Mortgage Industry Consultation on a Potential Income Verification Tool – What we learned report

Disclaimer

We do not guarantee the accuracy of this copy of the CRA website.

Scraped Page Content

Mortgage Industry Consultation on a Potential Income Verification Tool – What we learned report

July 2025

On this page

- Executive summary

- Background

- What we learned

- Current income verification practices and challenges

- Income verification opportunities for the future

- Additional roundtable questions

- Would you rely solely on the information provided by the CRA to verify a borrower’s income? If not, what other sources would you rely on?

- What (if any) consequences would there be if a lender is unable to verify the borrower’s income through the CRA?

- What is the cost of mortgage fraud for your organization? What would you be willing to contribute to develop an income verification tool?

- Conclusion

- Appendix

Executive summary

The federal government is committed to fighting mortgage fraud through income verification, as announced in Budget 2024. The 2024 Fall Economic Statement announced that the Canada Revenue Agency (CRA) has expanded its outreach to the broader financial sector, including mortgage lenders, on how to best design and implement a new tool to combat mortgage fraud. It further states that the CRA aims to begin implementing this measure in early 2025.

In the fall of 2024, the CRA consulted mortgage industry professionals on developing a tool to verify borrowers’ income. The CRA hosted roundtables for representatives of mortgage industry associations to discuss challenges verifying income and opportunities to support the industry and reduce risks of mortgage fraud. In addition, the CRA published an online questionnaire for all mortgage industry members to provide input.

Participants from the roundtables and the online questionnaire were consistent in their input. Both expressed concern about growing trends in mortgage fraud, including fake or altered documentation to inflate income when obtaining a mortgage. Participants were clear that a tool created by the CRA that allows mortgage professionals to verify the validity of a borrower’s income would streamline the mortgage approval process and reduce the risks of fraud significantly.

Participants provided valuable input on how a CRA income verification process should work and the information it should provide users. Information that is most relevant in the mortgage approval process includes the borrower’s name, income (total income, net income, and taxable income), and debts owed to the CRA for the last two years. They also highlighted key considerations for developing the tool, including the borrower’s consent, security of information sharing, real-time information sharing capability, and concern for users who may not have access to CRA digital services.

This report includes an overview of the consultation design and results, what we learned from participants, and next steps.

Background

Budget 2024 announced the Government of Canada’s intention to consult with the mortgage industry about a tool to help lenders verify income for mortgages.

The CRA led the consultation to develop a potential solution in collaboration with key players in the mortgage industry.

Borrowers must disclose their sources of income to get a mortgage. As proof, lenders typically ask borrowers to provide one or more of these Canadian tax documents:

- a proof of income statement

- tax information slips

- a notice of assessment

- a statement of income and deductions

Given the potential for mortgage fraud at the income disclosure stage of the transaction, the mortgage industry is interested in an income verification tool to improve the experience of borrowers and to combat possible fraud.

While combating mortgage fraud falls outside the scope of the CRA’s core mandate, the CRA holds many of the documents required by lenders as proof of income. Therefore, industry stakeholders have expressed interest in verifying borrowers’ information with the CRA directly.

Consultation overview

In the fall of 2024, the CRA invited national associations within the mortgage industry to participate in roundtable discussions to gather input on a potential income verification tool that would help combat mortgage fraud. During the roundtable discussions, participants had the opportunity to share their views on:

- the current state of, challenges with, and opportunities with income verification practices in Canada for mortgage borrowers

- the needs, opportunities, and considerations for a potential new income verification tool that is fully digital

In addition to the roundtable discussions, the CRA sought broader input from other interested and affected parties within the industry through an online questionnaire.

Roundtables

The following organizations participated in the roundtables:

- banks: Canadian Bankers Association

- credit unions: Canadian Credit Union Association, Servus Credit Union, and Desjardins

- mortgage and title insurers: Mortgage and Title Insurance Industry Association of Canada

- mortgage brokers: Canadian Mortgage Brokers Association and Mortgage Professionals of Canada

- mortgage finance companies: CMLS Financial & Nesto

- alternative mortgage associations: Canadian Alternative Mortgage Lenders Association

The CRA hosted two virtual roundtables with stakeholders (see Table 1). The roundtables were well received by participants. Participants said they were pleased the CRA had consulted them and emphasized that Canadian tax documents are a crucial part of reducing and mitigating fraud in the mortgage application process. They also expressed an interest in being involved throughout the decision-making and implementation process going forward.

| Date | Language | Number of participants |

|---|---|---|

| November 26, 2024 | English | 18 |

| November 27, 2024 | French | 5 |

Online questionnaire

The questionnaire was available on Canada.ca from November 14, 2024, to December 6, 2024, and shared by email with mortgage industry stakeholders, including the provincial and territorial financial regulators and banking, housing, and real estate associations.

The questionnaire received 1,637 completed submissions from industry members across Canada (see Table 2). To improve our processes, participant responses were analyzed with support from CRA’s internal Artificial Intelligence (AI) tool. Participant responses were not and will not be used to train the large language model (used in the AI tool). CRA employees reviewed data to ensure no personal information provided in participant responses was entered into the tool. CRA employees also reviewed the AI-generated findings for accuracy and led the report writing.

Note: response percentages are calculated to 2 decimals but displayed as rounded numbers in this report. This may cause added percentages to appear ± 1% of the total. In some cases, totals may appear not to add up to 100% due to this rounding.

| Type of organization | Location | Primary language |

|---|---|---|

|

|

|

What we learned

Roundtable and online questionnaire participants provided insight into the income verification practices and challenges as well as mortgage fraud trends. Overall, input was consistent across the various players in the mortgage industry. They made suggestions for how an income verification tool for the industry could increase efficiency and reduce the risk of fraud.

Current income verification practices and challenges

Trends in the mortgage fraud environment

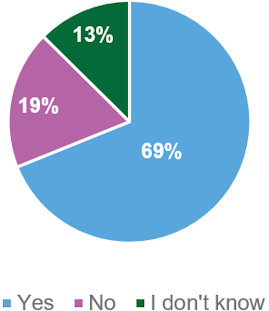

Most of the questionnaire participants (69%) said they are aware of trends in the mortgage fraud environment (see Chart 1). The major trend participants identified was fake or altered documents. Other potential issues noted were money laundering, fraud to qualify for a larger mortgage, and fraud within the industry.

Chart 1: Trends in the mortgage fraud environment

Responses to Question 1: Are you aware of any trends in the mortgage fraud environment? Base: All participants (n=1,637)

Text version for Chart 1: Trends in the mortgage fraud environment

Text version for Chart 1: Trends in the mortgage fraud environment

| Response | Percentage |

|---|---|

| Yes | 69% |

| No | 19% |

| I don’t know | 13% |

Steps lenders and mortgage brokers take to verify a borrower’s disclosed income

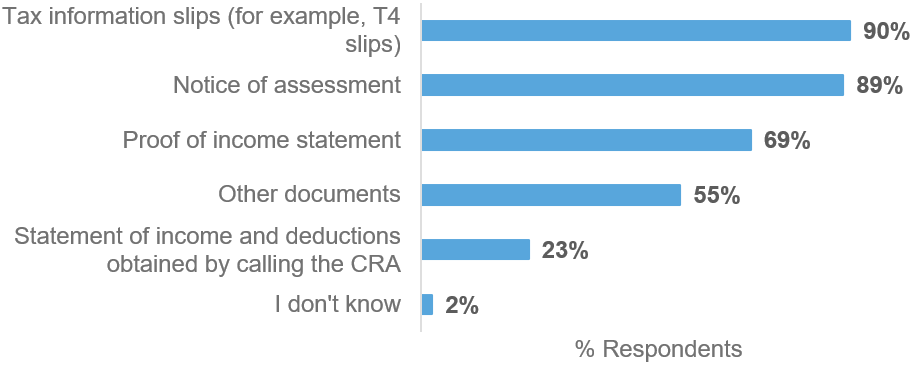

Participants confirmed that the current income verification process requires that brokers, lenders, underwriters, and insurers take multiple steps to verify a borrower’s identity and documents. For example, the process typically involves confirming employment directly with the employer and examining requested financial documents from the borrower, particularly CRA documents (see Chart 2).

The documents cited as being used most frequently for income verification include:

- income slips, such as the T4 slip, Statement of Remuneration Paid

- notices of assessment

- proof of income statements, which breakdown income by type (for example, earned, interest, grants)

Other CRA-held documents mentioned were:

- Canada child benefit (CCB) statements

- a statement of account to determine if the borrower owes money to the CRA

Non-CRA documents mentioned include employment letters, paystubs, and bank statements.

Chart 2: Financial documents requested of borrowers

Responses to Question 2: What financial documents do lenders and mortgage brokers ask borrowers to provide during the mortgage approval process? Base: All participants (n=1,637), 5,376 total responses

Text version for Chart 2: Financial documents requested of borrowers

Text version for Chart 2: Financial documents requested of borrowers

| Response | Percentage |

|---|---|

| Tax information slips (for example, T4 slips) | 90% |

| Notice of assessment | 89% |

| Proof of income statement | 69% |

| Other documents | 55% |

| Statement of income and deductions obtained by calling the CRA | 23% |

| I don’t know | 2% |

Participants also said they request the T1 return, officially referred to as the taxpayer’s income tax and benefit return, filed by the borrower to see a breakdown of their reported income that could be used to qualify for a mortgage, particularly for borrowers that are self-employed or have rental income.

Income verification opportunities for the future

Access to the income verification tool

Most questionnaire participants said that stakeholders including banks, mortgage brokers, credit unions, and mortgage finance companies should have access to the income verification tool (see Chart 3). Some expressed that no one should have access to an income verification tool, as income is personal information between the CRA and the taxpayer.

Chart 3: Suggested tool users

Responses to Question 4: Who should have access to the tool? Base: All participants (n=1,637), 7,221 total responses

Text version for Chart 3: Suggested tool users

Text version for Chart 3: Suggested tool users

| Response | Percentage |

|---|---|

| Banks | 85% |

| Mortgage brokers | 75% |

| Credit unions | 72% |

| Mortgage finance companies | 65% |

| Credit bureaus | 46% |

| Provincial and territorial financial institution regulators | 44% |

| Mortgage or title insurers | 43% |

| Other | 8% |

| I don’t know | 3% |

Information sharing process between the CRA, the borrower, and third parties

Participants gave many suggestions for how an income verification process should work. The most common suggestion was to use a new or existing CRA portal that would allow mortgage professionals to obtain information with the borrower’s authorization. They also suggested the tool be integrated with existing mortgage application platforms, such as an application programming interface (API) solution, like the process for accessing consumer credit information. Participants also stressed that the tool should be digital, and the response from the tool should be provided in real-time to be consistent with the industry’s digital solutions and speed of transactions.

Furthermore, roundtable participants highlighted that the tool’s accessibility should consider financial institutions with limited resources. For example, smaller institutions may not have technological resources to integrate the tool into their existing systems through an API and may need to access the tool through a standalone CRA portal.

Additionally, others noted that an income verification tool would need to account for the fact that some borrowers may not have access to existing CRA online services (such as seniors or those in rural areas).

Participants also suggested the income verification tool follow a similar process such as Represent a Client and document retrieval services to allow mortgage professionals to request documents from the CRA. CRA officials acknowledged during roundtable discussions that using these services to obtain taxpayer documents from the CRA is currently prohibited but that the technologies and functionalities discussed could be further explored to develop a potential income verification tool.

Others indicated that confirmation by the CRA on the validity of the borrower’s documents would be sufficient to verify income, as opposed to requesting documents directly from the CRA.

Minimum information required to verify income

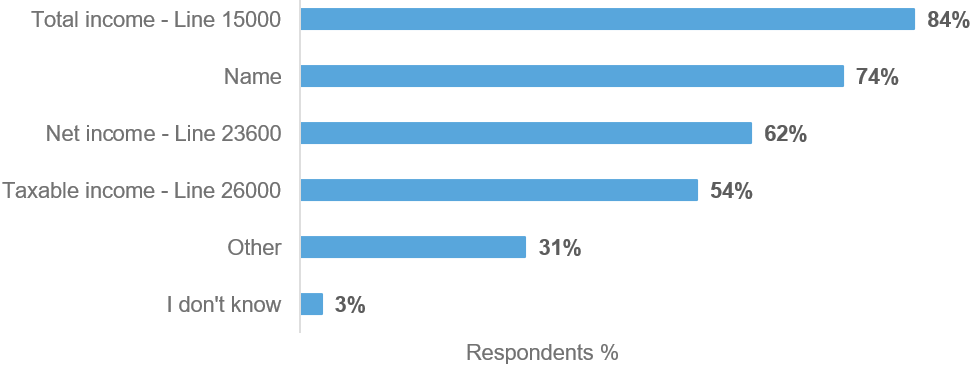

When asked about the minimum amount of information required to verify income, most participants indicated that the borrower’s name, as well as their total income, net income, and taxable income (on lines 15000, 23600, and 26000 of their income tax and benefit return) would be required (see Chart 4).

Chart 4: Minimum information required to verify income

Responses to Question 6: What is the minimum information you would require from the CRA to verify the borrower's income? Base: All participants (n=1,637), 5,027 total responses

Text version for Chart 4: Minimum information required to verify income

Text version for Chart 4: Minimum information required to verify income

| Response | Percentage |

|---|---|

| Total income – Line 15000 | 84% |

| Name | 74% |

| Net income – Line 23600 | 62% |

| Taxable income – Line 26000 | 54% |

| Other | 31% |

| I don’t know | 3% |

Participants indicated they would like as much information as possible to verify income, including the borrower’s tax returns, tax slips and statement of account. In particular, they said they would require a breakdown of the type of income and amounts that contribute to the amount on line 15000, including details on self-employment deductions and rental and business income. Roundtable participants reiterated that the tool should be built by factoring in diversity of income streams, including gig work and self-employment income. Participants also mentioned that it is important to know if a borrower owes money to the CRA as this may impact the lender’s decision on the application.

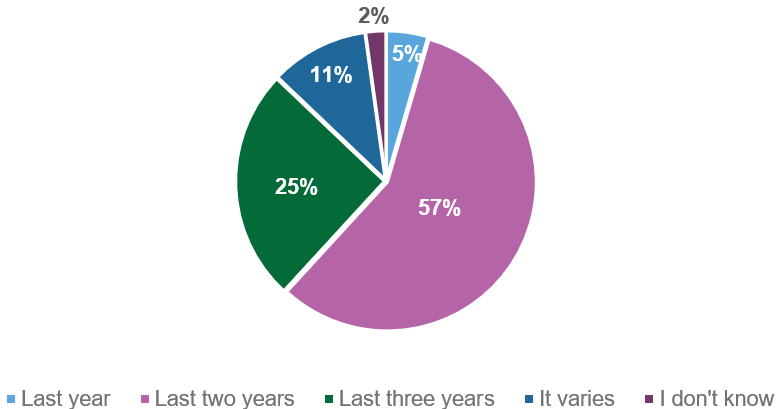

Most participants said that the minimum number of years of information required from the CRA is two years (see Chart 5). During the roundtable discussion, participants emphasized that this was important to understand historic income and identify trends, which can be particularly important for those who are self-employed or gig workers. Some even mentioned that five years of information is ideal, but two years is the industry average.

Chart 5: Years of income information required

Responses to Question 8: How many years of information would you require from the CRA to verify the borrower's income? Base: All participants (n=1,637)

Text version for Chart 5: Years of income information required

Text version for Chart 5: Years of income information required

| Response | Percentage |

|---|---|

| Last two years | 57% |

| Last three years | 25% |

| It varies | 11% |

| Last year | 5% |

| I don’t know | 2% |

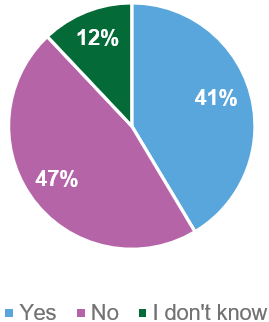

Yes/no validation from the CRA

Participants of the online questionnaire were divided on whether a yes/no validation of a borrower’s income from the CRA would be enough to meet their needs (see Chart 6).

Chart 6: Yes/no validation

Responses to Question 7: Would a “yes/no” validation from the CRA of a borrower’s income be enough to meet your needs? Base: All participants (n=1,637)

Text version for Chart 6: Yes/no validation

Text version for Chart 6: Yes/no validation

| Response | Percentage |

|---|---|

| No | 47% |

| Yes | 41% |

| I don’t know | 12% |

Those who said a yes/no response would not meet their needs (47%) were asked to explain why the information would not be sufficient, and they gave a variety of reasons.

Source of income

One of the main concerns expressed by participants is the need for a detailed breakdown of a borrower’s income. Participants explained that a yes/no validation of income would be insufficient because it lacks the detail required to adequately verify documents and have a full view of a borrower’s financial situation to make lending decisions. They require specific figures and breakdowns of income (for example, employment income, investment and rental income, capital gains, and Canada child benefit payments) as part of the mortgage application for several reasons.

Lenders have different requirements and offer different lending products based on individual financial situations. Mortgage professionals often need to be able to calculate a two-year average income to qualify borrowers who have multiple income sources or variable income. Consequently, self-employed borrowers are typically asked to provide their complete income tax and benefit return to show gross and taxable income and source of income.

Furthermore, participants explained that not all sources of income qualify for a mortgage application. Income such as registered retirement savings plan withdrawals, capital gains, and employment insurance benefits, which would appear on line 15000, “total income” may not qualify in some cases. An individual may intentionally or mistakenly give inaccurate information about the specifics of their income, while still matching CRA’s record of their total income. As such, a simple yes/no validation of a borrower’s income may not offer insight on all sources of revenue, which mortgage professionals need to be able to identify in case of any discrepancies that may indicate fraudulent activity.

Access to documents

Participants also explained that a yes/no validation of income would be insufficient because it does not provide them with access to verified tax documents or “physical” confirmation they can use to document a borrower’s file. Having access to a borrower’s tax documents not only allows them to examine their sources of income, but it is also generally required by lenders to have on file for mortgage applications as well as regulatory and compliance purposes. They also explained that they need to know if a borrower owes money to the CRA as part of their risk assessment, which requires obtaining a statement of account from the CRA. Overall, there is a concern that brokers would not be able to share the CRA’s yes/no response with lenders or that lenders would not accept a yes/no income verification by the CRA, which would diminish the value and use of CRA’s verification.

Participants expressed that they want to be able to obtain copies of a borrower’s Canadian tax documents directly from the CRA. This solution would allow them to help their clients who have difficulty accessing their tax documents and eliminate the opportunity for borrowers to submit fraudulent tax documents.

Potential for inaccurate results

Participants raised that a yes/no response by the CRA could cause issues for borrowers, mortgage professionals, and the CRA. They were concerned that small discrepancies in the reported income could result in a “no” response, which could be due to a minor typo, rounding the number, or a reassessment of their taxes. The borrower could also underreport their income in their mortgage application (for example, by not including overtime, bonuses, or additional employment), which could cause a “no” response.

This could further complicate the income verification process for the mortgage professional and borrower if the “no” response doesn’t include an explanation, causing the mortgage professional and borrower to seek clarification from the CRA and delaying the process.

Participants highlighted that the consequences of a false negative could be impactful. Delays in the income verification process could jeopardize a borrower’s purchase. A “no” response could also jeopardize the relationship between a mortgage professional and a borrower if the professional is not able to continue the mortgage application process. Instead, participants suggested the income verification tool respond with a number, which brokers and lenders can use to negotiate a lending amount with the borrower and continue the relationship. Alternatively, some proposed the tool respond with a yes/no type of response if the number is within or outside a specific range.

Protections for users of the income verification tool

To protect taxpayer information, participants acknowledged that the income verification process must include the borrower’s consent. When asked how the income verification tool should prevent unauthorized access to or misuse of tax information, participants suggested the tool:

- be secure with two-factor authentication to ensure only verified individuals can access the tool

- be accessible only to assigned users

- send notifications to the borrower when their information is being accessed

- have a time limit for the user to access the information

In addition, roundtable participants proposed an audit mechanism that will monitor the use of the tool to protect borrowers’ personal information.

Additional roundtable questions

The roundtables included three additional questions for discussion.

Would you rely solely on the information provided by the CRA to verify a borrower’s income? If not, what other sources would you rely on?

Participants commented that the information provided by the CRA to verify a borrower’s income would not be the only means of verification. They confirmed that other processes already exist to verify income, as described in the section about the steps lenders and mortgage brokers take to verify a borrower’s disclosed income (for example, confirming employment directly with the employer), and would continue to be used. Because Canadian tax documents provide historical income information, the CRA income verification tool could be used to verify the borrower’s reported income only for previous years.

However, they noted that a digital CRA tool would be the most efficient option and that it would likely become a tool heavily relied on by the industry because of the importance of Canadian tax documents in the mortgage approval process.

What (if any) consequences would there be if a lender is unable to verify the borrower’s income through the CRA?

Participants generally acknowledged they would use existing methods, such as examining tax documents, to verify borrower income if a borrower chooses not to use the tool provided by the CRA. However, they strongly reiterated that there is a need for the government to provide tools or resources to help mortgage professionals verify income and detect and report on suspicious or fraudulent activity to cut down on fraud in the industry.

What is the cost of mortgage fraud for your organization? What would you be willing to contribute to develop an income verification tool?

Participants said mortgage fraud costs the industry heavily. As noted by Mortgage Professionals Canada, “for every $1 lost to fraud it takes $4 for lenders to recoup.” Some participants said they would be willing to pay for an income verification tool since they have already been incurring such costs with third-party services (such as Equifax) and the benefits would outweigh reasonable costs for access to the tool and its services. One of the ideas discussed was a cost-per-use model by subscription (paying to access the service) or billing after usage. In addition, mortgage fraud has non-monetary costs for the industry, including time and reputation. Current income verification practices take a lot of time to complete. Furthermore, the foreclosure process on a property where the borrower is unable to make their payments can take up to a year, and cost approximately 20% to 30% of the property’s value.

Some participants said they would be willing to pay for an income verification tool if the benefits outweigh reasonable costs for access to the tool and its services. They were open to a cost-per-transaction model, flat monthly rates, or annual subscriptions. They shared that they had previously used third-party services that granted brokers and lenders access to borrowers’ documents with the borrower’s consent. They described the process as seamless, easy to understand, helpful for clients, and a worthwhile business expense.

Participants also pointed out that the tool should be built with the goal of catching the fraudster. Otherwise, they will continue perpetrating fraud and costing the industry. To mitigate this risk, participants proposed the CRA create an alert on a taxpayer’s credit bureau file to prevent them from submitting future applications through other brokers.

Conclusion

The purpose of the consultation was to learn from the mortgage industry about mortgage fraud and what type of income verification tool could help mitigate the risks of fraud. Participants were clear that a tool built by the CRA that allows mortgage professionals to verify the validity of borrowers’ income would streamline the mortgage approval process and reduce the risks of fraud significantly.

Based on the consultation findings, the most useful CRA documents for the mortgage industry to verify borrowers’ income are:

- notices of assessment

- proof-of-income statements

- income tax slips

- statements of account showing debt owed to the CRA

Participants expressed that an income verification tool should:

- include the borrower’s consent to share the information

- give users an immediate response

- be accessed through a secure online service, whether an existing CRA portal or a new one created for this purpose

- account for the fact that some borrowers may not have access to existing CRA online services

- be secure

Given the need for mortgage brokers to provide verified (official) documents to lenders, participants would like copies of CRA documents. However, a notable number (41%) of participants of the online questionnaire said it would be sufficient for the CRA to confirm that a borrower’s documents are valid. Participants highlighted that the CRA’s confirmation would need to indicate sources of income (such as employment and investments) and be shareable with lenders. They also said the CRA should consider the potential for false negatives due to system errors.

Next steps

The CRA has been actively consulting with international tax administration partners and IT, privacy, security, and legal experts to identify options that would help financial institutions detect and deter fraud in a manner that is secure, user-friendly, and compatible with the CRA’s systems.

The CRA has carefully reviewed participants’ feedback and will use it to inform decisions on the potential design and implementation of a new tool and consider opportunities to engage mortgage borrowers in the future on their needs, preferences, and concerns for the tool.

Appendix

Online questionnaire

Current income verification practices and challenges

- What key trends are you aware of in the mortgage fraud environment?

- [If yes] Please describe the trends you are aware of.

- What steps do lenders and brokers take to verify a borrower’s income in the mortgage approval process?

- What documents are borrowers asked to provide?

Income verification opportunities for the future

- Who should have access to the tool?

- How should the process of sharing income information between the CRA, the borrower, and third parties work?

- What is the minimum information you would require from the CRA to verify the borrower’s income?

- Would a “yes/no” validation from the CRA of a borrower’s income be enough to meet your needs?

- [If No] Please explain why a “yes/no” response would not meet your needs.

- How many years of information would you require from the CRA to verify the borrower's income?

- What protections should users of the income verification tool have in place to prevent unauthorized access or misuse of tax information?

Roundtable discussion guide

Current income verification practices and challenges

- What key trends are you aware of in the mortgage fraud environment?

- [If yes] Please describe the trends you are aware of.

- What steps do lenders and brokers take to verify a borrower’s income in the mortgage approval process?

- What documents are borrowers asked to provide?

Income verification opportunities for the future

- How should the process of sharing income information between the CRA, the borrower, and third parties work?

- Who should have access to the tool?

- What is the minimum information you would require from the CRA to verify the borrower’s income?

- How many years of information would you require from the CRA to verify the borrower's income?

- Would a “yes/no” validation from the CRA of a borrower’s income be enough to meet your needs?

- If not, why not?

- Would you rely solely on the information provided by the CRA to verify a borrower’s income?

- If not, what other sources would you rely on?

- What (if any) consequences would there be if a lender is unable to verify the borrower’s income through the CRA?

- What protections should users of the income verification tool have in place to prevent unauthorized access or misuse of tax information?

- What is the cost of mortgage fraud for your organization?

- What would you be willing to contribute to develop an income verification tool?

Page details

2025-07-11