for supply of leasehold improvements to landlord | 259 |

| Tax Topics - Statutory Interpretation - Interpretation Bulletins, etc. | 52 |

Canada v. 398722 Alberta Ltd., [2000] GSTC 32 (FCA)

In order to receive approval under the Town of Banff bylaws for the development and operation of a 63-unit hotel in Banff, the respondent was...

Midland Hutterian Brethren v. Canada, [2000] GSTC 109 (FCA)

In finding that heavy cloth purchased by a Hutterian colony (which was engaged in a farming business) to be made into work clothes for its members...

See Also

Ontario Tire Stewardship v. The King, 2026 TCC 77

Before going on to find that the Minister, in assessing the appellant, should grant it unclaimed ITCs pursuant to s. 296(2) for previous months, ...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 296 - Subsection 296(2) | s. 296(2) required a CRA assessment to take into account unclaimed ITCs for prior stale-dated months | 352 |

| Tax Topics - Excise Tax Act - Section 296 - Subsection 296(4) - Paragraph 296(4)(b) | TCC did not have jurisdiction to consider the Crown’s argument on s. 296(4) | 90 |

Fadali v. The King, 2026 TCC 86

Derksen J. found that the taxpayer was not entitled to claim ITCs respecting his construction expenses of a new home that he had sold in December...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 296 - Subsection 296(2.1) | the s. 296(2.1) requirement on CRA to apply available rebates when assessing HST reduced a late-filing penalty | 246 |

| Tax Topics - Excise Tax Act - Section 280.1 | penalty was reduced by unclaimed but available rebate | 163 |

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Builder - Paragraph (f) | taxpayer constructed and sold a new home as an adventure in the nature of trade | 112 |

Alberta Peloton Association v. The King, 2026 TCC 32

Peloton was a non-profit association that staged the Tour of Alberta Road Race every year. It was denied ITCs for inputs acquired to stage the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 141.01 - Subsection 141.01(2) | purposes of acquiring inputs to a free-attendance race was the generation of the inextricably-linked sponsorship revenues | 321 |

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Supply | doubtful that a supply of a race was made to non-paying spectators | 180 |

267 O'Connor Limited v. The King, 2024 TCC 161 (Informal Procedure)

Upon the appellant entering into an agreement in August 2013 to sell a property to a third party (“Starwood”), Starwood took over the carriage...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 169 - Subsection 169(4) | failure of recipient to demonstrate that that it had the supplier’s registration number at the time of its return filing, or to have documentation of an allocation to the alleged taxable supply | 196 |

| Tax Topics - Excise Tax Act - Section 182 - Subsection 182(1) | s. 182(1) inapplicable where damages paid by supplier rather than recipient | 178 |

ONR Limited Partnership v. The King, 2024 TCC 156

The appellant (the “LP”) was a wholly-owned limited partnership of a REIT. The REIT and the LP entered into two successive written forms of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Agency | REIT could not incur expenses for acts (issuing it units) which its alleged principal (its sub LP) lacked the capacity to perform, but it incurred expenses for the LP business as partner-agent | 467 |

| Tax Topics - General Concepts - Evidence | agreement authenticated pursuant to “comparison of hands” method | 137 |

| Tax Topics - Excise Tax Act - Section 272.1 - Subsection 272.1(1) | s. 272,1(1) inapplicable to expenses incurred by REIT to issue REIT units to fund its partnership investment | 142 |

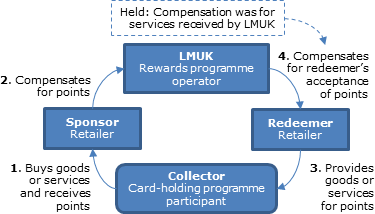

Royal Bank of Canada v. The King, 2024 TCC 125

The appellant (RBC) submitted that it offered loyalty reward points to its cardholders to entice them to use their cards and increase the volume...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 165 - Subsection 165(1.11) | issue should be stated "reasonably" | 131 |

| Tax Topics - Excise Tax Act - Section 141.02 - Subsection 141.02(21) | pre-approval of method for allocating inputs between foreign and domestic supplies did not stop CRA from assessing to deny zero-rating of the foreign supplies | 202 |

| Tax Topics - Excise Tax Act - Section 141.02 - Subsection 141.02(31) - Paragraph 141.02(31)(f) | s. 141.02(31)(f) is merely confirmatory of normal taxpayer onus | 98 |

| Tax Topics - Excise Tax Act - Schedules - Schedule VI - Part IX - Section 1 - Paragraph 1(a) | foreign interchange fees generated by Canadian credit card issuer related to the granting of credit rather than the making of a loan by it, and were not excluded under s. 1(a)(ii) | 445 |

| Tax Topics - Excise Tax Act - Section 141.02 - Subsection 141.02(1) - Direct Input | expenses of redeeming credit card loyalty points were inextricably linked to the issuer’s extension of credit, and only remotely linked to its earning zero-rated interchange fees | 368 |

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Recipient | merchant acquirer was the recipient of credit card interchange services even though it was a conduit to the merchant | 156 |

| Tax Topics - Statutory Interpretation - Exclusionary provisions | exclusionary provisions should be narrowly construed | 267 |

| Tax Topics - Excise Tax Act - Section 301 - Subsection 301(1.2) - Paragraph 301(1.2)(a) | taxpayer not precluded from raising an argument that the Minister was bound by an ITC method that it had described in detail in its pleadings | 175 |

Fiera Foods Company v. The King, 2023 TCC 140

Two bakery plants of the appellant were staffed in significant part by temporary workers (“TWs”), who were sourced from third parties (the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Regulations - Input Tax Credit Information (GST/HST) Regulations - Section 2 - Supporting Documentation | registrant not required to demonstrate that invoice received in name of supplier was in fact “issued” by it | 550 |

| Tax Topics - Excise Tax Act - Section 169 - Subsection 169(4) - Paragraph 169(4)(a) | no particular form of supplier documentation is required for ITC purposes | 328 |

Amex Bank of Canada v. The King, 2023 TCC 93, aff'd 2026 FCA 31

The Minister denied the input tax credit (“ITC”) claims of Amex Bank of Canada’s (“Amex”) for its 2002 to 2012 taxation years for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 141.01 - Subsection 141.01(4) | Amex did not make “free” supplies of rewards to credit card holders but instead were made for consideration and for the purpose of facilitating its exempt credit card business | 277 |

Praesto Consulting UK Ltd v HM Revenue and Customs, [2019] EWCA Civ 353

Mr Ranson, a former employee of an information technology consultancy (“CSP”), resigned to set up a competing company ("Praesto"), where he...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 141.01 - Subsection 141.01(2) | legal fees addressed to executive were paid by company to protect its business | 236 |

International Hi-tech Industries Inc. v. The Queen, 2018 TCC 240

The business of the appellant (“IHI”) included the construction of buildings using prefabricated panels. One of its key shareholders had...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 152 - Subsection 152(1) - Paragraph 152(1)(b) | departure of supplier from its usual prompt invoicing | 274 |

| Tax Topics - Excise Tax Act - Regulations - Input Tax Credit Information (GST/HST) Regulations - Section 3 - Paragraph 3(a) - Subparagraph 3(a)(ii) | invoice not issued if not sent | 244 |

| Tax Topics - Excise Tax Act - Section 168 - Subsection 168(9) | possible deposits subsequently may have been applied by agreement as payments on account | 233 |

| Tax Topics - Excise Tax Act - Section 221 - Subsection 221(2) | unregistered purchaser | 35 |

| Tax Topics - Excise Tax Act - Schedules - Schedule V - Part I - Section 9 - Subsection 9(2) | sale by corporation not exempted | 30 |

Thimo v. The Queen, 2017 TCC 164

Operations at an individual’s swimming school were suspended as a result of charges brought against him respecting alleged misconduct with a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 141.01 - Subsection 141.01(2) | no ITCs respecting services of criminal counsel which permitted an individual to resume a business | 258 |

572256 Ontario Limited v. The Queen, 2017 TCC 108 (Informal Procedure)

Paris J found that, notwithstanding the absence in evidence of a written agency agreement, a corporation (SVO) had purchased property as agent for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Agency | property found to be held as agent notwithstanding missing written agreement | 316 |

Le Groupe PPP Ltée v. The Queen, 2017 TCC 2, briefly aff'd 2018 FCA 123

A Quebec company (“PPP”) through car dealers offered motor vehicle replacement “warranties,” which, in the event of the loss of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 175.1 | “warranties” funding the incremental cost of a new vehicle after complete loss of old vehicle likely were insurance policies and were not re quality, fitness or performance | 345 |

| Tax Topics - General Concepts - Illegality | whether a product was an insurance policy did not turn on whether the provider was a properly licensed insurer | 216 |

Gemeente Woerden (Municipality of Woerden) v. Staatsecretaris van Financiën (Secretary of State for Finance, Netherlands), C:2016:466 (European Court of Justice (10th Chamber) )

The named Netherlands municipality did not provide two buildings constructed by it to the mostly VAT-exempt building users (e.g., schools)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 141.01 - Subsection 141.01(1.1) | sale of a building at 10% of cost to an intermediary for 90% non-taxable use entitled the vendor to full ITCs | 417 |

630413NB Inc. v. The Queen, 2016 TCC 156 (Informal Procedure)

A group of four corporations and their ultimate individual shareholder were unsuccessful in generating input tax credits for GST/HST on legal fees...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Business | alleged business of assuming litigation not caried out in business-like manner | 269 |

Airtours Holidays Transport Ltd. v. HMRC, [2016] UKSC 21

In 2002, the appellant (“Airtours”), which was in financial difficulty, instigated the preparation of a report by an accounting firm...

Andrei 95 Holdings Ltd. v. The Queen, 2015 TCC 224 (Informal Procedure)

The taxpayer was denied ITCs in respect of legal fees on the basis that it did not incur the legal fees in the course of any commercial activity....

Bijouterie Almar Inc. v. The Queen, 2010 TCC 618, [2010] GSTC 181

The Minister disallowed the ITCs claimed for $15 million of gold jewellery purchases made over four years on the grounds inter alia that the...

| Other locations for this summary | |

|---|---|

| Tax Topics - Excise Tax Act - Regulations - Input Tax Credit Information (GST/HST) Regulations - Section 3 - Paragraph 3(c) - Subparagraph 3(c)(iv) | "assorted gold jewellery" was sufficient description of bulk purchase |

Lavoie v. The Queen, 2014 DTC 1104 [at at 3218], 2014 TCC 68

The taxpayer's uncontradicted evidence was that his cottage in PEI was used approximately 170 days in a given year, only 10 of which were solely...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 163 - Subsection 163(2) | deducting home renovations tenuously related to home office was not grossly negligent | 196 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(h) | cottage used 10 days for personal use and 160 days for business was primarily for business use | 57 |

PDM Royalties Limited Partnership v. The Queen, 2013 TCC 270

The limited partnership units of the appellant were held by a sub-trust (the "Trust") of an income fund (the "Fund"). Unit subscription proceeds...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Regulations - Input Tax Credit Information (GST/HST) Regulations - Section 2 - Intermediary | no allocation on invoices | 129 |

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Recipient | intragroup expense-bearing agreement did not change the recipient of services rendered on IPO | 280 |

WHA Ltd. v. Revenue and Customs Commissioners, [2013] UKSC 24, [2013] 2 All ER 908

The appellant (WHA) was an affiliate of an English company (NIG) which issued motor breakdown insurance to car owners. The NIG policies indicated...

HMRC v. Aimia Loyalty UK Ltd, [2013] UKSC 15

{kind=link}

Reluxicorp Inc. v. The Queen, [2011] GSTC 138, 2011 TCC 336

The registrant was a hotel company that paid franchise fees to a hotel franchise ("Marriott") in the United States. Marriott's fees were based on...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Exclusive | 75% was not substantially all | 261 |

| Tax Topics - Excise Tax Act - Section 217 - Imported Taxable Supply | 173 | |

| Tax Topics - Excise Tax Act - Section 298 - Subsection 298(4) - Paragraph 298(4)(a) | no indication of advice sought as to whether an agency relationship | 116 |

Lyncorp International Ltd. v. The Queen, 2010 DTC 1351 [at at 4335], 2010 TCC 532, aff'd 2012 DTC 5032 [at 6684], 2011 FCA 352

The taxpayer, owned and operated by Mr. Mullen, invested in shares and made non-interest bearing loans to a number of corporate ventures to which...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 3 | 153 |

General Motors of Canada Limited v. The Queen, [2008] GSTC 41, 2008 TCC 117, aff'd [2009] GSTC 64, 2009 FCA 114

The Appellant (a car manufacturer) was the administrator of various defined benefit pension plans for its employees. It directed the trustee of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Financial Service | 95 | |

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Recipient | employer was contractually obligated for, and the recipient of portfolio advisory fees for employees' pension fund | 78 |

Y S I's Yacht Sales International Ltd v. The Queen, 2007 TCC 306

Woods, J. accepted that an agreement pursuant to which the appellant ("YSI") agreed to contract with suppliers in connection with refurbishing a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Agency | 93 |

Kretztechnik AG v Finanzamt Linz, [2005] EUECJ C-465/03, [2006] BVC 66 (ECJ (1st Chamber))

Kretztechnik raised capital through a share issue. The issue of shares did not constitute a supply of services, but it was held that the cost of...

A & W TradeMarks Inc. v. The Queen, 2005 TCC 493 (Informal Procedure)

The appellant, which became a wholly-owned subsidiary of a new income fund (the “Fund”), incurred $78,000 in fees directly to an investment...

Edible What Candy Corp. v. R., [2002] GSTC 33 (TCC)

The taxpayer was found to have made a misrepresentation attributable to neglect when it claimed input tax credits for GST incurred before it...

BJ Services Co. Canada v. The Queen, [2002] GSTC 124 (TCC)

A Canadian public company ("Nowsco") that was engaged in the provision of oil field services incurred significant fees for services rendered by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 141.01 - Subsection 141.01(2) | s. 141.01 was apportionment provision not applying where registrant only making taxable supplies | 181 |

Customs and Excise Commissioners v. Redrow Group plc, [1999] UKHL 4, [1999] 2 All ER 13, [1999] 1 WLR 408

As an incentive to purchasers of its new homes, a residential home developer entered into agreements with prospective purchasers and real estate...

Hleck, Kanuka, Thuringer v. The Queen, [1994] GSTC 46 (TCC)

In finding that GST on an airline ticket purchased by a law firm in order for the wife of one of its partners to attend a conference with him, was...

P & O (Dover) Ltd. v. Commissioners of Customs and Excise, [1992] V.A.T.T.R. 221

The appellant along with seven individual employees was charged with manslaughter in connection with the sinking of its vessel. The appellant's...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Recipient | employer the recipient of criminal counsel services | 156 |

Turner v. Customs and Excise Commissioners, [1992] BTC 5082 (Q.B.D.)

The appellant, who was ordered to pay the costs of the winning side in an unsuccessful lawsuit including VAT, was not entitled to a credit for...

Administrative Policy

GST/HST Notice 339, “Input Tax Credits Related to Dental Practices,” October 2024

- Davis Dentistry confirmed input tax credit (ITC) claims of a professional practice on the basis that a portion of its supplies to each...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Schedules - Schedule VI - Part II - Section 11.1 | 235 |

25 April 2023 GST/HST Ruling 202403 - Eligibility for employer to claim ITCs on amounts related to investment management services for pooled funds of an insurer

The Employer, as administrator for pension plans for its employees, contracted with the Insurer for the Insurer to provide certain pension...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 131 - Subsection 131(1) - Paragraph 131(1)(c) - Subparagraph 131(1)(c)(i) | s. 131(1)(c) could deem management fees of insurer to segregated funds to be taxable consideration | 361 |

May 2019 CPA Alberta CRA Roundtable, GST Session – Q.8

Can input tax credits be claimed by a builder where invoices are issued subsequent to the date of self assessment on substantial completion and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 133 | s. 133 determines time of acquisition for ITC purposes | 209 |

| Tax Topics - Excise Tax Act - Section 191 - Subsection 191(3) | supplies acquired prior to self-supply time generate ITCs even if only invoiced later | 125 |

| Tax Topics - Excise Tax Act - Section 141.01 - Subsection 141.01(2) | purpose of acquisition is assessed at time agreement is entered into | 214 |

17 May 2017 Interpretation 174642

Shortly before the occupancy of a newly constructed apartment complex (expected to be predominantly occupied by students), LP#1 purchases the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 191 - Subsection 191(3) | headlease structure of a student residence avoided triggering self-supply rule | 483 |

| Tax Topics - Excise Tax Act - Schedules - Schedule V - Part I - Section 6.11 | headlease of MURC not exempt where used by lessee more than 10% in short-term rentals | 128 |

| Tax Topics - Excise Tax Act - Schedules - Schedule V - Part I - Section 5 | claiming of ITC generated subsequent taxable sale | 154 |

13 December 2017 Interpretation 187306

Before going on to reject the proposition that an ITA s. 16.1 election had the effect of deeming the lessee to have acquired the leased property...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 225.1 - Subsection 225.1(2) - B | s. 16.1 election does not cause a leased property to be a capital property | 310 |

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Capital Property | s. 16.1 election did not deem leased property to be capital property | 55 |

2 August 2017 Ruling 182285

The Ontario Rebate for Electricity Consumers Act, 2016 (Ontario Rebate Act), provides financial assistance to certain Ontario electricity...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Consideration | Ontario electricity rebate does not reduce the consideration for the supply | 75 |

28 April 2017 Interpretation 154249

An ATM provider (the Vendor) agreed that X’s acquisition of the Vendor's ATMs would be financed by Vendor selling the ATMs to Lessor, with...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Recipient | failure of person contractually liable to pay software licence fees to acquire a licence indicated it was an agent rather than recipient | 355 |

10 February 2017 GST/HST Ruling 162056 - Application of the GST/HST to an investment transaction

A Canadian registrant (Investor) enters into an agreement with a Canadian corporation (Corporation 1) under which it pays lump sums in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Debt Security | royalty agreement is not a debt security unless a minimum royalty is specified | 267 |

| Tax Topics - Excise Tax Act - Section 182 - Subsection 182(1) | buyout of royalty agreement not subject to s. 182 | 185 |

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Commercial Activity | receipt of royalty not considertion for a taxable supply | 121 |

14 October 2016 Interpretation 170549

ACo and BCo, which were co-tenants of a property in construction held through a Nominee, signed an agency agreement in which Nominee was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 273 - Subsection 273(1) | Westcan test for JV, co-tenancy was JV | 190 |

| Tax Topics - Excise Tax Act - Section 240 - Subsection 240(3) - Paragraph 240(3)(a) | nominee accepted as registrant | 167 |

| Tax Topics - General Concepts - Agency | co-owners required to report pro rata portions of sale made by their agent | 209 |

26 February 2015 CBA Roundtable, Q. 33

Can a person claim input tax credits in a reporting period after its registration in respect of GST/HST paid in periods where the person was a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 225 - Subsection 225(1) | ITCs for prior unregistered periods | 38 |

GST/HST Technical Information Bulletin B-032 “Expenses Related to Pension Plans” 17 November 2015

Where an employer retains an investment manager for the company pension plan, and the pension plan pays the manager directly, CRA considers there...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Recipient | 349 | |

| Tax Topics - Excise Tax Act - Section 172.1 - Subsection 172.1(5) | imputation of a supply of an investment management service by employer to RPP where the fee was incured by the employer | 143 |

Memorandum 8-3 - "Calculating Input Tax Credits"

First-order v. second-order supplies

27. Where inputs are acquired, imported or brought into a participating province for consumption or use for...

GST/HST Notice "Bare Trusts, Nominee Corporations and Joint Ventures" February 2014

After noting that "a trustee of a bare trust, for example, a nominee corporation, may act as an agent of the participants in a joint venture by...

CBAO National Commodity Tax, Customs and Trade Section – 2013 GST/HST Questions for Revenue Canada, Q. 26.

An Ontario purchaser ("Ontario Co") remitted HST to a Quebec supplier ("Quebec Co," a GST registrant) on the basis of its view that the place of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 222 - Subsection 222(1) | deemed trust re HST collected in error | 130 |

| Tax Topics - Excise Tax Act - Section 225 - Subsection 225(1) | HST collected in error | 130 |

CBAO National Commodity Tax, Customs and Trade Section – 2013 GST/HST Questions for Revenue Canada, Q. 23 ("Pre-Incorporation Contracts")

In response to a question on pre-incorporation contracts, CRA stated that even in jurisdictions where the corporate legislation did not address...

24 June 2011 Headquarters Letter Case No. 126708

After using a property partly to generate revenues from commercial activities and partly from exempt activities (programs geared to children under...

7 June 2011 Headquarters Letter Case No. 132324

A Canadian company enters into an agreement with a non-resident registered service provider for its equipment to be refurbished outside Canada,...

24 February 2011, CBA/CRA GST Round Table, Q. 15 - "Amalgamation & Successor Corp's ITC Entitlement"

In a corporate reorganization involving a GST registrant that is engaged exclusively in commercial activities, assets are first transferred to a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 206 - Subsection 206(2) | 179 | |

| Tax Topics - Excise Tax Act - Section 271 | 179 |

16 March 2009 Interpretation Case No. 110027

A real estate nominee not only holds legal title to project real property but also, at the direction of the beneficial owners, enters into...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 240 - Subsection 240(1) | beneficial owners rather than nominee for condo project are considered to be engaged in commercial activity | 215 |

| Tax Topics - Excise Tax Act - Section 177 - Subsection 177(1.1) | real estate nominee can make election | 62 |

GST New Memorandum 8.1, ITCs—General Eligibility Rules, May 2005

Meaning of “acquire”

9. The word “acquire” is not defined in the Act. The ordinary dictionary definition of the term “acquire” is to...

P-112R "Assessment of Tax Payable where a Purchaser is Insolvent" 9 March 2000

Where a registrant which hads claimed ITCs for accounts payable goes bankrupt, and the supplier then claims a bad debt deduction in computing net...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 296 - Subsection 296(1) - Paragraph 296(1)(b) | assessment of insolvent purchaser | 140 |

12 April 2000 Interpretation No. 8394

Respecting the construction by a corporation of a facility and its sale to a subsidiary for lease back to that corporation for use by it in...

16 August 1994 Headquarter Letter

"To be entitled to an ITC in respect of Division III tax, the person must be the de facto importer of the good (i.e., the person who caused the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 169 - Subsection 169(4) | 120 | |

| Tax Topics - Excise Tax Act - Section 180 | 120 |

14 July 1997 Ruling R-11595-1 95 GAPR 425

GST paid for various services provided to a corporation relating to its issuance of bonds to Canadian residents and non-resident investors would...

GST/HST Technical Information Bulletin B-068 "Bare Trusts" Amended 10 January 2005

[A] bare trust is not engaged in commercial activities and is not entitled to claim ITCs. Instead, the beneficial owners are entitled to claim...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 240 - Subsection 240(1) | bare trustee required to register if it charges fees | 58 |

| Tax Topics - General Concepts - Agency | 226 | |

| Tax Topics - Excise Tax Act - Section 269 | transfer of registered title by (or to) bare trustee generally is for nil consideration | 102 |

GST/HST Policy Statement P-045: Butterfly Transactions 9 November 1992 (Obsolete February 2012)

Can a corporation ("Newco") which was incorporated solely for the purposes of facilitating the transfer of property between two other...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 272 | deemed no-supply on wind-up denies ITC to predecessor | 66 |

GST M 400-1-2 "Documentary Requirements" under "Types of Input Tax Credits"

"'Exclusively' means 90 per cent or more consumption, use or supply in the course of commercial activities".

GST M 300-7 "Value of Supply" under "Nil Consideration"

The deeming by s. 153(3) of a supply to be made for nil consideration does not alter the status of the supply as a taxable supply for other...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 153 - Subsection 153(1) | 25 |

Element B

Paragraph (b)

See Also

St-Joseph Immobilier Inc. v. Agence du revenu du Québec, 2024 QCCQ 766, aff'd 2025 QCCA 745

In 1984, the plaintiff (St-Joseph) acquired a 12-storey tower used only for commercial rentals, and between 1997 and 2002, converted four of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 141.1 - Subsection 141.1(3) - Paragraph 141.1(3)(a) | transformation of 2 floors of commercial building to residential use did not qualify as a “cessation” of commercial activity under s. 141.1(3)(a) | 198 |

| Tax Topics - Excise Tax Act - Section 169 - Subsection 169(1) - Element B - Paragraph (c) | conversion of 2 floors of building from commercial to residential use did not generate ITCs based on "cessation" of commercial activity | 170 |

1378055 Ontario Limited v. The Queen, 2019 TCC 149

The appellant (“137ON”), which was a corporation owned by members or affiliates of the Foley family that owned 10 residential rental...

Administrative Policy

19 August 1994 GST/HST Interpretation - GST Treatment of Leasehold Interest/Improvements, Cash Inducements and Entitlements to (ITCs)

The registrant, a financial institution, leases premises for various branch offices. Most leases negotiated require the landlord to pay to the...

Paragraph (c)

See Also

St-Joseph Immobilier inc. v. Agence du revenu du Québec, 2025 QCCA 745

St-Joseph incurred costs in converting the 1st and 2nd floors of a 12-storey mixed-use tower from commercial rental use into rental seniors’...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 141.1 - Subsection 141.1(3) - Paragraph 141.1(3)(a) | the transformation of 2 floors of commercial building to residential use did not qualify as a “termination” of commercial activity for QST purposes | 226 |

St-Joseph Immobilier Inc. v. Agence du revenu du Québec, 2024 QCCQ 766, aff'd 2025 QCCA 745

Starting in 2002, St-Joseph incurred costs in converting the 1st and 2nd floors of a 12-storey mixed-use tower from commercial rental use into...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 141.1 - Subsection 141.1(3) - Paragraph 141.1(3)(a) | transformation of 2 floors of commercial building to residential use did not qualify as a “cessation” of commercial activity under s. 141.1(3)(a) | 198 |

| Tax Topics - Excise Tax Act - Section 169 - Subsection 169(1) - Element B - Paragraph (b) | costs of converting 2 floors of commercial building to residential use were not an “improvement” (i.e., ACB increase) to the commercial-use building portion | 171 |

1378055 Ontario Limited v. The Queen, 2019 TCC 149

Individuals within the same extended family and a corporation controlled by family trusts sent vaguely worded invoices to a family company (the...

Subsection 169(1.1)

Administrative Policy

Memorandum 8-3 - "Calculating Input Tax Credits"

Example of allocation between improvements and repairs (para. 65)

Example

In March 2014, a landlord … engages a contractor to make improvements...

Subsection 169(2) - Credit for Goods Imported to Provide Commercial Service

Administrative Policy

21 October 2004 Headquarter Letter RITS 38435

Where a registrant imports tangible personal property of an unregistered non-resident for the purpose of providing storage services to the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 179 - Subsection 179(2) | 90 |

GST M 300-9 "Imported Services and Intangible Property"

When an imported taxable supply is used partly in a commercial activity, registrants will be able to claim an input tax credit on the GST payable...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Subsection 218.1 - Subsection 218.1(1) - Paragraph 218.1(1)(a) | 0 |

Subsection 169(4) - Required Documentation

Cases

Systematix Technology Consultants Inc. v. Canada, 2007 FCA 226, aff'g 2006 TCC 277

The appellant provided IT services through subcontractor consultants. The consultants in issue variously did not provide registration numbers on...

See Also

267 O'Connor Limited v. The King, 2024 TCC 161 (Informal Procedure)

In the settlement of an action against it by a third party (“Starwood”) for a failure of a property sale agreement to Starwood to close, the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 169 - Subsection 169(1) | damages paid by the vendor under a failed realty sale did not generate ITCs notwithstanding some IP transferred to it | 257 |

| Tax Topics - Excise Tax Act - Section 182 - Subsection 182(1) | s. 182(1) inapplicable where damages paid by supplier rather than recipient | 178 |

Entrepôt Frigorifique International Inc. v. The King, 2024 TCC 78

The appellant (Frigo) was assessed beyond the normal four-year period under s. 298(1)(a) to deny input tax credits (ITCs) for GST charged to it by...

Axamit Versa Inc. v. The King, 2022 TCC 163 (Informal Procedure)

The ARQ denied input tax credits claimed by Axamit for its 2015 year regarding GST charged by its landlord, because Axamit had not provided the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Regulations - Input Tax Credit Information (GST/HST) Regulations - Section 2 - Supporting Documentation | the GST registration number need not be set out in a document issued to the ITC claimant by the supplier | 303 |

| Tax Topics - Excise Tax Act - Section 223 - Subsection 223(2) | purpose of s. 223(2) | 253 |

CFI Funding Trust v. The Queen, 2022 TCC 60

A securitization trust (“CFI”) used a concurrent lease structure under which it became the concurrent (head) lessee of automobiles from...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Regulations - Input Tax Credit Information (GST/HST) Regulations - Section 2 - Supporting Documentation | supporting documentation can be originated by the recipient and be in electronic form | 364 |

Mediclean Incorporated v. The Queen, 2022 TCC 37

The taxpayer, which was engaged in the business of providing professional cleaning services, began to pay GST to its cleaning staff after they...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 261 - Subsection 261(1) | ITCs denied to a registrant who paid HST to unregistered suppliers - but s. 261(1) rebate accorded under s. 296(2.1) | 390 |

| Tax Topics - Excise Tax Act - Section 296 - Subsection 296(2.1) | Minister required to apply rebate for HST allegedly paid out of negligence | 275 |

| Tax Topics - Excise Tax Act - Section 298 - Subsection 298(4) - Paragraph 298(4)(a) | no carelessness in being misled by literal statement on CRA website | 177 |

| Tax Topics - Excise Tax Act - Section 285 | a reasonable person could have concluded that professional advice was not required | 178 |

| Tax Topics - Excise Tax Act - Section 169 - Subsection 169(5) | CRA allowed ITCs for suppliers whose registration numbers were not obtained but which in fact were registrants | 93 |

| Tax Topics - Excise Tax Act - Section 225 - Subsection 225(1) - A - Paragraph A(a) | unregistered independent-contractor staff who were mistakenly paid HST were required to file returns and remit such tax | 193 |

Construction S.Y.L. Tremblay Inc. v. Agence du revenu du Québec, 2018 QCCA 552

In the federal Construction S.Y.L. Tremblay case, Bédard J found that house-repair invoices, that did not give the house address or describe the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Stare Decisis | Court of Quebec not bound by Tax Court decisions/stare decisis does not preclude relitigation where unfairness would otherwise result | 239 |

| Tax Topics - Excise Tax Act - Regulations - Input Tax Credit Information (GST/HST) Regulations - Section 3 - Paragraph 3(c) - Subparagraph 3(c)(iv) | failure of invoices to describe the supplies could not be remedied by testimony | 425 |

| Tax Topics - General Concepts - Abuse of Process | taxpayer’s attempt to relitigate an adverse TCC decision in the Court of Quebec was an abuse of process given that the new evidence to be tendered did not address its defective invoices | 412 |

Agence du revenu du Québec v. Stamatopoulos, 2018 QCCA 474

A taxpayer (Stamatopoulos) serviced clothing manufacturers by securing sewing services for clothes that then were delivered to the manufacturer. ...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Regulations - Input Tax Credit Information (GST/HST) Regulations - Section 2 - Intermediary | ARQ failed to establish that a named supplier to the taxpayer did not act as a supplier or intermediary | 442 |

| Tax Topics - General Concepts - Onus | onus shifted to ARQ once the taxpayer had demonstrated that he had business deaings with issuer of mooted invoice | 209 |

Barlis 06 - Investimentos Imobiliários e Turísticos SA v. Autoridade Tributária e Aduaneira, [2016] EUECJ C-516/14 (European Court of Justice (Fourth Chamber))

Barlis, which operated hotels in Portugal, was denied the deduction of input tax respecting legal services on the basis that the four invoices...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Regulations - Input Tax Credit Information (GST/HST) Regulations - Section 3 - Paragraph 3(c) - Subparagraph 3(c)(iv) | mere technical non-compliance with VAT requirements for complete invoices should not prevent input tax claims | 156 |

SNF L.P. v. The Queen, 2016 TCC 12

The appellant ("SNF"), which carried on a metal recycling business, acquired metal scrap from 12 suppliers, who were registered for GST and QST...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Regulations - Input Tax Credit Information (GST/HST) Regulations - Section 2 - Intermediary | intermediary need not carry on business and may be a nominee | 131 |

| Tax Topics - Excise Tax Act - Section 261 - Subsection 261(1) | no rebate entitlement for an error caused by the applicant’s own inattention and carelessness | 114 |

| Tax Topics - General Concepts - Agency | "prête‑nom" contract is a valid contract | 217 |

Tan v. The Queen, 2015 TCC 121 (Informal Procedure)

The appellant incurred expenditures for her restaurant business, for which several of her suppliers provided her with receipts but did not and...

Constructions Marabella Inc. v. The Queen, 2012 TCC 397 (Informal Procedure)

The registrant's sole shareholder and president ("Mirabella") was a building contractor who subcontracted various elements of construction. ...

Comtronic Computer Inc. v. The Queen, 2010 TCC 55

The GST registration number of the supplier shown on the invoices provided to the Appellant ("Comtronic") was not that of the suppliers but was a...

Key Property Management Corporation v. The Queen, 2004 TCC 210

The appellant appealed the denial of several ITCs for legal services; some of the denials were upheld due to lack of documention. In this regard,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Service - Paragraph (c) | maintenance staff working for indeterminate group companies were not their employees cf. for employees working for group companies in pre-agreed proportions | 258 |

| Tax Topics - General Concepts - Agency | maintenance employees working for indeterminate group companies were not hired as agent for those companies | 174 |

San Clara Holdings Ltd. v. The Queen, [1995] E.TC 6 (TCC)

The registrant was prohibited from claiming input tax credits in respect of amounts paid by it to subcontractors who had not provided their GST...

Administrative Policy

May 2015 Alberta CPA Roundtable, GST Q. 6

In a corporate group, on entity (Corp A) makes the purchases and then journal entries transfer the expense over to the correct entity (Corp B)....

20 December 2012 Ruling Case No. 145166

As a result of delays in processing accounts payable invoices, two companies do not have monthly input tax credit accruals in their accounts that...

16 August 1994 Headquarter Letter

In a situation where an unregistered non-resident was listed as the importer of record, and it supplied goods to a registrant who wishes to obtain...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 169 - Subsection 169(1) | 74 | |

| Tax Topics - Excise Tax Act - Section 180 | 120 |

GST/HST Memorandum 8.4 Documentary Requirements for Claiming Input Tax Credits August 2012

14. To claim an ITC, a registrant must first obtain the proper documentary evidence to support the claim. Paragraph 169(4)(a) establishes the...

Paragraph 169(4)(a)

See Also

Fiera Foods Company v. The King, 2023 TCC 140

Two bakery plants of Fiera were staffed in significant part by temporary workers (“TWs”), who were sourced from third parties (the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Regulations - Input Tax Credit Information (GST/HST) Regulations - Section 2 - Supporting Documentation | registrant not required to demonstrate that invoice received in name of supplier was in fact “issued” by it | 550 |

| Tax Topics - Excise Tax Act - Section 169 - Subsection 169(1) | no requirement that the tax be payable to a particular person | 288 |

Paragraph 169(4)(b)

Administrative Policy

7 April 2022 CBA Roundtable, Q.12

A (GST/HST-registrant) public service body which acquires real property not primarily in the course of its commercial activities is required...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 228 - Subsection 228(6) | a PSB rebate for purchased real estate can be deducted from the GST/HST remittance for the purchase by filing the rebate and purchase returns together | 252 |

Subsection 169(5) - Exemption

See Also

Mediclean Incorporated v. The Queen, 2022 TCC 37

Although the appellant did not obtain GST/HST registration numbers from any of its suppliers (the “Subcontractors”), CRA allowed it to claim...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 261 - Subsection 261(1) | ITCs denied to a registrant who paid HST to unregistered suppliers - but s. 261(1) rebate accorded under s. 296(2.1) | 390 |

| Tax Topics - Excise Tax Act - Section 169 - Subsection 169(4) | Systematix applied to deny ITCs where only BNs, not registration numbers, obtained | 130 |

| Tax Topics - Excise Tax Act - Section 296 - Subsection 296(2.1) | Minister required to apply rebate for HST allegedly paid out of negligence | 275 |

| Tax Topics - Excise Tax Act - Section 298 - Subsection 298(4) - Paragraph 298(4)(a) | no carelessness in being misled by literal statement on CRA website | 177 |

| Tax Topics - Excise Tax Act - Section 285 | a reasonable person could have concluded that professional advice was not required | 178 |

| Tax Topics - Excise Tax Act - Section 225 - Subsection 225(1) - A - Paragraph A(a) | unregistered independent-contractor staff who were mistakenly paid HST were required to file returns and remit such tax | 193 |

Dr. Kevin L. Davis Dentistry Professional Corporation v. The Queen, 2021 TCC 25, aff'd 2023 FCA 76

A professional corporation’s orthodontics practice claimed input tax credits on the basis of an administrative arrangement of CRA with the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Schedules - Schedule VI - Part II - Section 11.1 | orthodontic practices make two supplies of services and devices | 383 |

| Tax Topics - Excise Tax Act - Regulations - Input Tax Credit Information (GST/HST) Regulations - Section 3 - Paragraph 3(b) | invoices showing nil tax and not allocating between the included zero-rated and exempt supply complied with s. 3 | 369 |

Administrative Policy

8 March 2018 CBA Commodity Tax Roundtable, Q.15

After noting that, to comply with s. 169(4)(a), the registration number supplied by a vendor “must be valid at the time the tax in respect of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Regulations - Input Tax Credit Information (GST/HST) Regulations - Section 3 - Paragraph 3(b) - Subparagraph 3(b)(i) | subject to s. 169(5), supplier’s registration number must be valid on due date | 310 |

GST M 400-1-2 "Documentary Requirements" under "Meals and Entertainment - Reimbursements"

Discussion of simplified "6/106" method for claiming ITCs re meal and entertainment expenses.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Commercial Activity | 10 |