Loral/ Telesat -- summary under Delaware etc. Mergers

Overview

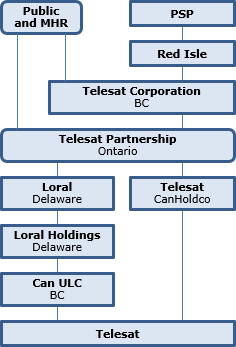

Telesat Canada, a Canadian corporation and global satellite operator that was mostly owned by Loral Space & Communications Inc. (a US public corporation) and Public Sector Pension Investment Board effected a sort of merger transaction in which both Telesat and Loral became subsidiaries of an Ontario LP (Telesat Partnership) whose general partner (Telesat Corporation) became a TSX and NASDAQ-listed corporation. The transaction was largely accomplished through a merger of Loral with a Loral Delaware subsidiary (with Loral as the survivor) on which the public Loral shareholders were given the choice of receiving units of Telesat Partnership that are exchangeable into the (listed) shares of Telesat Corporation, or such shares of Telesat Corporation itself.

US tax counsel opined that Telesat Corporation should not be deemed to be a US corporation under Code s. 7874 and that Telesat Partnership should not be treated as a publicly traded partnership or a US corporation. The exchanges by the Loral shareholders for shares of Telesat Corporation or units of Telesat Partnership were considered to be non-recognition transactions under Code s. 351 or s. 721.

The merger did not qualify as a foreign merger, so that no Canadian rollover treatment applied. The resulting sandwich structure entailed a non-Canadian partnership (Telesat Partnership – held by a B.C. corporation, Telesat Corporation) holding shares of a controlled foreign affiliate (Loral) which, in turn, received FAPI income in the form of Canadian-source dividends. The disclosure states that, assuming a full current distribution of dividends at the various levels:

Telesat Corporation may deduct in computing its taxable income a prescribed portion of such dividends received by it through Telesat Partnership. In determining the amount of such dividends from Loral that may be deducted in computing its taxable income, Telesat Corporation intends not to take into account any deduction claimed by Telesat Partnership pursuant to subsection 91(5) of the Tax Act. Telesat Corporation believes that such interpretation is consistent with the rationale expressed by the CRA for its published administrative position in this regard, so that there would be no net income inclusion to the partnership, and it was considered appropriate that there also should be no net inclusion to Telesat Corporation.

These deductions would also address Telesat Partnership being a SIFT partnership.

Telesat

Telesat, a Canadian corporation and a leading global satellite operator, providing its customers with communications services.

Telesat Corporation

Telesat Corporation, a newly-formed B.C. corporation, anticipated to be the new Canadian-controlled publicly traded entity in which Telesat Canada’s current direct and indirect shareholders may elect to receive Telesat Corporation Shares, and the general partner of Telesat Partnership.

Loral

Loral Space & Communications Inc., a Delaware public corporation holding a 62.6% economic interest and 32.6% voting interest in Telesat.

Telesat Partnership

Telesat Partnership LP, an Ontario limited partnership formed under the laws of Ontario, Canada in which Telesat’s current direct and indirect shareholders may elect to receive Telesat Partnership Units.

Telesat CanHoldco

Telesat CanHold Corporation, a B.C. corporation, and a wholly-owned subsidiary of Telesat Partnership. It is anticipated to hold approximately 37% of Telesat following consummation of the Transaction.

Merger Sub

Lion Combination Sub Corporation, a Delaware corporation and wholly owned subsidiary of Loral formed by Loral for the purpose of engaging in the Transaction pursuant to the terms of the Transaction Agreement and that will merge with and into Loral, with Loral surviving the Merger.

PSP Investments

Public Sector Pension Investment Board, a Canadian Crown corporation that holds its 36.7% equity interest, 67.4% voting interest on all matters except for the election of directors, and 29.4% voting interest for the election of directors in Telesat through a wholly owned subsidiary, Red Isle, a corporation organized under the CBCA.

Red Isle

Red Isle Private Investments Inc., a Canadian corporation and a wholly-owned subsidiary of PSP Investments.

MHR

MHR Fund Management LLC, a New York-based private equity firm and a major stockholder of Loral. Various funds affiliated with MHR and Dr. Rachesky held, as of September 30, 2021, approximately 39.9% of the outstanding voting common stock and 58.4% of the combined outstanding voting and non-voting common stock of Loral.

Transaction Agreement

The Transaction Agreement and Plan of Merger dated as of November 23, 2020 between Telesat, , Loral,Telesat CanHoldco), Merger Sub, PSP Investments, and Red Isle.

Transaction Steps

On November 18 and 19, 2021 and November 19, 2021, the Transaction Agreement was implemented, including:

- on November 18, 2021, Red Isle contributing 272,827 Telesat Non-Voting Participating Preferred Shares to Telesat in exchange for Class C fully voting shares of Telesat Corporation (“Class C Shares”) and the balance of its equity interest in Telesat to Telesat Partnership in exchange for class C units of Telesat Partnership (“Class C Units”);

- on November 18, 2021 and pursuant to stockholder contribution agreements, the contribution by current and former members of management of Telesat of their Telesat Non-Voting Participating Preferred Shares to Telesat Corporation in exchange for newly issued Class A common shares of Telesat (the “Class A common shares”) if such contributing shareholder is Canadian (as defined in the Investment Canada Act) or newly issued Class B variable voting shares of Telesat Corporation (the “Class B variable voting shares”) if such contributing shareholder is not Canadian;

- on November 18, 2021 and pursuant to the director contribution agreement, the contribution by John Cashman and Clare Copeland of their Telesat Director Voting Preferred Shares to Telesat Partnership in exchange for interests in Telesat Partnership, which were subsequently redeemed by Telesat Partnership for cash on November 19, 2021;

- on November 18, 2021 and pursuant to optionholder exchange agreements, the exchange of options, tandem stock appreciation rights and restricted stock units in respect of Telesat for corresponding instruments in Telesat Corporation with the same vesting terms and conditions; and

- on November 19, 2021, the merger of Merger Sub with and into Loral (the “Merger”), with Loral surviving the Merger as a wholly owned subsidiary of Telesat Partnership and the other Loral stockholders receiving shares of Telesat Corporation or units of Telesat Partnership as described below.

- Under the terms of the Transaction Agreement, at the effective time of the Merger (the “Effective Time”), each share of Loral common stock outstanding immediately prior to the Effective Time was converted into the right to receive:

(a) if the Loral stockholder validly made an election to receive units of Telesat Partnership pursuant to the Merger (a “Unit Election”), one newly issued Class A unit of Telesat Partnership if such Loral stockholder was Canadian (as defined above), and otherwise one newly issued Class B unit of Telesat Partnership,

(b) if the Loral stockholder validly made an election to receive shares of Telesat Corporation (a “Shares Election”), one newly issued Class A common share if such Loral stockholder was Canadian, or

(c) if the Loral stockholder validly made a Shares Election and was not Canadian, or did not validly make a Unit Election or a Shares Election, one newly issued Class B variable voting share. Following the Transaction, Telesat became an indirect wholly owned subsidiary of Telesat Corporation.

- In addition, on November 18, 2021, Telesat Corporation entered into the trust agreement and trust voting agreement with Telesat Partnership, TSX Trust Company as the trustee of Telesat Corporation Trust and, in the case of the trust agreement, Christopher DiFrancesco, effectuating the voting trust relating to the voting rights of units of Telesat Partnership.

Result of Transaction

The Transaction will result in the current stockholders of Loral, PSP Investments (through Red Isle) and other shareholders in Telesat (principally current or former management) owning approximately the same percentage of equity in Telesat indirectly through Telesat Corporation and/or Telesat Partnership as they currently hold (indirectly in the case of Loral stockholders and PSP Investments) in Telesat, Telesat Corporation becoming the publicly traded general partner of Telesat Partnership and Telesat Partnership indirectly owning all of the economic interests in Telesat, except to the extent that the other shareholders in Telesat elect to retain their direct interest in Telesat.

Investor Rights Agreements

Telesat Corporation and MHR, on the one hand, and Telesat Corporation and PSP Investments, on the other hand, entered into the Investor Rights Agreements dated as of November 23, 2020, pursuant to which, among other things, each of PSP Investments and MHR are entitled to designate three directors to the board of directors of Telesat Corporation and have the exclusive right to fill vacancies of any directorship for which it has the right to designate a director.

Voting rights and Telesat Corporation share structure

The Class A Shares and Class C Fully Voting Shares of Telesat Corporation carry 1 vote per share, and the Class B Variable Voting Shares (together, with the Class A Shares, the “Public Shares”) carry 1 vote per share; provided that any voting power of a single holder in excess of one-third of the outstanding voting power of the Telesat Corporation Shares and Telesat Partnership Units (via the Special Voting Shares) and the Golden Share Canadian Votes (see below) will effectively be transferred to the Golden Share. An issued and outstanding Class A Share will automatically be converted into a Class B Variable Voting Share if such Class A Share becomes beneficially owned or controlled, directly or indirectly, by a person who is not a Canadian (as defined in the Investment Canada Act).

The Special Voting Shares and the Golden Share have no material economic rights. The Class B and C Units of Telesat Partnership are effectively accorded 1 vote per share via the Special Voting Shares of Telesat Corporation. The Special Voting Shares are held by the trustee of a trust, entitling the Trustee to that number of votes on applicable matters on which holders of Telesat Public Shares are entitled to vote that is equal to the number of Telesat Corporation Shares into which the Telesat Partnership Units held by the holders of such Telesat Partnership Units on the applicable record date are convertible. Pursuant to the Partnership Agreement, each holder of Telesat Partnership Units has the right to direct Telesat Corporation as to how to instruct the Trustee to vote the voting power of the Special Voting Shares corresponding to such holder’s Telesat Partnership Units.

Voting power is attributed to the Golden Share in two ways. First, the Golden Share will be attributed with the number of votes required in order to ensure that the votes cast by the holders of Class A Shares and Class A Units, Class C Shares and Class C Units and the Golden Share, together, represent a simple majority of the votes cast and entitled to vote (such voting power, the “Golden Share Canadian Votes”). Second, the Golden Share will be attributed with the number of votes in excess of a Non-Canadian voting limitation.

Resulting MHR and PSP ownership and investments approvals

PSP Investments (through Red Isle) and MHR will own 36.8% and 36.4% (on a fully exchanged and converted basis) of the Telesat Corporation shares. Investor Rights Agreements generally provide that Telesat Corporation shall not propose or consent to and shall cause Telesat Partnership and Telesat Corporation’s other subsidiaries not to propose or consent to certain actions without obtaining the consent of MHR or PSP Investments, as applicable, so long as such principal shareholder and its affiliates own more than 5% of Telesat Corporation shares on a fully-diluted basis.

US tax considerations

S. 7874 inversion rules

Rules under code s. 7874 could cause Telesat Corporation or Telesat Partnership to be taxed as a U.S. corporation for U.S. federal income tax purposes (i) Telesat Corporation or Telesat Partnership acquired substantially all of the stock or assets of Loral (the “Acquisition Requirement”), (ii) following the acquisition, former shareholders of Loral own at least 80% of Telesat Corporation or Telesat Partnership by reason of their ownership of stock of Loral (the “80% Ownership Test”), (iii) the level of business activities conducted by Telesat Corporation or Telesat Partnership and its affiliates in Canada did not satisfy a certain minimum threshold level of activity (“Substantial Business Activities”), and (iv) in the case of Telesat Partnership, it is treated as a publicly traded partnership.

Opinion re non-US corporation status

Loral has received an opinion from special tax counsel that upon consummation of the Transaction, neither Telesat Corporation nor Telesat Partnership should be taxed as a U.S. corporation in light inter alia of the tests under Code s. 7874. However, such opinion does not consider current legislative proposals to lower the threshold for the 80% ownership test to 50% (or some other percentage). While Loral entered into the Transaction Agreement on November 23, 2020, it is possible that such legislative proposals, if enacted, might be applied on a retroactive basis, with no grandfather clause for transactions executed pursuant to a binding commitment entered into prior to such legislation’s enactment or in a prior tax year.

Surrogate foreign corp rules

Even if neither Telesat Corporation nor Telesat Partnership is treated as a U.S. corporation as referred to above, s. 7874 and the associated regulations contain an alternative set of rules that could result in Telesat Corporation or Telesat Partnership being treated as a “surrogate foreign corporation,” and Loral being treated as an expatriated entity, if (i) the Acquisition Requirement is satisfied, (ii) following the acquisition, former shareholders of Loral own at least 60% of Telesat Corporation or Telesat Partnership by reason of their ownership of Loral stock (the “60% Ownership Test”), (iii) Telesat Corporation or Telesat Partnership does not have Substantial Business Activities in Canada, and (iv), in the case of Telesat Partnership, it is treated as a publicly traded partnership.

Loral has received an opinion from special tax counsel that Telesat Corporation should not be treated as a surrogate foreign (and also that Telesat Partnership should neither be treated as a publicly traded partnership, nor, accordingly, a surrogate foreign corporation.) If Telesat Partnership were treated as a publicly traded partnership, it would be treated as a surrogate foreign corporation effective as of the consummation of the Transaction.

S. 351 exchange for Telesat Corporation Public Shares

The Merger, with respect to Loralstockholders who make a Telesat Corporation Election, should qualify as a non-recognition transaction described in Code s. 351 of the Code. Assuming that (as discussed above) Telesat Corporation is not treated as a U.S. corporation. s, 367(a) should apply to the exchange of Loral Common Shares for Telesat Public Shares by U.S. Holders.

S. 721 non-recognition treatment of exchange for Telesat Partnership Units

If Loral stockholders who make a Telesat Partnership Election, then the Merger, with respect to such stockholders, should qualify as a non-recognition transaction described in s. 721. In such event, a U.S. Holder that exchanges its Loral Common Shares for Telesat Partnership Units in the Merger generally should not recognize any gain or loss on such exchange, except that gain or loss would be recognized, in an amount equal to the difference, if any, between (i) the fair market value of the non-economic voting rights received in the exchange, over (ii) a pro rata portion (based on the relative values of the interests in the non-economic voting rights and Telesat Partnership Units received by such holder) of the holder’s adjusted tax basis in a pro-rata portion of each Loral Common Share exchanged for Telesat Partnership Units. The value of the non-economic voting rights established pursuant to the Trust Agreement is expected to be nominal.

Exchange of Units for Public Shares following Lock-up Period

After the expiration of the (six-month) Lock-Up Period, holders of Telesat Partnership Units may elect to exchange (and may be required to exchange) their Telesat Partnership Units for Telesat Public Shares. Such an exchange will result in the recognition of gain or loss in an amount equal to the difference, if any, between (i) the fair market value of Telesat Public Shares received, as applicable, plus the amount of the U.S. Holder’s share of Telesat Partnership’s liabilities, if any, and (ii) the U.S. Holder’s adjusted tax basis in the Telesat Partnership Units exchanged.

Canadian tax considerations

Merger

The Merger will not be a “foreign merger” for the purposes of the Tax Act. Accordingly, a Canadian holder who holds Loral Common Shares will generally realize a capital gain (or capital loss) equal to the amount by which the Canadian holder’s proceeds of disposition of the Loral Common Shares on the Merger exceed (or are less than) the aggregate of the holder’s adjusted cost base of the Loral Common Shares and any reasonable costs of disposition. The proceeds of disposition of the Loral Common Shares to a Canadian holder who receives Telesat Public Shares will be equal to the fair market value of the Telesat Public Shares received by such Canadian holder. The proceeds of disposition of the Loral Common Shares to a Canadian holder who receives Telesat Partnership Units will be equal to the aggregate of the fair market value of the Telesat Partnership Units and the non-economic voting rights received by such Canadian holder, whose value is expected to be nominal.

FAPI treatment of dividends paid by Can ULC to Loral Holdings.

Loral Holdings will be a controlled foreign affiliate of Telesat Partnership. Telesat Partnership will be required to include in its income for a year its share of the foreign accrual property income (“FAPI”) of Loral Holdings for such year, including its proportionate share of any dividends paid by Can ULC to Loral Holdings in such year. In turn, Telesat Corporation must include in income its share of the FAPI (including such dividends paid by Can ULC to Loral Holdings) of Telesat Partnership. However, if Loral Holdings and Loral each pay corresponding dividends in the same taxation year (and provided that Loral is a “foreign affiliate” of Telesat Corporation), Telesat Corporation may deduct in computing its taxable income a prescribed portion of such dividends received by it through Telesat Partnership. In determining the amount of such dividends from Loral that may be deducted in computing its taxable income, Telesat Corporation intends not to take into account any deduction claimed by Telesat Partnership pursuant to s. 91(5). Telesat Corporation believes that such interpretation is consistent with the rationale expressed by the CRA for its published administrative position in this regard.

SIFT tax rules

Telesat Partnership will be a SIFT partnership and, therefore, will be subject to SIFT tax on its “taxable non-portfolio earnings” including income, other than taxable dividends, from “non-portfolio property.” In particular, it would generally be required to pay SIFT tax if its Loral stock were non-portfolio property and the unlimited liability company (“Can ULC”) formed by Loral Holdings Corporation (“Loral Holdings”) and Telesat CanHoldco paid a dividend to Loral Holdings - but subject to any deductions that may be available to Telesat Partnership in computing the income from its Loral stock. As discussed above, provided Loral Holdings and Loral each pay corresponding dividends in the same taxation year as any dividend paid by Can ULC, it is anticipated the Telesat Partnership will be able to claim sufficient deductions so that it does not have net income from non-portfolio property.

Canadian withholding on Telesat CanHoldco dividends

Telesat Partnership will not be a “Canadian partnership.” However, in determining the rate of Canadian federal withholding tax applicable to dividends paid by Telesat CanHoldco to Telesat Partnership, Telesat Corporation, as general partner, expects Telesat CanHoldco to look through Telesat Partnership to its partners and, having regard to the CRA’s administrative practice in similar circumstances, not to withhold on that portion of a dividend attributable to Canadian resident partners of Telesat Partnership (including Telesat Corporation) and to take into account any reduced rates of Canadian federal withholding tax to which non-Canadian limited partners may be entitled under an applicable treaty.

FTCG rules

The foreign tax credit generator rules are not expected to apply to Telesat Partnership.