Subsection 5902(1)

Administrative Policy

10 September 2013 Internal T.I. 2010-0387631I7 - Surplus accounts; Disposition of foreign affiliate

{kind=link}

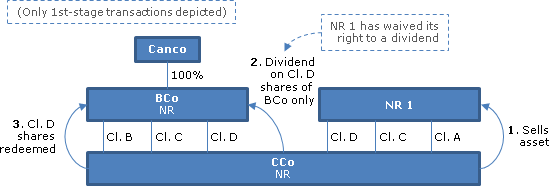

Canco owns all of the shares of BCo (a foreign affiliate) which in turn owns redacted percentages of the Class B, D and D shares of CCo (also a...

Subsection 5902(2)

Administrative Policy

7 February 1994 External T.I. 9309865 F - 6363-1 Foreign Affiliates / Cross-shareholdings / Surplus

Where a corporation resident in Canada owns 95% of the common shares of FA1 which, in turn, owns 100% of the common shares of FA2 which, in turn,...