Bacanora -- summary under New Non-Resident Holdco

Overview

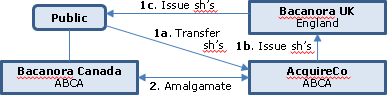

Bacanora Canada, whose key assets are Mexican subsidiaries holding lithium properties, is listed on the TSX, but its shares mostly trade on the AIM. It will effectively migrate to the UK under an Alberta Plan of Arrangement under which there will be a triangular exchange of shares with a newly-formed UK company (Bacanora UK) and a wholly-owned Alberta sub of Bacanora UK (Acquireco), so that the Bacanora Canada shareholders transfer their shares to Acquireco, Acquireco issues shares to Bacanora UK and Bacanora UK issues shares to the Bacanora Canada shareholders – with Bacanora Canada and Acquireco then amalgamating.

This exchange will occur on a taxable basis for Canadian purposes – and the AIM qualifies as a designated exchange for RRSP eligibility purposes. The U.S. tax disclosure indicates that there is substantial uncertainty as to whether the transaction qualifies as a s. 351 reorg given that there is a plan for Bacanora UK to do a substantial equity raise.

Bacanora Canada

An Alberta corporation listed on the TSXV and AIM whose head office and registered office is located in Calgary, Canada. Its principal assets are the Sonora Lithium and Magdalena properties in Mexico held in direct or indirect Mexican subsidiaries (with Cadence, another resource company, as a minority shareholder).

Bacanora UK

Bacanora Lithium Plc, a company incorporated under the UK Companies Act.

Acquireco

1976844 Alberta Ltd., a wholly-owned Alberta subsidiary of Bacanora UK Following the Arrangement, the amalgamated corporation resulting from its amalgamation with Bacanora Canada will be a wholly-owned subsidiary of Bacanora UK.

Bacanora Canada shareholders

The only two shareholders holding more than 10% of its shares are M&G Investments Fund ( an investment fund that is part of the Prudential Plc group of companies and is headquartered in London, UK) holding 10.04%) and 11.8% held by Igneous Capital Limited, a private corporation incorporated under the laws of the British Virgin Islands that is controlled by and ultimately beneficially owned by Mr. Edwards and a D&A Income Limited, which is in turn owned by a trust, of which Mr. Edwards is one of the potential beneficiaries.

Proposed financing

Having successfully completed the Feasibility Study on the Sonora Lithium Project, the Board intends to embark on a fund raising exercise in order to secure the US$419 million capital expenditure requirement to develop phase 1 of the Sonora Lithium Project and finance further work on the Zinnwald Lithium Project, irrespective of the approval of the Re-Domicile. It is intended that a substantial proportion of the funding will be raised through equity finance….

Reasons for transaction

Bacanora Canada currently incurs high costs associated with having a dual listing in AIM and on TSXV, yet Canadian shareholdings are estimated at less than 10% of Bacanora Canada’s shareholder base. Bacanora Canada now intends to raise a significant amount of new debt and equity financing to fund its growth as an international lithium company with new projects in Mexico and Germany and believes that a UK domiciled company with its primary listing on AIM is the best way to achieve this.

Plan of Arrangement steps

- Simultaneously with 2 and 3 below, each holder of a Bacanora Canada Share outstanding at the Effective Time, will transfer its Bacanora Canada Shares to AcquireCo in exchange for Bacanora UK Shares on the basis of one Bacanora Canada Share for one Bacanora UK Share;

- AcquireCo will issue that number of common shares of AcquireCo to Bacanora UK at a deemed value of $1.00 per common share of AcquireCo equal in value to the total number of Bacanora UK Shares issued by Bacanora UK to each Bacanora Canada Shareholder;

- In consideration of AcquireCo issuing its common shares to Bacanora UK, Bacanora UK will issue Bacanora UK Shares to each Bacanora Canada Shareholder in exchange for such Bacanora Canada Shareholder tendering its Bacanora Canada Shares to AcquireCo, on a one for one basis;

- The stated capital of the Bacanora Canada Shares shall be reduced, in the aggregate to $1.00;

- Bacanora Canada and AcquireCo shall be amalgamated as one corporation. The aggregate stated capital of the issued Amalco common shares will be an amount equal to the aggregate stated capital of the issued AcquireCo common shares immediately before this step.

Post-Arrangement steps

Following the completion of the Arrangement: (a) the outstanding options of Bacanora Canada under the option plan of Bacanora Canada, when exercised, will be exercised into Bacanora UK Shares, in accordance with the terms of the Bacanora Option Plan; and the restricted share units of Bacanora Canada under the RSU plan of Bacanora Canada when exercised, will be exercised into Bacanora UK Shares, in accordance with the terms of the Bacanora RSU Plan.

An application will be made to the London Stock Exchange plc for admission to trading of the Bacanora UK Shares on AIM.

Canadian tax consequences

Canadian resident non-exempts

A holder of Bacanora Canada Shares who is a Canadian resident and who receives Bacanora UK Shares pursuant to the Arrangement will realize a capital gain or capital loss on his Bacanora Canada Shares to the extent that the fair market value of such Bacanora UK Shares on the Effective Date exceeds (or is less than) the aggregate of the adjusted cost base to the holder of their Bacanora Canada Shares and reasonable costs of disposition.

RRSPs etc.

Provided the Bacanora UK Shares are listed on a designated stock exchange (which currently includes AIM), the Bacanora UK Shares will be qualified investments for Deferred Income Plans.

UK tax consequences

Disposal consequences

A Bacanora Canada Shareholder who, together with persons connected with him, does not hold more than 5% of shares in Bacanora Canada should not be treated as having made a disposal of his Bacanora Canada Shares for the purposes of UK taxation of chargeable gains to the extent that he receives Bacanora UK Shares in exchange for his Bacanora Canada Shares under the Arrangement. Instead, the Bacanora UK Shares will be treated as the same asset as his Bacanora Canada Shares, acquired at the same time as his Bacanora Canada Shares. Any Bacanora Canada Shareholder who, either alone or together with persons connected with him, holds more than 5% of Bacanora Canada Shares is advised that clearance has been sought from HM Revenue & Customs under section 138 of the Taxation of Chargeable Gains Act 1992 in respect of the Arrangement.

On-going treatment

The corporation tax rate applicable to Bacanora UK’s taxable profits is currently 19% and from 1 April 2020 the rate will reduce to 17%. For gains for an individual Bacanora UK Shareholder, the rate of capital gains tax on disposal of Bacanora UK Shares by basic rate taxpayers will be 10% and, for upper rate and additional rate taxpayers, the rate will be 20%.

US tax consequences

Qualification or not as s. 351 reorg

In order for the Arrangement to qualify as a s. 351 transaction, among other requirements, Bacanora Canada Shareholders who exchange Bacanora Canada Shares for Bacanora UK Shares under the Arrangement must acquire “control” of Bacanora UK as determined under s. 351 and the regulations issued thereunder. For this purpose, “control” is defined as the ownership of stock of Bacanora UK possessing (a) at 80% of the total combined voting power of all classes of stock of Bacanora UK entitled to vote and (b) at least 80% of the total number of shares of each other class of stock of Bacanora UK. In addition to other events, a financing by Bacanora UK under which Jersey shares are issued to investors, on, before or after the Effective Date, may prevent Bacanora Canada Shareholders who exchange Bacanora Canada Shares for Bacanora UK Shares under the Arrangement from acquiring “control” of Bacanora UK under s. 351. If the Exchange fails to qualify as a s. 351 transaction, then the Exchange would constitute a taxable disposition of Bacanora Canada Shares by a U.S. Holder.

PFIC rules

If Bacanora Canada were classified as a PFIC for any taxable year during which a U.S. Holder holds or held Bacanora Canada Shares, and if Bacanora UK also qualifies a PFIC for the taxable year that includes the day after the Effective Date of the Arrangement, then proposed Treasury Regulations generally would provide for the nonrecognition treatment of a s. 351 transaction to apply to such U.S. Holder’s exchange of Bacanora Canada Shares for Bacanora UK Shares pursuant to the Arrangement provided the Exchange otherwise qualifies as a s. 351 transaction. Based on current business plans and financial projections of the income and assets of Bacanora Canada and Bacanora UK, Bacanora Canada believes that there is a significant likelihood that Bacanora UK will be a PFIC for its current taxable year and Bacanora UK may constitute a PFIC in future taxable years.