Cases

4431472 Canada Inc. v. Canada (Attorney General), 2021 FC 812

A Canadian corporation (“443 Inc”) filed its tax returns on the basis that distributions received by it from a trust were distributions of fee...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 164 - Subsection 164(1) | reversal of CRA decision not to reassess on the basis that it was unclear whether it was a final decision | 585 |

Ludmer v. Attorney General of Canada, 2018 QCCS 3381, aff'd 2020 QCCA 697

Two of the taxpayers (“Ludmer” and Steinberg”) were invested along with family, friends and acquaintances (all resident in Canada) in a BVI...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4) - Paragraph 152(4)(a) - Subparagraph 152(4)(a)(i) | nature of the legal advice relied upon was unclear | 417 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(1) | improper advancing of “settlement” elements that were not sustainable | 45 |

| Tax Topics - Income Tax Act - Section 94.1 - Subsection 94.1(1) | equity-linked notes held in BVI company were portfolio investments held with a tax avoidance purpose, but were not subject to 7000(2)(d) interest accrual | 576 |

| Tax Topics - Income Tax Regulations - Regulation 7000 - Subsection 7000(2) - Paragraph 7000(2)(d) | mere possibility of locking in value accretion each year did not crystallize the maximum amount of interest respecting the year | 484 |

| Tax Topics - General Concepts - Negligence, Fiduciary Duty and Fault | damages awarded against CRA for inter alia making unreasonable reassessments | 260 |

| Tax Topics - Income Tax Act - Section 3 - Paragraph 3(a) - Business Source/Reasonable Expectation of Profit | recurring fee reduction amounts received for no work were income from a source | 313 |

Lambert v. Canada, 2005 DTC 5499, 2004 FCA 389

A taxable benefit was earned by the taxpayer when a corporation partly owned by him funded the costs of installing a new engine in an aircraft of...

James v. Canada, 2001 DTC 5075 (FCA)

Amounts that had been earned for work done by the taxpayer (James) for a corporation ("K.C.R. Investments") and that were paid by K.C.R....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Audit, Filing and Assessment Procedure | 101 | |

| Tax Topics - General Concepts - Evidence | 54 | |

| Tax Topics - Income Tax Act - Section 165 - Subsection 165(3) | vacating not a remedy for lack of due dispatch | 86 |

Neuman v. M.N.R., 98 DTC 6297, [1998] 1 S.C.R. 770, [1998] 3 CTC 177

The taxpayer transferred his shares of a commercial real estate company to a newly-incorporated company ("Melru") in consideration for 1,285.714...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Provincial Law | 55 |

Jones v. The Queen, 96 DTC 6016 (FCA)

The sale of a property by a corporation ("Ascot") owned by the taxpayer to the taxpayer's father for less than the property's fair market value...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Resolving Ambiguity | 77 |

Smith v. The Queen, 93 DTC 5351, [1993] 2 CTC 257 (FCA)

At a time that the taxpayer was an officer, director, and 49% shareholder of an incorporated Ford dealership ("Holiday 77"), Holiday 77...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(2) - Paragraph 40(2)(g) - Subparagraph 40(2)(g)(ii) | 39 |

Dixon v. Deputy Attorney General of Canada, 91 DTC 5584 (Ont HCJ.)

An allegation of the Crown that a corporation had knowingly sold land at a substantial undervalue to a corporation half-owned by its president, if...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Solicitor-Client Privilege | 160 | |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | common directing mind | 77 |

The Queen v. Fairey, 91 DTC 5230 (FCTD)

The taxpayer's employer, the Cancer Control Agency of British Columbia, was required by statute to deduct an amount from the taxpayer's monthly...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 5 - Subsection 5(1) | 72 |

Mcclurg v. Canada, 91 DTC 5001, [1990] 3 S.C.R. 1020

Mr. McClurg and Mr. Ellis each owned 400 voting and participating Class A shares and 37,500 Class C non-voting preference shares in a trucking...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Resolving Ambiguity | 66 |

Winter v. The Queen, 90 DTC 6681, [1991] 1 CTC 113 (FCA)

An individual ("Outerbridge") had a company controlled by him ("Littlefield") sell shares of another corporation ("Harvey") to his son-in-law for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | s. 56(2) applied to taxpayer rather than 15(1) to son-in-law as de minimis shareholder | 74 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(2) | specific provisions applied before GAAR | 104 |

R. v. Century 21 Ramos Realty Inc., 87 DTC 5158, [1987] 1 CTC 340 (Ont.C.A.)

S.56(2) applied when a mortgage owing to a company owned by the individual accused ("Ramos") was discharged and replaced by a mortgage owing to a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Other Legislation/Constitution - Charter (Constitution Act, 1982) - Subsection 15(1) | 47 | |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | benefit based on actual rather than subjective value | 93 |

Boardman v. The Queen, 85 DTC 5628, [1986] 1 CTC 103 (FCTD)

The Saskatchewan Court of Queen's Bench pursuant to s. 22 of the Married Women's Property Act (Sask.) directed the Registrar of Land Titles to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | 69 | |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(4) | 34 |

The Queen v. Hoffman, 85 DTC 5508, [1985] 2 CTC 347 (FCTD)

The defendant's Canadian employer deducted amounts from his salary and remitted them to its U.S. parent pursuant to an agreement between the...

De Groote v. The Queen, 85 DTC 5008, [1984] CTC 687 (FCTD)

S.56(2) did not apply to a payment of dividends since the payor corporation, instead of paying the dividends to the beneficial owner of shares...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(4) | 94 | |

| Tax Topics - Income Tax Act - Section 82 - Subsection 82(1) - Paragraph 82(1)(a) | no longer beneficial shareholder | 76 |

The Queen v. Chrapko, 84 DTC 6544, [1984] CTC 594 (FCTD), rev'd 88 DTC 6487, [1988] 2 CTC 342 (FCA)

The Ontario Jockey Club deducted from each pay cheque that it paid to a race track cashier the amount of cash shortages due to errors made by him....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Other Legislation/Constitution - Federal - Federal Courts Rules - Rule 420 [Amendment of Pleadings] | 38 | |

| Tax Topics - Income Tax Act - Section 67 | 71 |

Barbeau v. The Queen, 84 DTC 6148, [1981] CTC 496, [1981] DTC 5379 (FCTD)

Commissions paid by a company to a "technical and financial advis[ory]" company owned by the taxpayer's family were taxable to him. The...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 177 - Subparagraph 177(b)(iv) | 87 |

Champ v. The Queen, 83 DTC 5029, [1983] CTC 1 (FCTD)

The Class "A" voting shares of a company, which shares were owned by the taxpayer, had the same rights attached to them as the Class "B" voting...

Cox v. The Queen, 82 DTC 6287, [1982] CTC 322 (FCTD)

Where executors of an estate conveyed land to the taxpayer and his wife jointly in satisfaction of a quantum meruit claim which the taxpayer had...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Compensation Payments | 86 |

Fraser Companies, Ltd. v. The Queen, 81 DTC 5051, [1981] CTC 61 (FCTD)

Substantial interest-free loans were made by a New Brunswick pulp company to a subsidiary that was exempt from taxation by virtue of its status as...

Murphy v. The Queen, 80 DTC 6314, [1980] CTC 386 (FCTD)

S.56(2), unlike S.74(1) does not refer to property being transferred "either directly or indirectly by means of a trust or by any other means...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Property | included right to be included in class of discretionary beneficiaries | 46 |

| Tax Topics - Income Tax Act - Section 74.1 - Subsection 74.1(1) | 95 |

McClain Industries of Canada Inc. v. The Queen, 78 DTC 6356, [1978] CTC 511 (FCTD)

When the vendor shareholders of a company agreed to assign unpaid accrued management commissions to the purchaser, the amounts of the commissions...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(e) | 99 |

Perrault v. The Queen, 78 DTC 6272, [1978] CTC 395 (FCA)

It was indicated, obiter, that it was doubtful that s. 56(2) could be applied to the payment of a dividend which was included in the income of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | dividend satisfied share purchase consideration | 114 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | a single payment can result in income inclusions to 2 taxpayers - the 2nd as a taxable benefit | 91 |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | business continued "on a reduced scale" | 54 |

Nelson v. The Queen, 74 DTC 6266, [1974] CTC 360 (FCA)

Although it was the intention of the four related shareholders of a company that father hold 100 voting participating shares and each of his three...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | 187 |

The Queen v. Quinn, 73 DTC 5215, [1973] CTC 258 (FCTD)

Under a contract with the Canadian Scholarship Trust Fund it was agreed that interest on funds deposited by the taxpayer would be transferred to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(c) | 87 | |

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | 96 |

See Also

Bolduc v. Agence du revenu du Québec, 2025 QCCA 1470

A limited partnership (“SEC”) sold condo units for less than their fair market value to the daughter and wife of Mr. Migliara, the founder of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(b) | deemed FMV proceeds on sale by partnership of condos at an undervalue to individuals related to partners | 131 |

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | s. 246(1) equivalent applied to a benefit conferred by a partnership on the shareholder of a limited partner or of a business contractor | 183 |

Tremblay v. Agence du revenu du Québec, 2025 QCCA 783

The taxpayer (Tremblay) separated from his spouse (Francoeur) in 2011, and they divorced in 2016.

In 2013, in connection with their separation,...

Fournier v. Agence du revenu du Québec, 2018 QCCQ 786

The ARQ assessed the taxpayer and his wife for taxable benefits for a period of approximately 2 ½ years on the alleged basis that during that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Rectification & Rescission | taxpayer could reverse an assessment for a taxable benefit by subsequently engaging in self-help rectification | 390 |

Gainor v. The Queen, 2011 DTC 1317 [at at 1798], 2011 TCC 442

The taxpayer had been a director of corporation ("Canam") which had been struck from the corporate registry. Unaware of Canam's dissolution, CIBC...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Nature of Income | 172 |

Delso Restoration Ltd. v. The Queen, 2011 DTC 1315 [at at 1786], 2011 TCC 435 (Informal Procedure)

The corporate taxpayer was held entirely by the two individual taxpayers, who were alleged by the Minister to have had it pay for renovations on...

D'Andrea v. The Queen, 2011 DTC 1234 [at at 1356], 2011 TCC 298

The taxpayer was a manager of a corporation, which held real estate. He arranged to sell the property to a corporation ("Newco") that was owned...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4) - Paragraph 152(4)(a) - Subparagraph 152(4)(a)(i) | fraud conviction did not establish neglectful reporting | 193 |

Sochatsky v. The Queen, 2011 DTC 1065 [at at 346], 2011 TCC 41, 2012 TCC 65

The taxpayer was a director, shareholder and employee of a corporation. He resigned from his directorship and employment in 2001. In that year,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Payment & Receipt | bonus booked as loan back/constructive receipt | 131 |

| Tax Topics - Income Tax Act - Section 5 - Subsection 5(1) | amount booked as loaned-back bonus was remuneration | 186 |

GlaxoSmithKline Inc. v. The Queen, 2008 DTC 3957, 2008 TCC 324

The taxpayer purchased the active pharmaceutical ingredient of a drug that was marketed by it in Canada from an affiliated non-resident...

Laflamme v. The Queen, 2008 DTC 482, 2008 TCC 255

In the context of estate freeze transactions, a trust that the taxpayer had established for the benefit of his children transferred a portion of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Shares | 202 |

Ceco Operations Ltd. v. The Queen, 2006 DTC 3006, 2006 TCC 256

The taxpayer transferred assets of a business to a partnership in what was intended to be an s. 97(2) rollover transactions in consideration for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Substance | 99 | |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 270 | |

| Tax Topics - Income Tax Act - Section 97 - Subsection 97(2) | partnership subscription for taxpayer affiliate pref shares not boot | 263 |

Speer v. The Queen, 99 DTC 157 (TCC)

S.56(2) did not apply to an arrangement under which fees earned by companies as a result of a tax plan concocted by tax partners at Coopers &...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 129 - Subsection 129(1.2) | 37 |

Ferrel v. R., 97 DTC 1565, [1998] 1 CTC 2269 (TCC)

The taxpayer was the sole trustee of the family trust that, by utilizing his services, provided management services to corporations in which the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(4) | 65 |

Gilvesy v. The Queen, 96 DTC 1417, [1996] 3 CTC 2056 (TCC)

After facing bank pressure to have a corporation owned by him ("Enterprises") sell a property, the taxpayer arranged to have Enterprises sell the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Other | 53 |

Paxton v. The Queen, 95 DTC 179 (TCC), rev'd 97 DTC 5012 (FCA)

S.56(2) did not apply to transactions whereby the taxpayer, after agreeing with a third party to transfer his shares, or cause his shares to be...

Placements T.S. Inc. v. The Queen, 94 DTC 1302, [1994] 1 CTC 2464 (TCC)

A property over which the taxpayer had a right of first refusal was purchased for $500,000 from the arm's length owner by companies with whom the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4.01) | 110 | |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(4) | 126 |

Pierre Béliveau v. Minister of National Revenue, 91 DTC 669, [1991] 1 CTC 2683 (TCC)

When a corporation in which the taxpayer and his brother each had a 25% shareholding ("Brasserie") had its operating permit cancelled by the local...

Simon-Carves of Canada Ltd. v. MNR, 89 DTC 98, [1989] 1 CTC 2149 (TCC)

The direction by the U.K. shareholder of the taxpayer to pay off the liabilities of a U.S. affiliate of such shareholder gave rise to Part XIII...

Administrative Policy

21 June 2023 Internal T.I. 2017-0720181I7 - Application of 15(2) and 215(6)

Canco was assessed for and paid Part XIII tax regarding royalty payments that it made to its non-resident parent (Parentco) and to a non-resident...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 214 - Subsection 214(3) - Paragraph 214(3)(a) | no application of s. 214(3)(a) to Canco's conferral of a benefit on a non-resident sister by bearing the Part XIII tax on a royalty paid to it | 250 |

7 November 2022 External T.I. 2022-0926091E5 - Transfer of UK DB pension benefits to a UK SIPP

After a UK resident (under age 55) became resident in Canada, the commuted value of the individual’s member benefits under a UK defined-benefit...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(1) - Paragraph 56(1)(a) - Subparagraph 56(1)(a)(i) | constructive receipt where commuted value of entitlements under a UK defined-benefit plan transferred directly to a UK self-invested personal pension plan | 346 |

| Tax Topics - Income Tax Act - Section 94 - Subsection 94(1) - Contribution | direct transfer from one group UK pension plan to an individual UK pension plan constituted a contribution by the individual to the latter | 194 |

| Tax Topics - General Concepts - Payment & Receipt | constructive receipt doctrine applied to direct payment from one UK pension plan to UK individual pension plan | 106 |

1 June 2021 External T.I. 2020-0865201E5 F - Sale of property for POD less than FMV

Messrs. X and Y (unrelated individuals), who each wholly-owned operating corporations ("ACo" and "BCo"), also equally owned XYZCo, which built 12...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | sale of 2 properties by 50-50 corp at a knowing undervalue to the respective shareholders’ own corporations likely was non-arm’s length | 212 |

8 June 2018 Internal T.I. 2017-0683021I7 - Assignment of capital interest in a trust

As a discretionary irrevocable personal family trust, which had non-resident beneficiaries (Y and Y’s spouse (Z)), was approaching the 21-year...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(13) | purported drop-down of trust interests to an excluded beneficiary resulted in s. 104(13) inclusions to transferors | 343 |

| Tax Topics - Income Tax Act - Section 107 - Subsection 107(5) | purported drop down of trust interests by non-resident beneficiaries to ULC was ineffective so that s. 107(2.1) applied to subsequent purported asset distribution to ULC | 192 |

| Tax Topics - Income Tax Act - Section 105 - Subsection 105(1) | potential application of s. 105(1) to income distribution to non-qualifying transferee of trust interest | 273 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(25) - Paragraph 248(25)(a) | para. (a) refers to beneficiary in ordinary sense - and does not include assignee | 62 |

28 October 2016 External T.I. 2016-0654331E5 F - Transfer of rights to income

Upon a sale by A of leased land to a non-arm’s length corporation (Corporation A) in which A did not hold any shares, A and Corporation A...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Nature of Income | where rental lands purchased subject to obligation to pay the rents to vendor, rents did not have quality of income to purchaser under s. 9 | 165 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Incurring of Expense | where rental lands purchased subject to obligation to pay the rents to vendor, no income inclusion and deduction of the rents by the purchaser under ss. 9 and 18(1)(a) | 89 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(4) | where rental lands purchased subject to obligation to pay the rents to NAL vendor, s. 56(4) trumps s. 9 to include rents in purchaser’s income | 169 |

6 December 2016 External T.I. 2016-0666841E5 F - Sale of property for POD less than FMV

Opco’s shares are held as to 40%, 40% and 20% by Holdco A, Holdco B and Holdco C, which are wholly owned by three individual shareholders (A, B...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1.4) - Paragraph 15(1.4)(c) | application to Holdco shareholder of Opco where Opco conferrred a benefit on child of Holdco's shareholder | 210 |

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | s. 246(1) applicable to indirect shareholder benefit if direct shareholder influenced the benefit conferral | 205 |

14 March 2016 External T.I. 2016-0626781E5 - Neuman Type Situation

The only issued and outstanding share of Opco (which has retained earnings of $500,000) is 1 Class A common share, with a fair market value of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | s. 15(1) might apply where spouse subscribes nominal consideration for Opco shares and receives a large discretionary dividend | 226 |

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | Kieboom treated as entailing disposition of right to receive dividends | 340 |

| Tax Topics - Income Tax Act - Section 73 - Subsection 73(1) | spousal rollover for Kieboom disposition of economic interest | 82 |

24 June 2015 External T.I. 2015-0575911E5 F - Benefit to shareholder or conferred on a person

Corporation A, is wholly owned by Holdco, which has equal unrelated Shareholders 1, 2, 3 and 4. Corporation A disposes of a capital property to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1.4) - Paragraph 15(1.4)(c) | benefit only conferred on one shareholder (the husband) if wife of one of four sibling shareholders receives benefit | 333 |

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | benefit conferred on spouse of individual shareholder of parent | 153 |

S2-F3-C1 - Payments from Employer to Employee

1.8 A payment from an employer that is deemed [by s. 6(3)] to be employment income is included in an employee's income…[when] the amount is...

10 April 2014 External T.I. 2013-0514321E5 - Donated vacation

Employees, who are otherwise entitled to convert their vacation leave to cash, may donate a portion of their annual vacation entitlements for use...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(a) | donated vacation/no double taxation | 170 |

13 March 2014 External T.I. 2013-0510791E5 - Non-cash long-service award and cash donation

Will an employee realize a taxable benefit upon foregoing the receipt of a non-cash gift valued over $500 in recognition of long service and...

11 March 2014 Internal T.I. 2013-0513221I7 F - Stock options

Publico determined to grant stock options to its directors and consultants, as a result of which a private corporation ("Corporation") was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | double income inclusion under s. 56(2) or (4) to consulting corporation, and under s. 15(1) to its shareholder, where consultant's options issued directly by client to shareholder | 113 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(4) | implicit transfer by corporation when stock options earned by it were issued directly by its client to its shareholder | 175 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | s. 248(28) does not prevent a double income inclusion to corporation under s. 56 and shareholder under s. 15 | 226 |

| Tax Topics - Income Tax Act - Section 9 - Timing | no s. 9(1) income inclusion from consultant being granted stock options until exercise | 226 |

| Tax Topics - General Concepts - Fair Market Value - Options | stock options with no in-the-money value could have nil FMV | 134 |

| Tax Topics - Income Tax Act - Section 52 - Subsection 52(1) | s. 15 benefit due to shareholder receipt of stock options earned by corporation added to the ACB of the exercised shares | 165 |

27 February 2014 External T.I. 2013-0506401E5 - Loan from a partnership to an individual

{kind=link}

A partnership between Holdco1 as the 99.9% LP and Holdco2 as the 0.1% GP (owned by an arm's length individual) makes a $2 million...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2) | partnership to partner shareholder loan | 89 |

15 November 2013 Internal T.I. 2013-0478621I7 F - Transfer of intangibles - TP adjustments

Pursuant to a sales agreement between Canco, its immediate non-resident parent (Parent) and the ultimate U.S. parent of Canco (Pubco), as vendors,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) | group sale with Canco not charging for intangibles should engage s. 247(2) | 149 |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(4) | s. 69(4) inapplicable where grandchild Canco undercharges for asset sale, enhancing sales proceeds received by ultimate U.S. parent | 176 |

19 August 2013 External T.I. 2013-0488011E5 - Real Estate Referral Fees

If a real estate agent directed the real estate brokerage to pay a portion of the commission to the home purchaser as a referral fee, how would...

14 February 2013 Internal T.I. 2011-0424341I7 F - Amounts forwarded to trustee/beneficiary

The financial advisor of Mother settled a discretionary trust of which Mother and her friend (Y) were the trustees (with decisions to be made...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | s. 75(2) not applicable to dividends on common shares issued to discretionary family trust on estate freeze | 237 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(13) | income was received by children beneficiaries as agent for their mother | 263 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(6) - Paragraph 104(6)(b) | Quebec discretionary trust with two named trustees but, in fact, only one trustee, would not be entitled to s. 104(6)(b) deductions | 155 |

9 January 2013 External T.I. 2010-0384221E5 F - Paiements indirects

In finding that where a company was required under a collective agreement respecting self-employed workers which required it to pay certain fees...

6 December 2012 External T.I. 2012-0461711E5 F - Paiements indirects / Indirect payments

A producer who retains the services of an incorporated performing artist is required to pay a percentage of the fees otherwise payable by it to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 200 - Subsection 200(1) | no T4A slip to be issued by producer paying mandatory contributions to the fund for the union of the artist whose corporation receives fees from the producer | 197 |

30 October 2012 Ontario CTF Roundtable, 2012-0462891C6 - Application of 56(2) to discretionary trust

In response to a query as to whether, in the context of a fully discretionary trust where the sole trustee is also a discretionary beneficiary of...

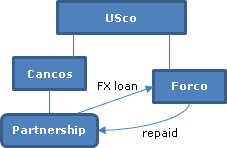

20 November 2012 Internal T.I. 2011-0416761I7 - Non-Resident, Part XIII Tax

{kind=link}

Although the facts are unclear, a possible approximation is that a partnership with Canadian partners, of which USco was the controlling...

25 September 2012 BC Tax Conference Roundtable, 2012-0457551C6 - Application of 56(2) to discretionary trust

CRA concluded that it could not "confirm, as requested, that subsection 56(2) will not apply in every case where the sole trustee (who is also a...

Income Tax Technical News, No. 16, 8 March 1999

RC now accepts that s. 56(2) "does not apply in the Neuman-type situations" and, further, has concluded that GAAR would not apply.

14 April 2009 External T.I. 2007-0238221E5 F - Rights of musician-Transfer

As part of a general response respecting the transfer of rights by a musician to a corporation, CRA stated:

As illustrated by … IT-335R2 [para....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(4) | s. 56(4) generally will apply where royalty is transferred without assignment of copyright, with exception of SOCAN royalty | 165 |

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1.1) | right to royalties from SOCAN constituted eligible property | 109 |

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Specified Investment Business | royalty income generated from an active business is itself active business income | 122 |

16 December 2008 External T.I. 2008-0279741E5 F - Renonciation au capital d'une fiducie

CRA indicated that the renunciation of a capital interest in a discretionary family trust would not give rise to the application of s. 56(2),...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | settlor’s valid renunciation of capital interest (but not income interest) prior to trustees’ exercise of discretion to distribute a capital gain would avoid application of s. 75(2)(a)(i) | 199 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(9) - Disclaimer | legally impossible for a beneficiary of a discretionary trust to partially renounce income from a specific trust property | 262 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition - Paragraph (i) | non-disposition distribution of non-taxable portion of trust capital gains avoids a gain under s. 107(2.1) | 375 |

| Tax Topics - Income Tax Act - Section 54 - Proceeds of Disposition | settlor’s renunciation of capital interest (but not income interest) prior to trustees’ exercise of discretion to distribute a capital gain would generate nil proceeds and not engage s. 56(2) or (4) | 194 |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(b) | s. 69(1) does not apply to a renunciation of trust capital interest since no disposition "to" any person | 44 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(4) | s. 56(4) inapplicable to disclaimer of capital interest in a trust | 43 |

4 January 2006 Internal T.I. 2005-0115801I7 F - Convention de retraite

A closely-held corporation that was dividending out all the profits of its business also established a purported retirement compensation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Retirement Compensation Arrangement | arrangement was not an RCA because the benefits were not reasonable | 110 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(r) | excessive benefits would have resulted in denial under ss. 18(1)(o.2) and 20(1)(r) had the arrangement qualified as an RCA | 206 |

| Tax Topics - Income Tax Act - Section 67 | Petro-Canada applied re determining reasonableness | 264 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Salary Deferral Arrangement | contributions to a purported RCA that contemplated excessive benefits also were not in relation to an SDA because the contributions instead were indirect shareholder appropriations | 108 |

11 March 2003 External T.I. 2002-0179095 F - Issuance-Discretionary Shares non-Consid.

A and B, who were the equal common shareholders of Opco, each had personal holding companies (Holdco A and B) form an equally owned holding...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | a benefit can be conferred on a taxpayer even where no net economic benefit | 213 |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(b) | issuance of shares at less than FMV to joint Holdco of current shareholders could generate a deemed gain under s. 69(1)(b) | 154 |

18 October 2002 External T.I. 2002-0163615 F - Waiver of Capital Dividend

On the death of her husband, Ms. A received a bequest of all the common and Class A preferred shares of a private company (Portfolioco). Her...

14 August 2002 External T.I. 2001-0116385 F - PARTAGE DE COMMISSIONS

Where Mr. X, who is a shareholder of a life insurance firm (“Firm B”), sells mutual fund products on behalf of another firm (“Firm A”) of...

1998 Strategy Institute Round Table, No. 981310

S.56(2) will not apply where: the freezor exchanges common shares of an investment holding company ("Holdco") under s. 86(1) for redeemable...

29 October 1996 External T.I. 9630325 - TRUSTEE DIRECTING PAYMENT OR RIGHT TO INCOME

With respect to a testamentary trust with four trustees who are siblings and who are beneficiaries along with their spouses and children, RC found...

30 October 1995 Internal T.I. 9516317 F - VALIDITÉ DES DIVIDENDES DISCRÉTIONNAIRES

Discretionary dividends were found to be valid in light of the McClurg and Neuman decisions.

2 June 1995 External T.I. 9503755 - CHARITABLE GIFT ANNUITY IN RRSP

Discussion of application of ss.56(2) and 146(8) where an annuitant wishes to use some or all of the property in his RRSP to purchase a charitable...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 146 - Subsection 146(8) | 29 |

2 November 1994 Internal T.I. 9420446 - REDIRECTION OF SALARY DURING A STRIKE

Where the union and management negotiate an agreement whereby the union will supply a certain number of essential workers during a strike, with...

28 October 1994 External T.I. 9402465 - NON-CAP. LOSSES AND CORP. DEBT

In response to a question respecting intercorporate debt between related corporations designed to permit them to utilize non-capital losses within...

17 May 1993 Memorandum (Tax Window, No. 32, p. 2, ¶2592)

Pension income equally divided between two spouses as a result of a marriage breakdown would be subject to s. 56(2) in Alberta, but not in B.C.

11 May 1994 Memorandum 932735 (C.T.O. "IAAC Payments Applied to a Loan after Bankrupt Discharged")

In the case of a wrap-around IAAC where the taxpayer does not actually receive the funds, the annuity payments would ordinarily be included in the...

92 C.R. - Q.22

RC's position that s. 56(2) ordinarily will be applicable if a waiver of dividends in a closely held corporation is undertaken for the purpose of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | 29 |

92 C.R. - Q.22

RC will continue to assess a benefit in situations where a shareholder receiving a dividend on a discretionary share did not make adequate...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | 56 |

24 February 1992 Memorandum (Tax Window, No. 13, p. 12, ¶1628)

Generally, s. 56(2) will not be applied in the case of a waived or discretionary dividend where the shareholders deal at arm's length with one...

13 November 1990 T.I. (Tax Window, Prelim. No. 2, p. 9, ¶1044)

Ss.56(2) and (4.1) will apply to a family mortgage plan under which a parent purchases a GIC from a financial institution at less than the going...

23 March 1990 T.I. (August 1990 Access Letter)

In response to a suggestion that a corporation could be purged of non-qualifying assets in order to qualify as a qualified small business...

14 July 1989 Inter-Divisional Memorandum (Dec. 89 Access Letter, ¶1045)

In a situation similar to McClurg, where both the husbands and the wives held shares of the corporation and the corporation declared dividends...

87 C.R. - Q.72

S.56(2) applies where the board has the discretion to pay dividends on one or more classes of shares at its discretion. McClurg is being appealed.

86 C.R. -Q.40

It would be "unlikely" that s. 56(2) would apply to an income-splitting to which s. 74.4 doesn't apply by virtue of the small business corporation...

86 C.R. - Q.41

It is not possible to state that it is ever possible to waive dividends in favour of related shareholders without the application of s. 56(2).

85 C.R. - Q.6

Where the taxpayer is assessed under s. 56(2), the recipient's income (particularly where not statute-barred) will be reduced.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | 17 |

84 C.R. - Q.24

S.56(2) will ordinarily be applicable if the waiver of dividends in a closely held corporation is undertaken for the purpose of transferring...

84 C.R. - Q.82

RC will accept the payment of large discretionary dividends as a special recompense to the active shareholders, provided that the non-active...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 67 | 56 |

81 C.R. - Q.26

s. 56(2) would ordinarily be applicable if the waiver of dividends in a closely held corporation is undertaken for the purpose of transferring...

79 C.R. - Q.19

Where a waiver of dividends in a closely-held corporation is undertaken for the purpose of transferring income to the other shareholders...

IT-468R "Management or Administration Fees Paid to Non-residents" (Archived) 29 December 1999

The portion of a management or administration fee paid to a non-resident affiliate that is in excess of a reasonable amount may be treated as a...

IT335R2 "Indirect Payments" 12 July 2004

13. An amount to which subsection 56(2) applies could be included in the income of both the taxpayer and the person who receives the payment or...

Articles

Bowman, "New Wine in Old Bottles - Using Personal Trusts as Business Vehicles", Business Vehicles, Vol. III, No. 1, 1996, p. 114

"Trust-partnership structures may permit greater flexibility than a single corporation ... since management of the business can be left in the...