Subsection 156(1) - Definitions

Qualifying Group

See Also

9331-0688 Québec Inc. v. The King, 2023 TCC 173 (Informal Procedure)

In finding that three corporations which had the same individual as their sole shareholder did not qualify as specified members of a qualifying...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 128 - Subsection 128(1) | controlling shareholder of a corporate closely-related group must itself be a corporation | 35 |

Administrative Policy

12 February 2018 interpretation 167422R

In the original version of this Interpretation (see 167422), CRA found that, in the structure depicted immediately below (involving a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Qualifying Subsidiary | qualifying subsidiary definition can be applied iteratively | 63 |

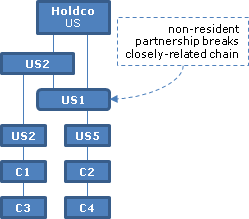

19 June 2015 Interpretation 167422

In a wholly-owned group, there are two stacks of four corporations beneath a common Holdco. The two bottom (Canadian) corporations will not be...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 128 - Subsection 128(2) | limitations on stacking | 328 |

4 February 2014 Interpretation 159039

{kind=link}

GST/HST Memorandum 14-5, Election to Deem Supplies to be Made for Nil Consideration, June 2023

Example 1

Where OpCo (a registrant substantially all of whose preoperty was acquired for use or supply exclusively in commercial activities)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 175.1 | 168 | |

| Tax Topics - Excise Tax Act - Section 272 | 182 |

Guide for Providers of Financial Services under "Special Provisions" - "Election for Nil Consideration for Closely Related Corporations"

General discussion.

Qualifying Member

Administrative Policy

27 February 2020 CBA Roundtable, Q.5

In CIBC World Markets, the Federal Court of Appeal found that a non-resident permanent establishment of CIBC had deemed separate person status...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 132 - Subsection 132(2) | s. 132(2) does not deem a non-resident person to be a resident | 159 |

26 February 2015 CBA Roundtable, Q.21

CRA indicated that s. 186(1) applied “only for the purpose of ITC calculations” and does not have the effect of deeming the holding company to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 186 - Subsection 186(1) | s. 186(1) does not help a parent to qualify for a s.156 election | 147 |

26 February 2015 CBA Roundtable, Q.22

Black’s Law Dictionary (9th ed.) defines "nominal" as "trifling, especially as compared to what would be expected (lamp sold for a nominal price...

24 April 2015 Interpretation 166609

In interpreting "property having a nominal value" in para. (c) of "qualifying member," should the value of the property be compared with the value...

14 January 2015 Interpretation 165076

In commenting on the "it is reasonable to expect" test in (c)(iii), CRA stated:

The CRA would generally review available documentation such as...

10 February 2014 Interpretation 154536

FinanceCo, which was a de minimis financial institution, held both equipment used in leasing and loans. In the course of a general discussion, CRA...

Subsection 156(1.1)

Paragraph 156(1.1)(a)

Subparagraph 156(1.1)(a)(i)

Clause 156(1.1)(a)(i)(C)

Administrative Policy

GST/HST Memorandum 14-8 Closely Related Canadian Partnerships and Corporations for Purposes of Section 156 June 2023

3 stacked Canadian partnerships, which thus form a closely related group, are closely related to a 4th Canadian partnership jointly owned by them

Paragraph 156(1.1)(b)

Administrative Policy

GST/HST Notice No. 303 - Changes to the Closely-related Test

The revised ETA closely-related person test requires that 90% or more of shareholder votes in respect of all corporate matters must be held and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 128 - Subsection 128(1.1) - Paragraph 128(1.1)(a) - Subparagraph 128(1.1)(a)(i) | exception for special voting matters provided by statute, or where a statute provides a special class vote | 286 |

| Tax Topics - Excise Tax Act - Section 150 - Subsection 150(2) - Paragraph 150(2)(b.1) | example of substantially all test not satisfied | 174 |

Subparagraph 156(1.1)(b)(iii)

Clause 156(1.1)(b)(iii)(C)

Administrative Policy

GST/HST Memorandum 14-8 Closely Related Canadian Partnerships and Corporations for Purposes of Section 156 June 2023

Where 2 grandchildren of AB Corp each hold a 50% partnership interest in XY, each corporation in that chain, as well as each corporation in...

Subsection 156(1.2)

Administrative Policy

GST/HST Memorandum 14-8 Closely Related Canadian Partnerships and Corporations for Purposes of Section 156 June 2023

By virtue of a qualifying group – consisting of a holding partnership (X) holding 90% of a partnership (Y) and 90% of a corporation (Z) – each...

Subsection 156(1.3)

Paragraph 156(1.3)(b)

Subparagraph 156(1.3)(b)(i)

Administrative Policy

GST/HST Memorandum 14-8 Closely Related Canadian Partnerships and Corporations for Purposes of Section 156 June 2023

S. 156(1.3)(b)(i) tests applied on a source-by-source basis

9. The income entitlement part [in s. 156(1.3)(b)(i)] recognizes the fact that a...

Subparagraph 156(1.3)(b)(iii)

Administrative Policy

GST/HST Memorandum 14-8 Closely Related Canadian Partnerships and Corporations for Purposes of Section 156 June 2023

Test in s. 156(1.3)(b)(iii) precludes a limited partner as such being closely related to the partnership

12. In a limited partnership, the limited...

Subsection 156(2) - Election for Nil Consideration

Administrative Policy

21 December 2017 Interpretation 164739

Although ETA s. 173(1) often imputes a taxable supply by an employer based on the amount of taxable benefits conferred by it under ITA s. 6(1)(a),...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 173 - Subsection 173(1) - Paragraph 173(1)(d) - Paragraph 173(1)(d) | no denial under s. 170 where employer acquisition "benefited" from s. 156 election: imputed s. 173 tax even though no ITC | 178 |

Excise and GST/HST News - No. 95 under "

//www.cra-arc.gc.ca/E/pbg/gf/rc4616/README.html">Form RC4616 – Simplified filing procedures concerning existing elections for nil consideration"...

Excise and GST/HST News - No. 94 14 January 2015

Effective January 1, 2015, an election (or revocation of an election) must be made jointly by a particular specified member of a qualifying group...

Excise and GST/HST News – No. 91 under "GST/HST election for closely related persons" May 2014

[E]ffective January 1, 2015, parties to a new election or revocation will be required to file Form RC4616, (replacing Form GST25…) with the...

91 CPTJ - Q.10

The election under s. 156 is not intended to apply to butterfly transactions. Because a newly-created corporation will usually only make exempt...

Subsection 156(2.01)

Articles

John Bassindale, Robert G. Kreklewetz, "Budget 2014: Changes for Section 156 and Closely Related Persons", Sales and Use Tax, Federated Press, Volume XII, No. 4, 2014, p. 659

Brief refiling deadline (pp. 659-660)

[E]xisting section 156 elections [must] be filed during the calendar year 2015 - a relatively brief one-year...

Subsection 156(3) - Cessation

Administrative Policy

29 January 2015 Interpretation 167061

In the course of a general discussion on completion, filing and revocation of form RC4616, CRA stated:

[Effect of disqualification]

[I]n the event...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 156 - Subsection 156(4) | one signing member/MyBA filing | 309 |

Subsection 156(4) - Form of Election and Revocation

Administrative Policy

May 2019 CPA Alberta CRA Roundtable, GST Session – Q.20

Closely related Company A and Company B (monthly filers) made an election under Company A's My Business account with an effective date of October...

26 February 2015 CBA Roundtable, Q. 15

Before responding to a question on backdated s. 273 elections, CRA did not demur when the questioner noted that CRA had indicated that a s. 156...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 273 - Subsection 273(4) | backdated election for valid JV permissible/co-ownership not co-terminous with JV | 198 |

29 January 2015 Interpretation 167061

In the course of a general discussion on completion and filing of form RC4616, CRA stated:

[Filing by one specified member]

[T]he first specified...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 156 - Subsection 156(3) | disqualification does not affect non-paired members/avoiding inadvertent revocation | 316 |

28 August 2000 Headquarters Letter Case 30915

"If the parties have conducted themselves as if an election were in place (and if the conditions for making the election are met at all relevant...

GST25 "Closely Related Corporations and Canadian Partnerships - Election or Revocation of the Election to Treat Certain Taxable Supplies as Having Been Made for Nil Consideration"

All or substantially all generally means 90% or more. ... You do not have to file this form with the Canada Revenue Agency.

Forms

Paragraph 156(4)(b)

Subparagraph 156(4)(b)(ii)

Cases

Castle Building Group Ltd. v. Canada (National Revenue), 2021 FC 947

The Applicants were Castle, a registrant which purchased building materials for resale, and was the exclusive supplier of building materials to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 171 - Subsection 171(1) | billing election did not subtract from the principal making taxable supplies and being a registrant | 346 |

Denso Manufacturing Canada Inc. v. Canada (National Revenue), 2020 FC 360, aff'd 2021 FCA 236

Following the commencement of an audit in November 2015, in February 2016 a CRA auditor asked the applicant (Denso Manufacturing), which was...

Administrative Policy

May 2019 CPA Alberta CRA Roundtable, GST Session – Q.4

Respecting a query on late-filed ETA s. 156 elections, CRA stated:

Under administrative tolerance, the CRA may consider a request to accept a...

May 2017 Alberta CPA Roundtable, GST/HST Q.5

When will CRA will accept a late-filed s. 156 election (form RC4616)? CRA responded:

CRA normally accepts these when the registrant is eligible,...

23 March 2017 CBA Commodity Taxes Roundtable, Q.11

How can registrants obtain permission pursuant to s. 156(4)(b)(ii) to file an election after the dates in s. 156(4)(b)(i) have passed? CRA...

GST/HST Policy Statement P-255 Late-filed Section 156 Elections and Revocations July 2015

A request to accept a late-filed section 156 election or revocation of the election will be considered...within the context of the following...