Advance Pricing Arrangement - Program report - 2016

Disclaimer

We do not guarantee the accuracy of this copy of the CRA website.

Scraped Page Content

Advance Pricing Arrangement - Program report - 2016

On this page

- Executive summary

- Introduction

- Background

- APA program: 2016 calendar year

- Applications

- Production and inventory

- Table 1: APA program application and inventory statistics

- Intergovernmental status

- Completion times

- Table 2: APA program completion time statistics

- Intercompany transactions

- Table 3: APA program transaction type statistics (since program inception)

- Transfer pricing methodologies

- Table 4: APA program transfer pricing methodology statistics (since program inception)

- Participation by industrial sector

- Participation by country

- Participation by Canadian province

- Closing remarks

- How to contact us

Executive summary

The Canada Revenue Agency’s (CRA) Advance Pricing Arrangement (APA) program is administered through the CRA’s Competent Authority Services Division (CASD), which is part of the International and Large Business Directorate (ILBD), International, Large Business and Investigations Branch (ILBIB).

The APA program is a proactive service offered by the CRA to assist taxpayers in resolving transfer pricing disputes that may arise in future tax years. The primary objective of the program is to provide increased certainty with respect to future transfer pricing issues in a manner consistent with the Income Tax Act (ITA), and guidance delivered through the CRA’s information circulars (IC) and by the Organisation for Economic Co-operation and Development (OECD).

The CRA has published an annual report on its APA program since the 2001-2002 fiscal year. Beginning in 2016, the annual report will be based on a calendar year format and given that the 2016 year is a transitional year for reporting purposes, we have included APA results for both the fiscal year and the calendar year. A summary of the key findings presented in this year’s calendar year report is provided below:

- Measured on the basis of the number of pre-file meetings conducted with taxpayers over the course of the 2016 calendar year, the CRA had 23 applicants to the program this past year.

- The calendar year opened with an active case inventory of 107 APAs. Twelve new cases were accepted into the program, 3 cases were withdrawn or unresolved, while 26 cases were completed, resulting in a closing inventory of 90 cases at the end of the period.

- 90% of all cases currently in process involve taxpayers seeking an APA on a bilateral or multilateral basis, as opposed to 10% of taxpayers seeking an APA on a unilateral basis.

- The average time to conclude a bilateral APA from acceptance into the program to completion was 47.3 months.

- Cases involving transfers of tangible property constituted over one-half of APAs in process (63%). Cases involving intangible property, intra-group services and financing represented 17%, 17% and 3% of cases, respectively.

- The transactional net margin method (TNMM) continued to be the most frequently employed transfer pricing methodology. A TNMM was proposed in 69% APAs in process. The cost plus and profit split were the next most popular method being proposed in 11% and 10% of cases, respectively. The comparable uncontrolled price (CUP) method and resale price methodologies were proposed in 9% and 1% of cases, respectively.

- APAs involving taxpayers with operations in automobile and other transportation equipment represented 21% of in process APAs at the end of the period. APAs pertaining to the health sector were the second most prevalent representing 12% of the cases in process. APAs pertaining to the computer and electronics industry, as well as the petroleum industry, and the metals and minerals industry were the next most common each representing 8% of cases in process.

- The composition of bilateral and multilateral APAs continued to reflect the significant flow of goods and services exchanged between Canada and the United States. Although lower than the proportion historically observed, APAs involving the United States represented 56% of APAs in process.

- APAs with Canadian corporations headquartered in the Province of Ontario continue to represent over one-half of all APAs completed and in process.

Introduction

This year’s APA report is the fifteenth of its kind issued by the CRA on the APA program. The report is targeted to taxpayers, tax representatives, and international tax administrations. The key objectives of the report include:

- Enhancing awareness of the CRA’s APA program;

- Notifying readers of changes to the APA program;

- Providing an operational status update; and,

- Identifying issues that may impact the APA program in future years.

Maintaining the approach of previous publications, this year’s report continues to place a heavy emphasis on statistical analysis and quantitative data with a particular aim of providing insight to the approaches taken by the CRA and its treaty partners on difficult transfer pricing issues.

Background

The APA program is delivered through the CRA’s Competent Authority Services Division (CASD), which is part of the International and Large Business Directorate (ILBD), International, Large Business and Investigations Branch (ILBIB).

The program is a service offered by the CRA to assist taxpayers in proactively resolving prospective transfer pricing disputes. The primary objective of the program is to provide increased certainty with respect to transfer pricing methodologies to be applied to future intercompany transfer pricing transactions in a manner consistent with the Income Tax Act (ITA), and guidance delivered through the CRA’s information circulars (IC) and by the Organisation for Economic Co-operation and Development (OECD).

The APA process is based on cooperation and transparency with the free flow of information. It differs from the CRA’s audit process in that it focuses on prospective or future tax years rather than tax years that have already elapsed. In essence, an APA is an arrangement between a taxpayer and a tax administration that sets out an appropriate transfer pricing methodology, to be used on a prospective basis, for establishing a transfer price which is arm’s length for the transactions between related parties. The establishment of a transfer price embodies the arm’s length principle as described by the OECD’s Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations and the CRA’s current version of IC87-2 International Transfer Pricing.

The APA process is initiated by Canadian taxpayers through contact with the CASD. For further information on the CRA’s APA program, please refer to the current version of IC94-4 International Transfer Pricing: Advance Pricing Arrangements (APAs).

APA program: 2016 calendar year

The following section provides an operational overview of the APA program along with current trends, issues, and changes to the program. Specific topics that will be examined in greater detail include:

- Applications;

- Production and program inventory;

- Intergovernmental status;

- Completion times;

- Intercompany transactions;

- Transfer pricing methodologies;

- Participation by industrial sector;

- Participation by country; and,

- Participation by Canadian province.

Applications

Taxpayers interested in obtaining an APA must first submit a pre-file package to the Director of CASD in order to request an APA pre-file meeting. As much as possible, an APA request-information package should include all the information listed in Appendix I of the current version of the CRA’s IC94-4. CASD will review the package and, if satisfied that it is complete, will contact the taxpayer with possible date(s) for a pre-file meeting.

Pre-file meetings, which take place between a taxpayer and the CRA, provide an opportunity for the taxpayer to learn more about the APA program and for the CRA to obtain clarification on the taxpayer’s business, industry, and most importantly, the requested covered transaction(s). The primary objective of the meeting is to explore the suitability of the taxpayer and the proposed covered transaction(s) for the APA program.

After considering the nature of the request, the availability of information, and the taxpayer’s willingness to address potential issues identified during or after the pre-file meeting, a decision is then taken as to whether or not a taxpayer will be permitted to the next stage of the APA process. Those taxpayers invited to continue on in the process are subsequently required to prepare a detailed APA submission outlining the specifics of the covered transaction(s) including a detailed transfer pricing analysis and all pertinent information necessary for the CRA to review and complete its own transfer pricing analysis. Once the CRA has received and reviewed the taxpayer’s APA submission for completeness, a decision is taken to accept or reject a taxpayer’s request for an APA.

Although a taxpayer’s acceptance into the APA program is not determined at the pre-file stage, the number of pre-file meetings held in a given period can provide a preliminary forecast of future years’ inventory. It can also be used to gauge the current level of interest in the CRA’s APA program. Historically, the CRA has averaged 28 pre-file meetings annually when computed over the past decade. In the 2016 calendar year, the CRA conducted a total of 23 pre-file meetings.

Withdrawals from the APA process can occur during the application stage or after an acceptance of application has been granted to the program. By definition, an application withdrawal occurs when a taxpayer formally engages the CRA in an APA pre-file meeting but either chooses on its own accord not to pursue an APA or is informed by the CRA that the proposed covered transaction(s) is not well suited for the APA program. An APA withdrawal occurs where a taxpayer has provided a detailed APA submission but either is subsequently unable to continue in the APA process or is informed by the CRA that they are not suited for the APA program.

In an effort to maintain transparency in the program and to ensure applicants are able to meet the requirements of an APA, the CRA continues to be proactive at ensuring that taxpayers have the necessary feedback on their proposed transfer pricing methodologies and covered transactions. Based on this feedback, some taxpayers opt not to pursue an APA, while in other instances, the CRA may conclude that it would not be appropriate to accept or pursue an APA with a taxpayer. If the CRA declines an APA request, or chooses not to pursue an APA, taxpayers are provided with an explanation for the CRA’s decision. As an example, the CRA may decline an APA request when the central issue involves a matter that is before the courts. In most cases, however, taxpayers are given an opportunity to make further representations on any outstanding issues that are precluding their acceptance into the program.

APAs are best suited for current transactions that will likely continue on into the future with little to no change to the transactions themselves, and where the underlying assumptions that form the basis of an APA transfer pricing methodology do not change over the duration of both the immediate pre-APA period and the APA period itself. Transactions involving one-time events, such as corporate restructurings of a significant nature, generally reside outside of the intended scope of the APA program. Apart from a refusal by the CRA, other reasons why a taxpayer may not pursue an APA include: financial constraints, significant changes in operations such as a business restructuring, and changes in personnel.

In the 2016 calendar year, there were a total of 5 withdrawals from the APA process, 2 occurred during the application stage and 3 after the applications had been accepted into the program. From an efficiency standpoint, the withdrawal of an APA during the application stage instead of during the post submission stage can represent a significant saving of resources for both taxpayers and tax administrations.

At the close of the most recent calendar year, 17 applications were under consideration for acceptance to the program (that is, instances where a pre-file meeting has occurred between the CRA and a taxpayer, but a taxpayer had yet to provide the APA submission).

Production and inventory

In the 2016 calendar year, 12 new cases were accepted to the program. These new cases are in addition to those cases already reflected as part of inventory from acceptances issued in years past. Outgoing inventory, which includes APAs completed, unresolved, and withdrawn from the program, totalled 29 cases. Closing inventory at the end of the year was 90 cases.

Table 1: APA program application and inventory statistics

| Period | Pre-file meetings | Application withdrawals | Applications pending | Opening APA balance | APAs accepted | APAs completed | APAs unresolved | APA withdrawals | Closing APA balance | Change in inventory from previous period |

|---|---|---|---|---|---|---|---|---|---|---|

| 2016* | 23 | 2 | 17 | 107 | 12 | 26 | 0 | 3 | 90 | -17 |

| 2015** | 24 | 2 | 8 | 109 | 23 | 21 | 1 | 3 | 107 | 12 |

| 2015-16*** | 24 | 3 | 10 | 94 | 25 | 24 | 0 | 0 | 95 | 1 |

| 2014-15 | 28 | 1 | 14 | 110 | 22 | 31 | 1 | 6 | 94 | -16 |

| 2013-14 | 21 | 8 | 9 | 99 | 39 | 25 | 0 | 3 | 110 | 11 |

| 2012-13 | 24 | 3 | 35 | 102 | 21 | 24 | 0 | 0 | 99 | -3 |

| 2011-12 | 34 | 4 | 35 | 96 | 17 | 10 | 0 | 1 | 102 | 6 |

* Statistics for 2016 calendar year. Going forward, the CRA will be reporting statistics on a calendar year basis.

** Unpublished statistics for the 2015 calendar year presented for comparison purposes.

*** Unpublished statistics for the 2015-2016 fiscal year presented for comparison purposes.

Intergovernmental status

Of the 26 completed APAs in the 2016 calendar year, all but two were bilateral agreements with foreign tax administrations. Since the program’s inception, the vast majority of APAs have been bilateral APAs. Including multilateral APAs, 85% (or 243 cases) of the 286 successfully concluded cases have involved at least one other foreign tax administration. For APAs still in process, 81 (or 90%) of the 90 cases, are bilateral or multilateral. It can reasonably be concluded that the CRA and applicants to the APA program continue to be focused on bilateral (or multilateral) arrangements in order to eliminate double-taxation and secure the highest degree of tax certainty.

Completion times

It is the scope and complexity of a case and not the size of the covered transaction(s) or companies involved, along with other factors such as a taxpayer’s cooperation and the availability of necessary quality information, that determine the length of time required to complete an APA. In some instances, cases require a substantially greater investment in the CRA’s time and resources because they cover a particularly complex transaction(s), or because the necessary information needed to complete a transfer pricing analysis is limited in scope. In this respect, readers should be aware that given the relatively small number of cases used in the computation of the CRA’s APA completion time statistics, the figures presented in the following section may be susceptible to biases resulting from the presence of extreme outliers.

Once a case has been accepted into the program, the process that ensues generally requires a substantial investment in time and resources from all stakeholders. Bringing an APA from start to finish is broken down into three distinct stages. These stages are historically described as due diligence, negotiations, and post-negotiations stages.

The due diligence stage begins once a candidate has been accepted into the program and finishes with the completion of a position paper outlining the CRA’s views on the covered transaction(s). Due diligence includes reviewing materials presented by the taxpayer, undertaking site visits, issuing additional queries and/or information requests to permit the CRA to review the APA submission and complete a thorough financial and transfer pricing analysis, and concludes with the formalization of a position for competent authority negotiations.

In the second stage (for bilateral and multilateral APAs only), the CRA engages in government-to-government negotiations with the corresponding foreign tax administration in order to establish an agreement on the approach and transfer pricing methodology to be employed over the course of the APA term. This can often require additional analysis, research, and fact-finding in order to help resolve differences between the CRA’s and a foreign tax administration’s transfer pricing positions.

And finally, the third stage pertains to the documentation and signing of a bilateral/ multilateral understanding between the CRA and a foreign tax administration, and similarly the signing of a corresponding domestic APA between the CRA and the Canadian taxpayer. Depending on the complexity of the transfer pricing methodology agreed to during negotiations, the time required to finalize an APA can vary from case to case.

Focusing on the 24 bilateral APAs closed in the 2016 calendar year, the CRA required on average 30.2 months to complete its due diligence and an analysis on the covered transactions. An additional 5.9 months were needed for negotiations with the corresponding foreign tax administration. And finally, 11.3 months were needed on average to draft and finalize the bilateral and domestic APA agreements. Overall, for cases completed this past fiscal year, 47.3 months were required on average to proceed from acceptance to completion.

Readers should be aware that the total time to complete an APA does not necessarily equate to the sum of the due diligence, negotiations, and post-negotiations stages. In some instances, cases have been put into suspense while the CRA awaits additional information from a taxpayer. Instances of this nature generally occur when a taxpayer is reconsidering their suitability for the APA program or is unable to provide the necessary information needed for the CRA to undertake a thorough financial and transfer pricing analysis. In other instances, delays are due to the fact that the APA program requires the simultaneous exchange of position papers between tax administrations prior to commencing negotiations. It should be noted any such delays are included in the times of completion at the respective stages of the APA process.

Table 2: APA program completion time statistics

| Period | Type | Number of cases | Due diligence (Months) | Negotiations (Months) | Post-negotiations * (Months) | Average time: Acceptance to completion (Months) | Median time: Acceptance to completion (Months) |

|---|---|---|---|---|---|---|---|

| 2016** | Bilateral/Multilateral | 24 | 30.2 | 5.9 | 11.3 | 47.3 | 42.7 |

| 2015-16 | Bilateral/Multilateral | 21 | 34.3 | 6.0 | 12.4 | 52.7 | 49.0 |

| 2014-15 | Bilateral/Multilateral | 30 | 31.5 | 5.8 | 11.1 | 48.4 | 48.0 |

| 2013-14 | Bilateral/Multilateral | 23 | 30.0 | 4.9 | 13.0 | 47.8 | 50.6 |

| 2012-13 | Bilateral/Multilateral | 21 | 27.9 | 11.6 | 12.0 | 51.5 | 56.8 |

| 2011-12 | Bilateral/Multilateral | 9 | 22.1 | 5.7 | 12.0 | 44.0 | 47.3 |

| Weighted Average | 128 | 30.1 | 6.6 | 11.9 | 49.0 | 49.1 | |

| 2016** | Unilateral | 2 | 18.2 | -- | 5.2 | 23.3 | 23.3 |

| 2015-16 | Unilateral | 3 | 12.2 | -- | 2.9 | 15.1 | 15.4 |

| 2014-15 | Unilateral | 2 | 30.4 | -- | 40.4 | 70.8 | 70.8 |

| 2013-14 | Unilateral | 2 | 31.3 | -- | 14.9 | 46.2 | 46.2 |

| 2012-13 | Unilateral | 3 | 30.6 | -- | 5.3 | 35.9 | 26.8 |

| 2011-12 | Unilateral | 1 | 63.7 | -- | 26.8 | 90.5 | 90.5 |

| Weighted Average | 13 | 27.1 | 13.3 | 40.3 | 38.3 |

* For unilateral APAs, this column represents the time required to finalize an APA once a CRA transfer pricing position has been established.

** Statistics for 2016 calendar year. Going forward, the CRA will be reporting statistics on a calendar year basis.

Intercompany transactions

Intercompany transactions can broadly be classified into four categories: the transfer of tangible property; the transfer of rights associated with intangible property; intra-group services; and financing.

The majority of APAs continue to relate to the cross-border transfer of tangible property. At the close of the 2016 calendar year, 63% of APAs in process related to transfers of tangible property. Cases involving intangible property and intra-group services were the second most common type of transactions in the APA program, each representing 17% of all cases in process. Cases relating to financing accounted for 3% of all cases in process.

Table 3: APA program transaction type statistics (since program inception)

| Transaction type | Completed | % of total | In process | % of total | Combined | % of total |

|---|---|---|---|---|---|---|

| Tangible Property | 151 | 53% | 57 | 63% | 208 | 55% |

| Intangible Property | 70 | 24% | 15 | 17% | 85 | 23% |

| Intra-Group Services | 59 | 21% | 15 | 17% | 74 | 20% |

| Financing | 6 | 2% | 3 | 3% | 9 | 2% |

| Total | 286 | 100% | 90 | 100% | 376 | 100% |

Transfer pricing methodologies

The TNMM continues to be the predominant methodology employed in APAs – 69% of both completed and in process cases. At the end of the 2016 calendar year, the TNMM in conjunction with an operating margin profit level indicator (PLI) represented 56% of all cases currently in process in the APA program. The total cost plus, return on assets, and berry ratio profitability indicators are represented in 9%, 3% and 1% of all cases using the TNMM, respectively.

The profit split methodology, which is commonly utilized when intangible assets factor into the transfer pricing equation, is currently in use in 10% of APAs in process and in 12% of completed cases. The use of the profit split methodology in a significant number of cases reflects the CRA’s perspective that where both parties to the transaction are contributing to above normal profits (residual profits), a profit split will often provide a result that is more in keeping with the arm’s length principle. The profit split methodology is also often used when the operational characteristics of two non-arm’s length parties are highly integrated, making it difficult to clearly identify functions performed, risks undertaken and assets owned by each respective party. Additionally, where it is appropriate and possible, all covered transactions involving the licensing of intangible property are initially analysed utilizing the profit split methodology.

The cost plus, comparable uncontrolled price / transaction, and resale price methodologies were represented in 11%, 9%, and 1% of APAs currently in process at the close of the 2016 calendar year.

As an addition to the yearly report, the following section represents the correlation between industry and transfer pricing methodologies. In the 2016 calendar year, certain industrial sectors were analyzed compared to their most prominent transfer pricing methodology. The TNMM with an operating margin PLI is represented in several industrial sectors, including in 91% of the health sector cases, 71% of the computers and electronics sector cases, 63% of the automotive and other transportation sector cases, and 57% of the metals & minerals sector cases. The Cost/Cost Plus methodology is represented in 57% of the petroleum sector cases as depicted in the graphs below.

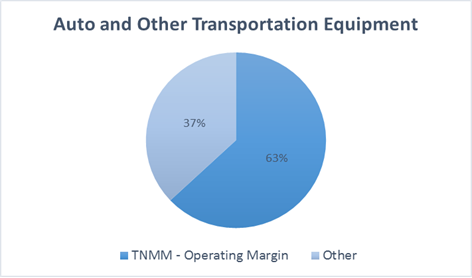

“Transfer Pricing Methodology used for cases within the auto and transportation equipment industry”

“In 2016, 63% of cases within the auto and transportation equipment industry used the Transactional Net Margin Method – Operating Margin methodology.”

“Whereas, 37% of cases within the auto and transportation equipment industry used other methodologies.”

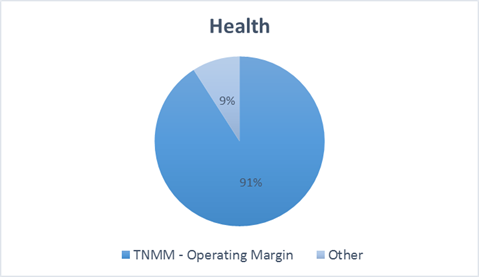

“Transfer Pricing Methodology used for cases within the health industry.”

“In 2016, 91% of cases within the health industry used the Transactional Net Margin Method – Operating Margin methodology.”

“Whereas, 9% of cases within the health industry used other methodologies.”

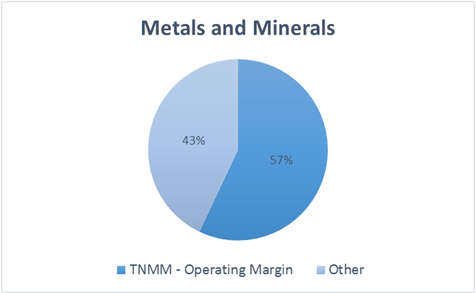

“Transfer Pricing Methodology used for cases within the metals and minerals industry."

“In 2016, 57% of cases within the metals and minerals industry used the Transactional Net Margin Method – Operating Margin methodology.”

“Whereas, 43% of cases within the metals and minerals industry used other methodologies. ”

“Transfer Pricing Methodology used for cases within the computers and electronics industry. ”

“In 2016, 71% of cases within the computers and electronic industry used the Transactional Net Margin Method – Operating Margin methodology.”

“Whereas, 29% of cases within the computers and electronics industry used other methodologies.”

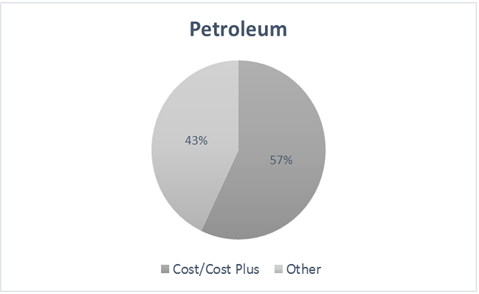

“Transfer Pricing Methodology used for cases within the petroleum industry"

“In 2016, 57% of cases within the petroleum industry used the cost/cost plus methodology.”

“Whereas, 43% of cases within the petroleum industry used other methodologies.”

It should be noted, that where an APA is still in process and the CRA has yet to finalize its position paper, the methodology reported is the methodology that is proposed by the taxpayer. Following the development of the CRA’s position, where an alternative methodology has been selected by the CRA, the alternative approach may be that which is reflected in the statistics. Additionally, statistics reported for the cost plus method include service transactions and cost sharing arrangements.

Table 4: APA program transfer pricing methodology statistics (since program inception)

| Transfer pricing methodology | Completed | % of total | In process | % of total | Combined | % of total |

|---|---|---|---|---|---|---|

| Comparable Uncontrolled Price / Transaction | 38 | 14% | 8 | 9% | 46 | 12% |

| Cost Plus | 41 | 15% | 10 | 11% | 51 | 14% |

| Resale Price | 19 | 7% | 1 | 1% | 20 | 5% |

| Transactional Net Margin Method (TNMM) - Total * | 136 | 46% | 62 | 69% | 198 | 53% |

| PLI - Berry Ratio | 10 | 4% | 1 | 1% | 11 | 3% |

| PLI - Operating Margin | 84 | 27% | 50 | 56% | 134 | 36% |

| PLI - Return on Assets | 6 | 2% | 3 | 3% | 9 | 2% |

| PLI - Total Cost Plus | 36 | 13% | 8 | 9% | 44 | 12% |

| Profit Split | 52 | 19% | 9 | 10% | 61 | 16% |

| Total * | 286 | 100% | 90 | 100% | 376 | 100% |

* Totals may not sum due to rounding.

Participation by industrial sector

Participation in the APA program by industrial sector generally reflects the pattern of Canadian trade. Cases involving taxpayers with operations residing within the automobile and other transportation equipment, health, computers and electronics, petroleum, and metals and minerals sectors represent over one-half of all in-process cases in the CRA’s APA program.

Since the inception of the APA program, there have been 87 cases related to the automobile and other transportation equipment sector, of which 19 are currently still in process. Cases with taxpayers operating in the realm of the computer and electronics sector have represented 43 cases in total, of which 7 are still in process.

Participation by country

Currently, the CRA is actively engaged in bilateral or multilateral APA processes involving taxpayers from 15 different countries. After the United States, these other countries are United Kingdom, Switzerland, South Korea, Japan, Germany, Netherlands, Ireland, Sweden, India, China, Portugal, Denmark, Chile, and Austria.

The breakdown of bilateral and multilateral APAs by country continues to reflect the significant flow of goods and services exchanged between Canada and the United States. Since the program’s inception, the CRA has completed 182 APAs (or 75%), of the 243 successfully concluded cases, involving the United States on a bilateral basis. At the close of the 2016 calendar year, there were 45 cases in process involving the United States. Currently, APAs involving the United States represent 56% of all APAs in process.

Participation by Canadian province

The distribution of APAs across Canada broadly reflects the allocation of Canadian corporate headquarters within the country. Taxpayers located in Ontario represent over one-half of all APAs currently in process totalling 58 cases or 65%. There are currently 10 cases, or 11%, involving taxpayers headquartered in the Province of Quebec. Representation from Western Canada (the Provinces of British Columbia, Alberta, Saskatchewan and Manitoba) totalled 20 APAs or 22% of cases. And finally, there are currently 2 cases or 2% of all in-process APAs involving taxpayers located in the Atlantic Provinces.

Closing remarks

Since its inception in 1990, the APA program has become a key compliance tool for the CRA while fostering a collaborative and cooperative relationship between taxpayers and other tax administrations. It has also shown that communication, transparency, and compromise permit the resolution of mutually agreeable solutions to complex transfer pricing issues on a proactive basis. The program provides an opportunity for taxpayers to openly discuss the challenges they face in attempting to comply with the tax laws of multiple jurisdictions. Prospective tax certainty provided through the program helps to reduce barriers to trade and contributes to the free flow of capital.

To ensure program efficiency, taxpayers are required to provide the pre-file package prior to being granted a pre-file meeting. This package should include significantly detailed information pertaining to financial statements, business operations, and industry. This information is generally similar to that which taxpayers have historically been asked to provide during later stages of the APA process.

The CRA is optimistic that increased rigor in the earliest phases of the APA process will further reduce the time required to complete bilateral APAs successfully with Canada’s tax treaty partners in future years. The CRA also believes that this focus will help ensure that only taxpayers that are willing to openly work with the CRA on a transparent basis will be permitted access to the APA program.

The changes, which were preliminarily introduced in fiscal year 2010-11, fully complement a series of program objectives aimed at expediting the rate at which it takes to successfully conclude an APA from acceptance into the program to a signed APA agreement. These objectives include establishing mutually agreed upon targets and timelines with our foreign tax administrative counterparts and the identification of priority cases. In this regard, the CRA is confident that over the course of the 2017 calendar year, the improved number of cases completed and completion times will be maintained.

How to contact us

If you have any comments or questions about this report or the services offered by the Competent Authority Services Division, contact us by telephone at 613-946-6081, send us a facsimile at 613-990-7370, email us at CP-PO_MAP_APA-PAA_APP@cra-arc.gc.ca, or write to us at the following address:

For delivery by mail and by courier:

Canada Revenue Agency

Director, Competent Authority Services Division

International and Large Business Directorate

International, Large Business and Investigations Branch

427 Laurier Ave W, 8th Floor

Ottawa ON K1A 0L5

Page details

2023-11-07