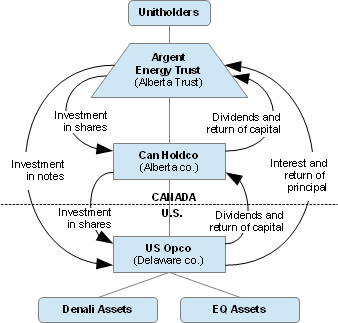

Argent

A TSX-listed mutual fund trust ("Trust"), through a Canadian Holdco, will hold a US Opco which will carry on a US oil and gas business. Structure is similar to Eagle Energy, except that the US energy business is held through a Canadian holding corporation holding a US operating company rather than a Canadian sub trust holding a Delaware LP.

Canadian Tax

The Trust is not contemplated to be subject to SIFT tax on the basis that Can Holdco is a portfolio investment entity.

Based on the nature of the activities of US Opco and on it maintaining its central management and control in the US, its earnings are expected to give rise to exempt surplus rather than taxable surplus, so that dividends from US Opco can be received free of Canadian tax. It is expected that Can Holdco will designate the dividends paid by it as eligible dividends.

US Tax

US Opco anticipates that it will be entitled to deduct interest payments on the notes held by Trust, based inter alia on the CT Notes being treated as debt and satisfying the earnings stripping rules in s. 163(j). In particular, s. 163(j) requires that US Opco's debt-to-equity ratio be no more than 1.5:1, and that US Opco's "net interest expense" (interest expense minus interest income) be no more than 50% of its "adjusted taxable income" (taxable income before the deduction of certain items, including net interest expense). US Opco expects to have an initial debt-to-equity ratio of 1.6:1, so its deductions will be initially limited. The interest payments are expected to be exempt from US withholding tax, in accordance with the Treaty.

Risk Factors

- In the event that Can Holdco is found to be a Canadian-controlled private corporation and it makes excessive eligible dividend designations, it could be subject to penalty tax.

- If the units were found to be financing transactions under US Treasury regulations, then the US Opco notes and units together would likely be a financing arrangement under US conduit financing rules. Unit holders would have to provide a Tax Certification or else the notes would be subject to US withholding tax.

- As the Trust does not expect to hold taxable Canadian property, it will not be subject to the non-resident ownership restrictions in s. 132(7).

- As the Trust does not derive income from real property in Canada, Canadian resource property, or timber resource property, Part XIII.2 withholding tax will not apply.

Article

Brian Kearl and Eugene Friess, "Will Cross-border Income Trusts Be Next in the Department of Finanace's Cross-hairs?" Internation Tax Planning, Vol XVII, No. 4, p. 1204: In comparing the Eagle Energy trust-on-trust-on-LP structure to the Argent Energy trust-on-Canco-on-US Opco structure, they state (p. 1208):

...it is understood through discussions with U.S. counsel that using a U.S. Opco as opposed to a U.S. LP to carry on the U.S. business may be preferred in order to, inter alia, attract U.S. institutional investment and acquire U.S. federal oil and gas leases.