Starlight Multi-Family (No. 1) Value-Add -- summary under Asset Purchases

Overview

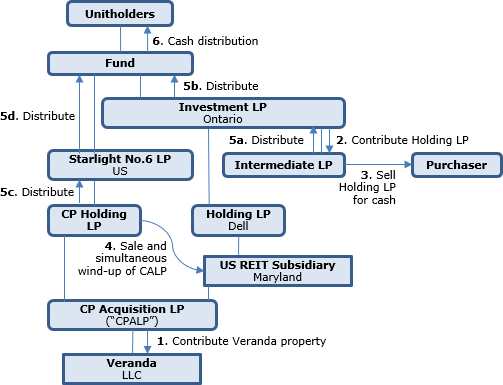

As targeted on its formation three years’ previously, the Fund indirectly sold three US rental properties at a gain after having increased the rents. In order to avoid the realization of foreign accrual property income gains, and instead realize (non-FAPI) capital gains that could be integrated with capital gains treatment to the Fund unitholders, the gains were not realized within the corporate subsidiary (a US private REIT) and instead were realized on internal transfers by subsidiary LPs. In order to get the proper basis adjustments for the distribution of such capital gains, various tiers of partnerships were wound-up on a bottom-up basis as a part of the distribution of proceeds, and with the net sales proceeds ultimately distributed in redemption of the Fund units.

FIRPTA was recognized on the gains on the sales.

Fund

The Fund is an Ontario LP that was established as a “closed-end” limited term fund in June 2017 to indirectly acquire income-producing multifamily properties that could achieve significant increases in rental rates as a result of undertaking high return, light value-add capital expenditures and active asset management, with the goal of ultimately directly or indirectly disposing of its interests in the assets by the end of the term of the Fund. The time horizon for the Fund was intended to be three years, with the initial term scheduled to expire in June 2020, and with two one-year extensions available subject to approval of the Fund GP. The Class A Units and Class U Units of the Fund are currently listed on the TSX-V. Daniel Drimmer beneficially owns 30.82% of the Class C Units, representing a 6.13% voting interest in the Fund.

Fund GP

Starlight U.S. Multi-Family (No. 1) Value-Add GP, Inc., an Ontario corporation owned by the Manager and holding a 0.01% general partner interest in the Fund.

Investment LP

Starlight U.S. Multi-Family (No. 1) Value-Add Investment L.P., an Ontario LP of which the Fund is the 99.99% limited partner and a wholly-owned Ontario subsidiary of the Fund is the general partner having a 0.01% general partner interest and a carried interest.

Intermediate LP

A Delaware LP to be formed prior to the closing whose sole limited partner will be Investment LP.

Holding LP

Starlight U.S. Multi-Family (No. 1) Value-Add Holding L.P., a Delaware LP of which Investment LP is the 99.99% limited partner and the general partner is a Delaware partnership (as to which the Manager is an indirect 80% owner) having a 0.01% general partner interest plus a carry.

U.S. REIT Subsidiary

Starlight U.S. Multi-Family (No. 1) Value-Add Fund REIT Inc. a Maryland liability company that (with the exception of preferred shares held by outside investors) is wholly-owned by Holding LP and which, through subsidiary LLCs holds multi-unit rental properties in the southern U.S.

Starlight Investments Acquisition (No.6) Partnership

An LP whose limited partner is the Fund.

CP Holding LP

Coventry Pointe Multi-Family Holding LP, whose limited partner is Starlight Investments Acquisition (No.6) Partnership

CP Acquisition LP

Coventry Pointe Acquisition LP, held by CP Holding LP and U.S. REIT Subsidiary (as limited partners) and by "CP Acquisition GP LLC" (as general partner) CP Acquisition LP holds the Veranda property.

Veranda Property LLC

A Delaware LLC to be formed as a wholly-owned subsidiary of CP Acquisition LP.

Manager

Starlight Group Property Holdings Inc.

Value of Transaction

The Transaction is valued at approximately US$239,600,000 and includes gross cash consideration of approximately US$92,100,000 payable to the Fund, with the Purchaser also indirectly assuming all of the Fund’s existing debt in the amount of approximately US$147,500,000. In connection with the Transaction, unitholders will be entitled to receive a distribution per Unit in the following amounts:

|

Class of Units1 |

Pre-U.S. Tax |

Pre-U.S. Tax IRR |

Post U.S. Tax |

|

Class A |

C$12.35 |

16.9% |

C$11.31 |

|

Class C |

C$13.11 |

16.8% |

C$12.02 |

|

Class D |

C$12.35 |

16.9% |

C$11.31 |

|

Class E |

US$12.38 |

17.0% |

US$11.34 |

|

Class F |

C$12.79 |

16.8% |

C$11.72 |

|

Class U |

US$12.38 |

17.0% |

US$11.34 |

The net proceeds of the Transaction, after applicable U.S. taxes are paid, will be distributed to Unitholders as part of the cancellation of all issued and outstanding Units and dissolution of the Fund. Any U.S. taxes paid from the Fund’s proceeds of disposition are generally expected to be recognized as having been paid by the Unitholders for purposes of the foreign tax credit and foreign tax deduction rules in the Tax Act.

Periodic distributions

Under the Acquisition Agreement, Unitholders of the Fund are permitted to receive monthly Permitted Fund Distributions in an amount not to exceed (i) C$0.05000 per Unit in respect of each of the Class A Units, Class C Units, Class D Units and Class F Units, and (ii) US$0.05000 per Unit in respect of each of the Class E Units and Class U Units, in each case consistent with past practice. Assuming the Closing occurs in early January 2020, the Fund GP Board currently intends that its previously announced monthly distribution, in respect of November 2019 and payable on December 16, 2019, will be the Fund’s final regular monthly distribution.

Pre-closing transaction steps

Prior to Closing:

- CP Acquisition LP will transfer the Veranda Property to Veranda Property LLC in consideration for the assumption by Veranda Property LLC of the Veranda Property liabilities and additional membership interests in Veranda Property LLC; and

- Investment LP also will transfer the Holding LP Interest to Intermediate LP in consideration for additional limited partnership interests in Intermediate LP;

Closing steps

- Intermediate LP will transfer to the Purchaser the limited partner interest in Holding LP Interest (the “Holding LP Interest”) for cash consideration equal to the Fund value minus the less the CP sale proceeds described below and the carried interest entitlement of the GP of Holding LP;

- CP Holding LP will transfer 50% of the membership interest in CP Acquisition GP LLC to the U.S. REIT Subsidiary for cash consideration of U.S.$39K; and

- CP Holding LP will transfer the limited partner interest in CP Acquisition LP (the “CP Acquisition LP Interest”) to the U.S. REIT Subsidiary for cash consideration of U.S.$7.8M; and simultaneously, the Purchaser will cause CP Acquisition GP LLC to distribute its GP interest in CP Acquisition LP to the U.S. REIT Subsidiary such that all of the partnership interests in CP Acquisition LP will be held by the U.S. REIT Subsidiary and the LP will thus be terminated;

- The Fund will cause the applicable Fund Entities to distribute the proceeds from the sale, net of applicable U.S. taxes, to the Fund, which it will use along with any other available cash after applicable U.S. taxes, for an estimated total of US$81.8M to pay a distribution to all of the Unitholders, cancel all issued and outstanding Units and dissolve the Fund and its remaining subsidiaries.

REIT opinion

The Purchaser is not required to complete the Transaction unless the Fund has delivered to the Purchaser an opinion of Clark Hill PLC regarding the U.S. REIT Subsidiary’s organization and operation in conformity with the requirements for qualification and taxation as a real estate investment trust pursuant to ss.856 and 857 of the Code throughout the period up to the Closing.

Canadian tax considerations

Veranda transfer

Any recapture of depreciation or capital gain realized by CP Acquisition LP in respect of the transfer by CP Acquisition LP of the transfer of the Veranda property to Veranda LLC will be allocated to CP Holding LP, the U.S. REIT Subsidiary and CP Acquisition GP LLC in accordance with the partnership agreement governing CP Acquisition LP.

The U.S. REIT Subsidiary is a “controlled foreign affiliate” (“CFA”) of Holding LP. Accordingly, to the extent that the U.S. REIT Subsidiary earns “foreign accrual property income” (“FAPI”), the amount of such FAPI allocable to the Holding LP must be included in computing the income of the Holding LP for the fiscal period of the Holding LP in which the taxation year of the CFA ends. Dividends received by Holding LP from the U.S. REIT Subsidiary will be included in computing its income; however, a deduction generally will be available to the extent that Holding LP has included such amount in its income as FAPI. Any allocation of recapture income or capital gain by CP Acquisition LP to the U.S. REIT Subsidiary as a consequence of the Veranda property transfer is not expected to result in any material amount of FAPI being recognized by Holding LP.

Similarly, Veranda LLC will be a CFA of CP Acquisition LP, until CP Acquisition LP ceases to exist. Accordingly, any FAPI of Veranda LLC allocable to CP Acquisition LP must be included in computing the income of CP Acquisition LP for the fiscal period of CP Acquisition LP in which the taxation year of Veranda LLC ends.

Holding LP interest transfer

Any capital gain (or capital loss) realized by Investment LP in respect of the transfer of the LP interest in Holding LP by Investment LP to Intermediate LP will be allocated to the Fund and the general partner of Investment LP.

Distribution of refinancing proceeds

Because the purchase price to be paid by the Purchaser for the transfer to it of the Holding LP interest pursuant will be reduced by any refinancing proceeds distributed by Holding LP prior to closing, the reduction in the adjusted cost base of Investment LP’s partnership interest in Holding LP as a consequence of such distribution is not expected to change the capital gain realized respecting such disposition of the Holding LP interest.

Sales of Holding LP and CP Acquisition GP LLC interests

Intermediate LP and CP Holding LP will respectively realize a capital gain or loss on the sale of the Holding LP interest to the Purchaser, and on the sale of an interest in CP Acquisition GP LLC to the U.S. REIT Subsidiary (which will be owned by the Purchaser at the time of such sale).

Winding-up of CP Acquisition LP

As a result of the termination of CP Acquisition LP occurring as a result of the acquisition of the remaining interests in CP Acquisition LP by the U.S. REIT Subsidiary, the fiscal period of CP Acquisition LP will be deemed to end and CP Holding LP’s adjusted cost base in the CP Acquisition LP Interest at the time of sale will reflect CP Holding LP’s share of any income (including capital gains) or loss realized by CP Acquisition LP in that fiscal period prior to the sale sequence of the Veranda Transfer as described above. Any such capital gain realized by Intermediate LP or CP Holding LP will be allocated to its members.

Bottom-up dissolutions

Following the above sale transactions by them, Intermediate LP and CP Holding LP (collectively the “Lower Tier Subsidiary Partnerships”) will be dissolved, with the net sale proceeds of such sales distributed to Investment LP (in the case of Intermediate LP) and Starlight Investments Acquisition (No.6) Partnership (in the case of CP Holding LP) (collectively, the “Upper Tier Subsidiary Partnerships”), and where applicable to their respective general partners. In turn, it is expected that each Upper Tier Subsidiary Partnership will dissolve and distribute the proceeds received from the dissolution of the applicable Lower Tier Subsidiary Partnership to the Fund and its respective general partner. The fiscal period of each Lower Tier Subsidiary Partnership and each Upper Tier Subsidiary Partnership will be deemed to end prior to the time at which such partnership ceases to exist as a consequence of such dissolutions.

Dispositions by partners on dissolutions

The partners of each such dissolving Partnership (including the Upper Tier Subsidiary Partnerships, in the case of the dissolution of the Lower Tier Subsidiary Partnerships, and the Fund, in the case of the dissolution of the Upper Tier Subsidiary Partnerships) will be considered to dispose of their interests in the dissolving Partnership for proceeds of disposition equal to the amount of cash plus the fair market value of any other property distributed to them by the dissolving Partnership on the dissolution. Each of the Upper Tier Subsidiary Partnerships and the Fund will realize a capital gain (or capital loss) to the extent that such proceeds, net of reasonable costs of disposition, exceed (or are less than) its adjusted cost base of its interest in the applicable dissolving Partnership, taking into account any adjustments in respect of income (including capital gains) or loss allocated to it by the dissolving partnership for its fiscal period that is deemed to end as a consequence of the dissolution as described above.

Foreign tax credits

In general, a Holder will only be entitled to claim a foreign tax credit in respect of U.S. taxes paid by the Fund and the Subsidiary Partnerships in respect of the Transaction to the extent it has borne the economic burden of such taxes. For these purposes, U.S. taxes paid by a Subsidiary Partnership should generally be considered to have been borne by a particular Holder to the extent of the Holder’s share of such tax as determined in accordance with the Limited Partnership Agreement.

A Holder’s ability to apply U.S. taxes in the foregoing manner may be affected where the Holder does not have sufficient taxes otherwise payable under Part I of the Tax Act or sufficient U.S. source income in the taxation year in which the U.S. taxes are paid, or where the Holder has other U.S. source income or losses, has paid other U.S. taxes or, in certain circumstances, has not filed a U.S. federal income tax return where required for the relevant taxation year. Although the foreign tax credit provisions are designed to avoid double taxation, the maximum credit is limited.

US tax considerations

No FIRPTA implications to dispositions of interests in Canadian partnerships

The Fund primarily own interests in Canadian partnerships that have elected to be treated as corporations for U.S. federal income tax purposes (e.g. the Investment LP). The interests in such Canadian partnerships (that are treated as corporations for U.S. federal income tax purposes) should not be treated as USRPIs because these Canadian partnerships should not be treated as U.S. corporations as they were not created or organized under the laws of the U.S. Since Non-U.S. Unitholders would not be directly or indirectly disposing of any USRPIs pursuant to the Transaction, any gain realized by such Non-U.S. Unitholders should not be subject to U.S. federal income tax.

Disposition of USRPIs by deemed US corporations

The Investment LP and Starlight Investments Acquisition (No.6) Partnership are treated as corporations for U.S. federal income tax purposes. As a result of the transaction, each such partnership will be considered to dispose of a USRPI. Any gain realized from such a disposition will be treated as if it were effectively connected with a U.S. trade or business and each partnership will be subject to U.S. corporate tax on any recognized gain.