Brochure - Doing taxes for someone who died

Disclaimer

We do not guarantee the accuracy of this copy of the CRA website.

Scraped Page Content

Brochure: Doing taxes for someone who died

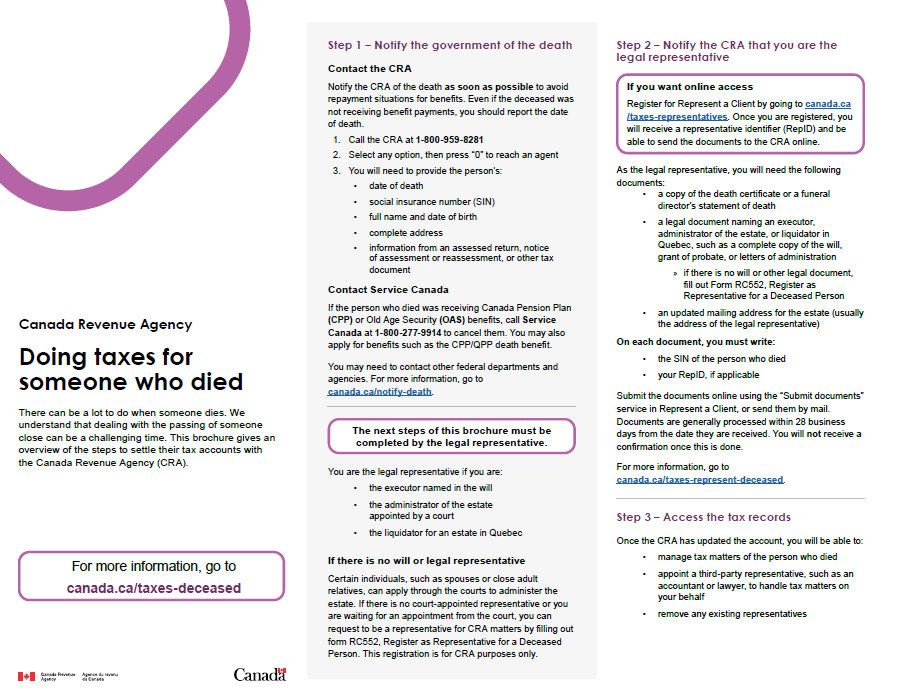

There can be a lot to do when someone dies. We understand that dealing with the passing of someone close can be a challenging time. This brochure gives an overview of the steps to settle their tax accounts with the Canada Revenue Agency (CRA).

Brochure description

- Step 1 – Notify the government of the death

Contact the CRA

Notify the CRA of the death as soon as possible to avoid repayment situations for benefits. Even if the deceased was not receiving benefit payments, you should report the date of death.

- Call the CRA at 1-800-959-8281

- Select any option, then press “0” to reach an agent

- You will need to provide the person’s:

- date of death

- social insurance number (SIN)

- full name and date of birth

- complete address

- information from an assessed return, notice of assessment or reassessment, or other tax document

Contact Service Canada

If the person who died was receiving Canada Pension Plan (CPP) or Old Age Security (OAS) benefits, call Service Canada at 1-800-277-9914 to cancel them. You may also apply for benefits such as the CPP/QPP death benefit.

You may need to contact other federal departments and agencies. For more information, go to canada.ca/notify-death.

The next steps of this brochure must be completed by the legal representative.

You are the legal representative if you are:

- the executor named in the will

- the administrator of the estate appointed by a court

- the liquidator for an estate in Quebec

If there is no will or legal representative

Certain individuals, such as spouses or close adult relatives, can apply through the courts to administer the estate. If there is no court-appointed representative or you are waiting for an appointment from the court, you can request to be a representative for CRA matters by filling out form RC552, Register as Representative for a Deceased Person. This registration is for CRA purposes only.

- Step 2 – Notify the CRA that you are the legal representative

If you want online access

Register for Represent a Client by going to canada.ca/taxes-representatives. Once you are registered, you will receive a representative identifier (RepID) and be able to send the documents to the CRA online.

As the legal representative, you will need the following documents:

- a copy of the death certificate or a funeral director’s statement of death

- a legal document naming an executor, administrator of the estate, or liquidator in Quebec, such as a complete copy of the will, grant of probate, or letters of administration

- if there is no will or other legal document, fill out Form RC552, Register as Representative for a Deceased Person

- an updated mailing address for the estate (usually the address of the legal representative)

On each document, you must write:

- the SIN of the person who died

- your RepID, if applicable

Submit the documents online using the “Submit documents” service in Represent a Client, or send them by mail. Documents are generally processed within 28 business days from the date they are received. You will not receive a confirmation once this is done. For more information, go to canada.ca/taxes-represent-deceased.

- Step 3 – Access the tax records

Once the CRA has updated the account, you will be able to:

- manage tax matters of the person who died

- appoint a third-party representative, such as an accountant or lawyer, to handle tax matters on your behalf

- remove any existing representatives

- Step 4 – File the final Return

You must file a final T1 Income Tax and Benefit Return, called the Final Return, for the person who died.

The Final Return is used to report any income from property, investments and belongings up until the date of death. You can also claim any eligible deductions and credits.

To get started, you will need to determine the deceased person’s income from all sources.

- Check previous-year tax returns for the names of employers and investment companies

- Check safety deposit boxes for more sources of income and benefits

- Contact payers such as employers, financial institutions, and pension plan managers

- Get information slips such as a T4 from an employer or a T5 from a bank

- Contact Service Canada at 1-800-622-6232 if the deceased was receiving:

- CPP benefits and you do not have a T4A(P) slip

- OAS pension and you do not have a T4(OAS) slip

You must also ensure that the person who died filed tax returns for all previous years and file any outstanding returns.

For more information, including due dates, go to canada.ca/prepare-tax-returns-deceased.

- Step 5 – File any optional T1 returns (if applicable)

If the person who died had eligible income, you can also file other optional T1 returns.

You do not need to file any of the optional T1 returns, but doing so may reduce or eliminate tax for the person who died.

This is possible because you can claim certain deductions or credits more than once, split them between returns, or claim them against specific kinds of income.

For more information, including due dates, go to canada.ca/prepare-tax-returns-deceased.

- Step 6 – File a T3 Trust Return (if applicable)

When someone dies, their belongings, property, assets and liabilities form their estate.

An estate may continue to earn income such as investment income or receive amounts such as a death benefit.

If the estate earns income after death or distributes property to beneficiaries, you may need to file a T3 Trust Income Tax and Information Return.

Note: If the CPP/QPP death benefit amount is the only income of the estate, and a T3 Return is not otherwise required to be filed, the beneficiary of the estate can report the amount directly on their T1 Return for the year the amount was received.

For more information, including due dates, go to canada.ca/prepare-tax-returns-deceased.

- Step 7 – Before distributing the assets

Before distributing the deceased person’s assets, you must get a clearance certificate. A clearance certificate certifies that all amounts owed to the CRA have been paid.

If the assets are distributed before obtaining a clearance certificate and amounts are owing to the CRA, the legal representative is personally liable for the debt, up to the value of the assets distributed.

Apply for a clearance certificate after:

- all required tax returns have been filed

- you have received the notices of assessment for the returns

- any amounts owing have been paid or secured

- there are no outstanding adjustment requests, objections, taxpayer relief, or appeals requests

For more information, go to canada.ca/clearance-certificate.

- Additional information

Residents of Quebec

If the person who died was a resident of Quebec, there are more steps to complete with Revenu Québec.

For more information, go to revenuquebec.ca and search for “liquidators of a succession”.

Mailing instructions

Send any documents or forms to the deceased person’s tax centre.

For mailing addresses, go to canada.ca/cra-offices.

If you need help or more information

Go to canada.ca/taxes-deceased

Call 1-800-959-8281 and select the option for “Estates and Trusts”

Page details

2025-01-21