Inter Pipeline

Overview

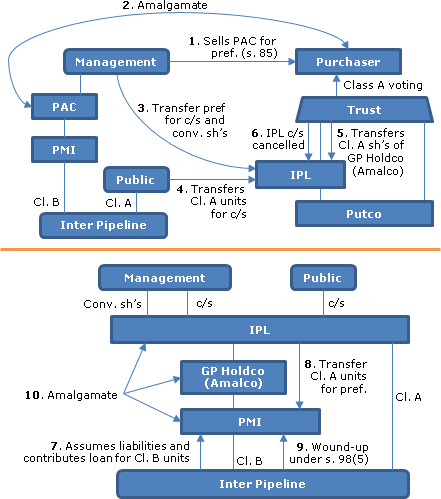

At the beginning of June 2013, the obligation of Inter Pipeline to pay management and incentive fees to its general partner (Pipeline Management Inc., or "PMI") was effectively eliminated by the management shareholders of the sole shareholder of PMI (Pipeline Assets Corporation, or "PAC") transferring their common shares of PAC on a rollover basis to a purchasing corporation (the "Purchaser"). The Purchaser was controlled by the independent directors of PMI in their capacity of trustees of a shareholder trust (the "Trust"), but was 99.999% owned by Inter Pipeline as a non-voting shareholder. The consideration paid was the issuance of preferred shares with a redemption amount of $340 million or $240 million, depending on when two Inter Pipeline projects came into production. The conversion (the "Conversion") of Inter Pipeline into a corporation under a proposed Alberta Plan of Arrangement will be accomplished by its being wound-up under s. 98(6) into PMI, with PMI then being amalgamated with other corporations in the group, and with management's preferred shares being converted, or being convertible, into common shares of the amalgamated corporation ("New Inter Pipeline").

Inter Pipeline

Inter Pipeline is an Alberta LP whose Class A Units trade on the TSX. PMI holds Class B units representing its general partner interest. Inter Pipeline owns and operates a major energy infrastructure business. It became subject to tax under the SIFT rules effective January 1, 2011.

Management internalization transactions

In order to effectively eliminate management fees payable to its general partner (PMI), on June 1, 2013 Inter Pipeline indirectly purchased PMI. In particular:

- the Trust was settled with charitable beneficiaries and its trustees were the independent directors of PMI

- the Trust incorporated Inter Pipelines Ltd. ("IPL")

- 1740974 Alberta Ltd. ("Putco") was incorporated, with each of the Trust and IPL holding 50% of its shares

- following the incorporation of the Purchaser, all its Class A Voting Shares were held by the Trust, and all of its Class B Non-Voting Common Shares of the Purchaser (representing a 99.999% equity interest) were held by Inter Pipeline

- Pipeline Assets Corporation ("PAC"), which was the sole shareholder of PMI and whose shareholders were four managers of PMI and a family holding company of the Chairman, was sold by those shareholders to the Purchaser pursuant to a share purchase agreement

- under the share purchase agreement, the Purchaser issued Preferred Shares to the vendors comprising Class A Preferred Shares having a redemption amount of $170 million and Class B Preferred Shares with a redemption amount of $170 million provided that the redemption amount of each Class B Preferred Share was multiplied by 70/170 (i.e., reducing the aggregate redemption amount to $70 million) if the "Trigger Date" had not occurred by January 1, 2017, i.e., both the Foster Creek and Christina Lake projects were not yet producing revenue

- each such Preferred Shares also: was entitled to receive cash dividends equal to the cash distributions on a Class A Unit of Inter Pipeline; was puttable for its fair market value to Putco; had a redemption and retraction amount equal to the current market price of a Class A Unit of Inter Pipeline plus unpaid distributions (subject, in the case of a Class B Preferred Share, to being multiplied by 70/170 as per above); was retractable on the first to occur of various specified dates including January 1, 2014 (in the case of the Class A Preferred Shares) or the first to occur of the Trigger Date and January 1, 2017 (in the case of the Class B Preferred Shares), and was redeemable on June 1, 2038 (or earlier on certain events)

- the Purchaser agreed that at the request of any vendor it would execute a joint s. 85(1) election form

- the Purchaser and PAC then amalgamated, with the Preferred Shares of the vendors becoming Preferred Shares of Amalco ("GP Holdco") having 32% of the total votes, with the Trust owning all of the Class A Voting Shares of GP Holdco representing a controlling 68% voting interest and with Inter Pipeline holding all the Class B Non-Voting Common Shares

Plan of Arrangement

Under the Plan of Arrangement:

- IPL will exercise a call option and acquire the one issued and outstanding voting share of Putco owned by the Trust

- each outstanding Class A Preferred Share (or Class B Preferred Share) of GP Holdco will be transferred to IPL in exchange for one Common Share (or one Convertible Share) of IPL; each Convertible Share will be automatically converted into one Common Share on the Trigger Date, or into 70/170 of a Common Share if January 1, 2017 occurs first

- each outstanding Class A unit of Inter Pipeline will be transferred to IPL in exchange for one Common Share of IPL

- the Trust will transfer its Class A Voting Shares of GP Holdco to IPL for cash consideration

- the one issued and outstanding Common Share of IPL owned by the Trust will be transferred by it to IPL for cash consideration equal to its market value

- PMI will assume all obligations of Inter Pipeline, and contribute to PMI a loan of $288.6 million owing by Inter Pipeline to PMI, in consideration for the issuance of Class B Units of Inter Pipeline

- IPL will transfer all of its Class A Units of Inter Pipeline to PMI in consideration for preferred shares of PMI with an aggregate redemption amount equal to the fair market value of the transferred units

- accordingly, Inter Pipeline will be wound-up by operation of law into PMI

- an amended DRIP will become effective

- outstanding deferred unit rights will be amended to refer to IPL

- IPL, GP Holdco, PMI and Putco will amalgamate, with the authorized capital of the amalgamated corporation (New Inter Pipeline) consisting of Preferred Shares and Common Shares, with each outstanding Common Share and Convertible Share of IPL being converted into one Common Share or Convertible Share, as the case may be, of New Inter Pipeline and with each issued and outstanding share in the capital of GP Holdco, PMI and Putco being cancelled

Canadian tax consequences

S. 85. The exchange of Class A Units for Common Shares will occur on a taxable basis unless a s. 85 election is made with IPL. The election must be provided to IPL on or before the 90th day following the effective date of the Arrangement. Amalgamation. A shareholder will not realize a capital gain or loss as a result of the amalgamation of IPL.