Infographic: Supporting Canadian Innovation

Disclaimer

We do not guarantee the accuracy of this copy of the CRA website.

Scraped Page Content

Infographic: Supporting Canadian Innovation

Did you know that the SR&ED Tax Incentive Program is the largest Government of Canada program supporting research and development in Canada? Click on this infographic to learn more about the available tax incentives, benefits, eligibility requirements and available services the CRA offers.

Supporting Canadian Innovation

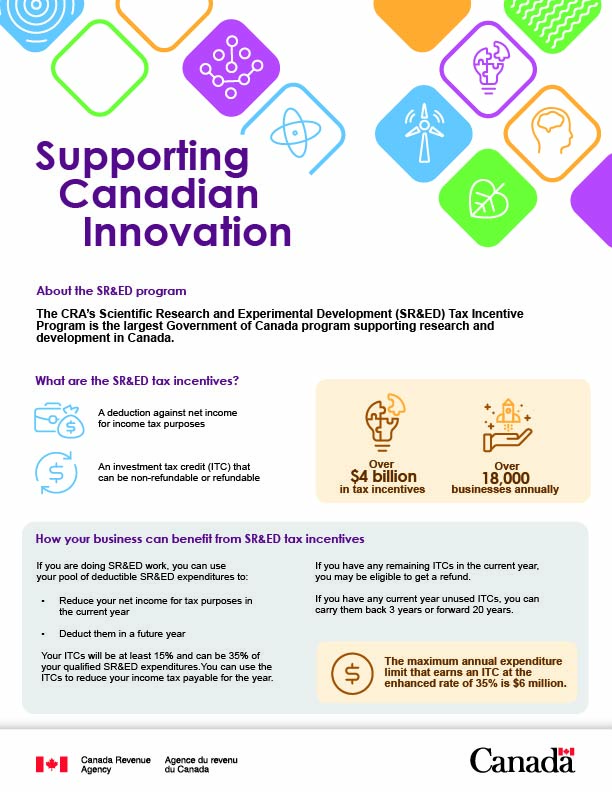

About the SR&ED Program

The CRA’s Scientific Research and Experimental Development (SR&ED) Tax Incentive Program is the largest Government of Canada program supporting research and development in Canada.

- Over $4 billion in tax incentives annually

- Over 18,000 businesses annually

What are SR&ED tax incentives?

- A deduction against net income for income tax purposes

- An investment tax credit (ITC) that can be non-refundable or refundable

How your business can benefit from SR&ED tax incentives

If you are doing SR&ED work, you can use your pool of deductible SR&ED expenditures to:

- Reduce your net income for tax purposes in the current year

- Deduct them in a future year

Your ITCs will be at least 15% and can be 35% of your qualified SR&ED expenditures. You can use the ITCs to reduce your income tax payable for the year. If you have remaining ITCs in the current year, you may be eligible to get a refund.

If you have any current year unused ITCs, you can carry them back 3 years or forward 20 years.

The maximum annual expenditure limit that earns an ITC at the enhanced rate of 35% is $6 million.

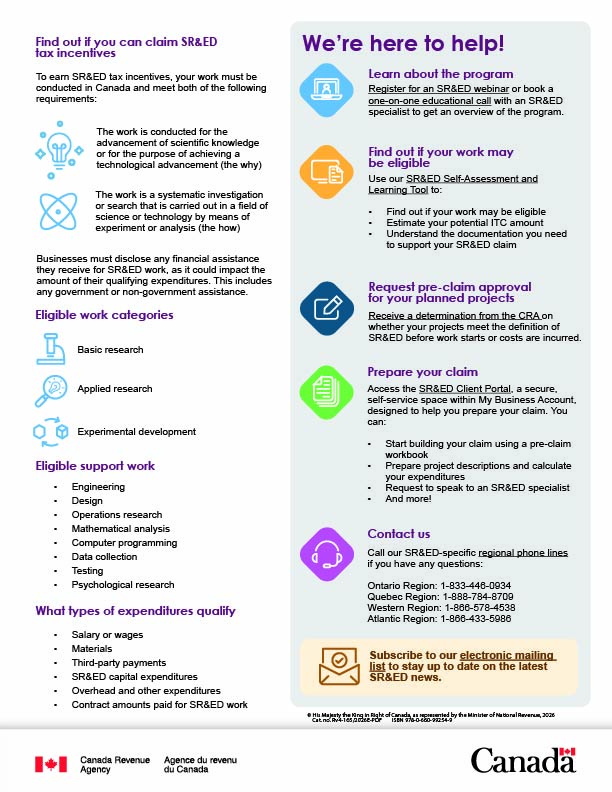

Find out if you can claim SR&ED tax incentives

To earn SR&ED tax incentives, your work must be conducted in Canada and meet both of the following requirements:

- The work is conducted for the advancement of scientific knowledge or for the purpose of achieving a technological advancement (the why)

- The work is a systematic investigation or search that is carried out in a field of science or technology by means of experiment or analysis (the how)

Businesses must disclose any financial assistance they receive for SR&ED work, as it could impact the amount of their qualifying expenditures. This includes any government or non-government assistance.

Eligible work categories

- Basic research

- Applied research

- Experimental development

Eligible Support work

- Engineering

- Design

- Operations research

- Mathematical analysis

- Computer programming

- Data collection

- Testing

- Psychological research

What types of expenditures qualify

- Salary or wages

- Materials

- Third-party payments

- SR&ED capital expenditures

- Overhead and other expenditures

- Contract amounts paid for SR&ED work

We’re here to help!

Learn about the program

Register for an SR&ED webinar or book a one-on-one educational call with an SR&ED specialist to get an overview of the program.

Find out if your work may be eligible

Use our SR&ED Self-Assessment and Learning Tool to:

- Find out if your work may be eligible

- Estimate your potential ITC amount

- Understand the documentation you need to support your SR&ED claim

Request pre-claim approval for your planned projects

Receive a determination from the CRA on whether your projects meet the definition of SR&ED before work starts or costs are incurred.

Prepare your claim

Access the SR&ED Client Portal, a secure, self-service space within My Business Account, designed to help you prepare your claim. You can:

- Start building your claim using a pre-claim workbook

- Prepare project descriptions and calculate your expenditures

- Request to speak to an SR&ED specialist

- And more!

Contact us

Call our SR&ED-specific regional phone lines if you have any questions:

- Ontario Region: 1-833-446-0934

- Quebec Region: 1-888-784-8709

- Western Region: 1-866-578-4538

- Atlantic Region: 1-866-433-5986

Subscribe to our electronic mailing list to stay up to date on the latest SR&ED news.

Page details

2026-04-23