Loblaw/GWL/Choice -- summary under Butterfly spin-offs

Overview

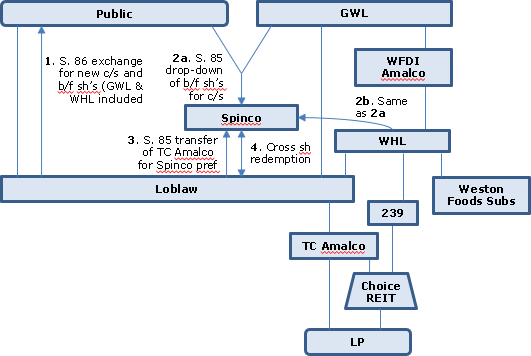

Loblaw has a substantial real estate rental portfolio (much of it being stores rented to it plus the former CREIT portfolio) held through Choice REIT. Loblaw will be effecting a butterfly spin-off of its Choice holdings to its parent, George Weston Limited (also TSX-listed) pursuant to a CBCA Plan of Arrangement, subject to receiving CRA rulings. This is to be accomplished by first butterflying the Choice holdings to a “Spinco” held by the Loblaw shareholders including GWL and an indirect GWL subsidiary (WHL). WHL, which apparently also indirectly holds the Weston Foods division, would then effect a butterfly distribution of its Spinco shares to a second transferee corporation (WHL/TC). There then would be a triangular amalgamation of Spinco with inter alia WHL/TC pursuant to which the public shareholders of Spinco would receive GWL common shares in exchange for their Spinco common shares.

In order to effect the initial spin-off to Spinco, there will be a s. 86 exchange of old Loblaw common shares for new Loblaw common shares and Loblaw butterfly shares. In order to reflect the FMV reduction of a Loblaw common share, the existing Loblaw stock options will be exchanged for a higher number of new options with a lower exercise price but an aggregate in-the-money value that is no higher. The in the money amount of the new and old options will be determined based on the weighted average TSX trading price of the Loblaw shares for the five-day trading period beginning on the Effective Date of the Arrangement, and ending immediately before the Effective Date, respectively.

Loblaw/Choice REIT

Loblaw is one of Canada’s largest grocery, pharmacy and health and beauty retailers and is a leading provider of apparel and general merchandise. Its common shares (the “LCL Shares”) are listed on the TSX. Currently, Loblaw holds an approximate 61.6% effective interest in Choice REIT through its indirect ownership of 21,500,000 “Trust Units” of Choice REIT and 389,961,783 (exchangeable) Class B LP Units (of a subsidiary LP of Choice REIT), representing all of the outstanding Class B LP Units.

TC Amalco

A CBCA corporation that will hold the interest in Choice REIT referred to above, namely, the Class B Units (and related Special Voting Units) and Trust Units.

GWL

George Weston Limited, which is TSX-listed, is the majority owner of Loblaw GWL has two reportable operating segments: Weston Foods and Loblaw. 93% of its market capitalization is accounted for by its interest in Loblaw.

Background to choice of butterfly

Management determined that a pro rata spin-out to all shareholders would be the best strategic alternative and would be financially attractive but also determined that spinning out or distributing Loblaw’s interest in Choice REIT directly to LCL Shareholders could not be accomplished on a tax-efficient basis. If Loblaw were to have spun out its Choice REIT interest in a direct distribution to all LCL Shareholders, it would have triggered an amount of tax payable by Loblaw that today would be approximately $640 million. To address this impediment, management and its advisors developed a spin-out structure that would involve distributing the Choice REIT interest to GWL and providing LCL Shareholders other than GWL and its subsidiaries with the equivalent market value of their pro rata interest in Choice REIT in the form of GWL Common Shares. In this structure, the Choice REIT interest and the GWL Common Shares would be distributed at FMV based on their respective trading prices at the time of the spin-out.

Consequences of Arrangement

Under the Arrangement, LCL Shareholders other than GWL and its subsidiaries will receive 0.135 of a GWL Common Share (26.7 million GWL Common Shares in total) for each LCL Common Share held and GWL will receive Loblaw’s approximate 61.6% effective interest in Choice REIT. Following the Arrangement, GWL will own an approximate 65.4% effective interest in Choice REIT directly (which includes the approximate 3.8% effective interest in Choice REIT currently owned by wholly-owned, direct subsidiaries of GWL prior to the Arrangement), and GWL will continue to be controlled by Mr. W. Galen Weston who, directly and indirectly through entities which he controls, will own approximately 52.8% of the outstanding GWL Common Shares. The public shareholders of Loblaw will own approximately 16.8% of the outstanding GWL Common Shares as a result of the Arrangement and Loblaw will have no ownership in Choice REIT. GWL’s market capitalization is expected to increase from approximately $13.0 billion to $15.7 billion, and its public float of GWL Common Shares is expected to increase from approximately $4.6 billion to $7.3 billion.

Pre-Arrangement Transactions

Under the Pre-Arrangement Transactions: (i) Loblaw and its applicable subsidiaries will undertake various reorganizations to ensure that the Trust Units and Class B LP Units representing LCL’s approximate 61.6% effective interest in Choice REIT are held by TC Amalco prior to the Effective Time, and (ii) GWL and its applicable subsidiaries will undertake various reorganizations to ensure that the Trust Units representing GWL’s approximate 3.8% effective interest in Choice REIT are held by WFDI Amalco prior to the Effective Time.

Plan of Arrangement

- Each LCL Shareholder will exchange each of its LCL Common Shares for one LCL New Common Share and one LCL Spin-off Butterfly Share (the “LCL Capital Reorganization”). The aggregate PUC of the LLC Common Shares will be allocated between the LCL New Common Shares and the LCL Spin-off Butterfly Shares on a relative FMV basis.

- Concurrently with the LCL Capital Reorganization, and in order to reflect the FMV reduction of an LCL Common Share, each holder of LCL Stock Options will exchange all of such holder’s outstanding LCL Stock Options for a number of LCL New Stock Options with an aggregate in-the-money value that is no higher. The in the money amount of the new and old options will be determined based on the weighted average TSX trading price of LCL Common Shares for the five-day trading period beginning on the Effective Dates, and ending immediately before the Effective Date, respectively.

- The number of LCL DSUs, PSUs and RSUs will be proportionately increased to reflect such FMV reduction.

- Each holder of LCL Spin-off Butterfly Shares will transfer each LCL Spin-off Butterfly Share that it owns to Spinco in exchange for one Spinco Common Share (the “Spinco Share Exchange”).

- Loblaw will transfer the LCL Spin-off Distribution Property (namely, its TC Amalco Common Shares) to Spinco for 1,000,000 Spinco Preferred Shares, electing under s. 85(1).The net FMV of such property will accord with the s. 55(1) “distribution” fraction.

- Spinco will redeem all of the Spinco Preferred Shares held by Loblaw for the Spinco Redemption Note, with any deemed dividend designated by Spinco as an eligible dividend.

- The first taxation year of Spinco will end.

- Loblaw will redeem the LCL Spin-off Butterfly Shares held by Spinco for the LCL Redemption Note.

- Loblaw will satisfy its obligations under the LCL Redemption Note by transferring the Spinco Redemption Note to Spinco.

- Spinco will satisfy its obligations under the Spinco Redemption Note by transferring the LCL Redemption Note to Loblaw.

- Each LCL New Common Share will be converted into one LCL Common Share.

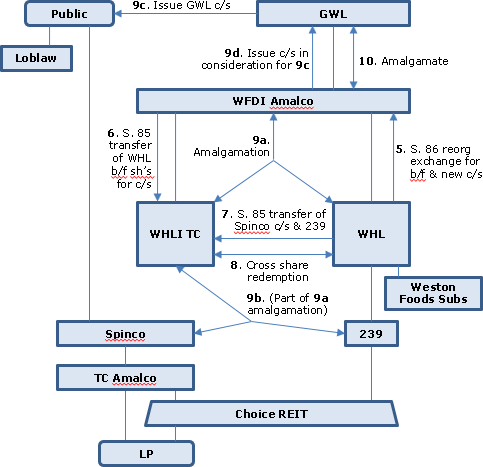

- WFIC Sub will transfer all of the LCL Common Shares that it owns to WFIC Sub Holdco for 10,000 common shares of WFIC Sub Holdco, electing under s. 85(1) – and similarly for LCL Common Share drop-downs by Rocky to Rocky Holdco, and by Rocky Sub to Rocky Sub Holdco.

- WFDI Amalco will exchange each WHL Common Share that it owns for one WHL New Common Share and one WHL Spin-off Butterfly Share.

- WFDI Amalco will transfer all of the WHL Spin-off Butterfly Shares that it owns to WHL/TC for 10,000 WHL/TC Common Shares, electing under s. 85(1).

- WHL will transfer the WHL Spin-Off Distribution Property (being all the common shares in 2397454, and the WHL’s Spinco Common Shares to WHL/TC for 1,000,000 WHL/TC Preferred Shares, electing under s. 85(1).

- The net FMV of the WHL Spin-off Distribution Property received by WHL/TC will approximate the s. 55(1) “distribution” fraction.

- WHL/TC will redeem all of the WHL/TC Preferred Shares held by WHL for the WHL/TC Redemption Note.

- The first taxation year of WHL/TC will end.

- WHL will redeem all of the WHL Spin-off Butterfly Shares held by WHL/TC for the WHL Redemption Note.

- WHL will satisfy its obligations under the WHL Redemption Note by transferring the WHL/TC Redemption Note to WHL/TC.

- WHL/TC will satisfy its obligations under the WHL/TC Redemption Note by transferring the WHL Redemption Note to WHL.

- WFDI Amalco by exercising its conversion right will have each WHL New Common Share converted into one WHL Common Share.

- WFDI Amalco, WHL/TC, 2397454 (assumed in the diagram to be a holding company for Choice REIT holdings of WHL, although this is not disclosed) , Rocky, Rocky Sub, WFIC Sub, Spinco and TC Amalco will amalgamate to form Spinco Amalco, with each issued and outstanding common share of WFDI Amalco being converted into one Spinco Amalco Common Share, each issued and outstanding Spinco Common Share (other than a Spinco Common Share held by a predecessor corporation) being cancelled, and in consideration therefor, GWL will issue to each such holder of Spinco Common Shares a number of GWL Common Shares per Spinco Common Share equal to the Spinco/GWL Conversion Ratio.

- As consideration for the issuance of GWL Common Shares, Spinco Amalco will issue 1,000,000 Spinco Amalco Preferred Shares to GWL. The stated capital of the Spinco Amalco Common Shares, and the stated capital of the Spinco Amalco Preferred Shares, will be an amount equal to $0.01 and the amount to be added by GWL to the stated capital of the GWL Common Shares will be an amount equal to the PUC of the Spinco Common Shares.

- GWL and Spinco Amalco will amalgamate, and the issued and outstanding GWL Common Shares and GWL Preferred Shares immediately prior to the amalgamation will survive and continue to be GWL Common Shares and GWL Preferred Shares.

- As part of the Arrangement, GWL expects to issue 1,296,000 GWL Common Shares to a third party for a cash subscription price per GWL Common Share equal to the effective price being used for the GWL Common Shares being issued to LCL Shareholders in the Arrangement.

Due Bill Trading

Due Bill trading may only be used in connection with a “push-out” of listed securities (i.e. where the certificates representing the originally listed securities to which the entitlement attaches will not be replaced with new certificates; rather, only the entitlement (e.g. the dividend, shares of a new company, etc.) will be “pushed-out” to shareholders). In the case of the Arrangement, this means that Due Bill trading will only be used in connection with the LCL Common Shares, as the certificates representing the LCL Common Shares will not be replaced with new certificates. Any LCL Common Shares traded during the Due Bill Period will have Due Bills attached and will therefore carry the right to receive GWL Common Shares.

Canadian tax consequences to LCL shareholders

Loblaw s. 86 reorg

Each Resident Shareholder will exchange each of its LCL Common Shares for one LCL New Common Share and one LCL Spin-off Butterfly Share. A Resident Shareholder will not realize a capital gain or a capital loss as a result of such exchange. The aggregate ACB of a Resident Shareholder’s LCL Common Shares immediately before such exchange will be allocated among the LCL New Common Shares and LCL Spin-off Butterfly Shares received by the Resident Shareholder on the exchange in proportion to the relative FMV of such shares.

Spinco Share Exchange

Pursuant to the Spinco Share Exchange, each Resident Shareholder will transfer each of its LCL Spin-off Butterfly Shares to Spinco in exchange for one Spinco Common Share. Subject to such shareholder reporting otherwise, a Resident Shareholder will be deemed under s.85.1 to have disposed of all of its LCL Spin-off Butterfly Shares for proceeds of disposition equal to the aggregate ACB of such shares.

Conversion

The conversion of each LCL New Common Share held by a Resident Shareholder into one LCL Common Share will be deemed not to be a disposition.

Spinco Amalgamation

The amalgamation of WFDI Amalco, Spinco, TC Amalco, WHL/TC, 2397454, Rocky, Rocky Sub and WFIC Sub to form Spinco Amalco will occur on a s. 87(4) rollover basis. Resident Shareholders will receive 0.135 of a GWL Common Share in exchange for each Spinco Common Share held immediately before the amalgamation. A Resident Shareholder who receives only GWL Common Shares on the amalgamation will be deemed to have disposed of its Spinco Common Shares for proceeds of disposition equal to their aggregate ACB.

GWL/Spinco Amalco amalgamation

GWL and Spinco Amalco will amalgamate, and on the amalgamation, each GWL Common Share held by a Resident Shareholder will survive and continue to be one GWL Common Share of the amalgamated corporation. A Resident Shareholder will be deemed to have disposed of its GWL Common Shares for proceeds of disposition equal to the Resident Shareholder’s aggregate ACB of such shares immediately before the amalgamation.

Advance income tax ruling

The Tax Ruling Application was submitted to the CRA in September 2017. The Tax Ruling requested from the CRA requires, among other things, that the LCL Spin-off Butterfly complies with all of the requirements of the public company “butterfly reorganization” rules in s.55 of the Tax Act. Itis also expected to confirm that the Pre-Arrangement Transactions will generally occur on a tax-deferred basis for Loblaw, GWL and their applicable subsidiaries and affiliates.

Potential loss of butterfly treatment

Under s. 55 of the Tax Act, Loblaw and Spinco will recognize a taxable gain on the transfer by Loblaw of the LCL Spin-off Distribution Property as part of the LCL Spin-off Butterfly if: (i) within three years of the transfer, Spinco (or GWL, as the successor of Spinco) engages in a subsequent spin-off or split-up transaction under s.55 or Loblaw engages in a split-up (but not a spin-off) transaction under s. 55; (ii) a “specified shareholder” disposes of shares of Loblaw or Spinco (or GWL, as the successor of Spinco), or property that derives 10% or more of its value from such shares or property substituted therefor, to an unrelated person or a partnership as part of the series of transactions which includes the LCL Spin-off Butterfly; (iii) there is an acquisition of control of Loblaw or of Spinco (or of GWL, as the successor to Spinco) that is part of the series of transactions that includes the LCL Spin-off Butterfly; or (vi) certain persons acquire shares in the capital of Loblaw (other than in specified permitted transactions) in contemplation of, and as part of the series of transactions that includes, the LCL Spin-off Butterfly. If any of the above events occurred and caused the LCL Spin-off Butterfly to be taxable to Loblaw and Spinco under s.55, each of Loblaw and Spinco (and GWL, as the successor of Spinco), would be liable for a substantial amount of tax.

U.S. tax consequences

Taxable distribution characterization

A U.S. Holder who receives GWL Common Shares pursuant to the Arrangement should be treated as receiving a taxable distribution in an amount equal to the FMV of the gross amount of GWL Common Shares received by such holder, without reduction for Canadian withholding tax, if any, plus the amount of cash received in lieu of fractional GWL Common Shares, although the matter is not entirely free from doubt. Such taxable distribution would be treated as a dividend, taxable as ordinary income, to the extent of a U.S. Holder’s share of the current and accumulated earnings and profits of the Company. The amount of the dividend received by a non-corporate U.S. Holder, including an individual, generally would be “qualified dividend income” subject to U.S. tax at preferential rates, provided the Company is treated as a “qualified foreign corporation” under the Code and certain holding period and other requirements are met. A qualified foreign corporation includes a non-U.S. corporation that is eligible for the benefits of a comprehensive income tax treaty with the United States which the United States Treasury Department determines to be satisfactory for such purposes and which includes an exchange of information provision.

E&P calculation

GWL does not intend to calculate earnings and profits for U.S. federal income tax purposes. U.S. Holders should therefore expect the entire amount of any distribution on GWL Common Shares to be treated as a dividend for U.S. federal income tax reporting purposes. Dividends received by non-corporate U.S. Holders may be subject to an additional tax on unearned income of 3.8%.