NexPoint

Overview

Nexpoint Hospitality Trust (the “REIT”) is proposing to use the proceeds of an IPO to invest in 11 U.S. hotels. An affiliate of its...

BSR REIT

Overview

A closely-held Delaware LLC with a portfolio of apartment buildings in the southern U.S. appraised at U.S.$890M (“BSR”) is proposing...

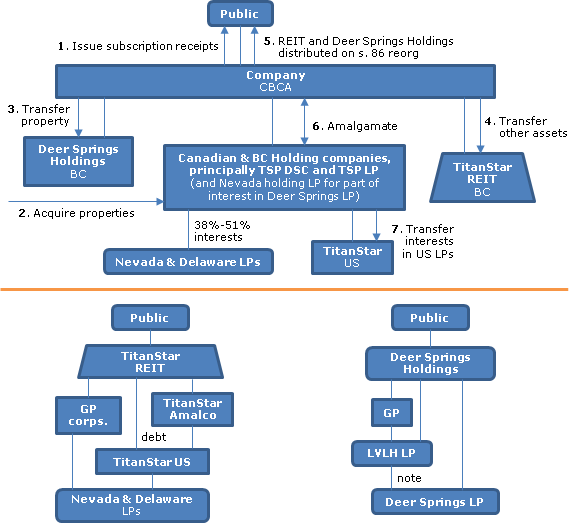

TitanStar

{kind=link}

WPT

Overview

Through an indirectly owned Delaware LP (the "Partnership"), the REIT (an Ontario unit trust) will acquire a portfolio of 37 warehouse...

Inovalis

Overview

The REIT, which is an Ontario unit trust, is offering 10.5M units for $105M. It will acquire four leasehold interests in French and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Public Transactions - Other - DRIPs - Bonus Unit Plans | Inovalis Real Estate Investment Trust unit offering: investment in French and German office properties using headlease and option structure | 84 |

Milestone Apartments

Overview

Offering of 20 million REIT units ($200 million). Through an indirectly owned Delaware LP (the "Partnership"), the REIT will acquire a...

Agellan

Overview of structure

The REIT will invest directly or indirectly in a mix of Canadian and US industrial and commercial (plus one retail) rental...

Northwest Healthcare

Offering

Of units of the REIT, which is TSXV-listed, at $2.00 per unit for gross proceeds of $25M ($28.75M if over-allotment).

Current...

Granite

Structure

Granite REIT, a TSX and NYSE listed Canadian mutual fund trust governed by Ontario law, will be the 99.999% limited partner of a Quebec...

Timbercreek

Structure

The Fund subscription proceeds described below are used by the Fund to subscribe for a general partner interest in a subsidiary general...

Healthlease

Overview of structure

A TSX-listed REIT (HealthLease REIT) will hold a portfolio of seniors care facilities in the case of the western Canadian...

Pure Multi-Family

An Ontario LP ("REIT LP") that will trade on the TSX Venture Exchange invests in a Maryland corporation (holding US apartment buildings) that...