Subsection 182(1) - Forfeiture, Extinguished Debt, Etc.

Cases

Agence du revenu du Québec v. FTI Consulting Canada Inc., 2022 QCCA 1740

The appellants (the “ARQ”) were owed approximately $13.4 million of tax by a corporation (“CQIM”) immediately before it was placed into...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Other Legislation/Constitution - Federal - Companies' Creditors Arrangement Act - Section 32 - Subsection 32(7) | CCAA did not establish that deemed GST payment under ETA s. 182 arose when the underlying contract was engaged | 363 |

| Tax Topics - Statutory Interpretation - Similar Statutes/ in pari materia | CCAA not in pari materia with ETA provisions | 173 |

Automodular Corporation v. General Motors of Canada Limited, 2018 ONSC 1640

The plaintiff (“Automodular”) brought an action against General Motors of Canada Limited and General Motors Company (collectively, “GM”)...

Re Ravelston, [2006] GSTC 124, 2006 CanLII 32429 (Ont Sup Ct J)

A Canadian registrant (RCL) provided management services under a management services agreement (the "MSA") with another Canadian registrant...

See Also

British Columbia Hydro and Power Authority v. The King, 2025 TCC 61

BC Hydro, which had entered into an electricity purchase agreement (EPA) with an independent power producer for the supply of electricity at a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | parol evidence could not be used to bifurcate a payment | 252 |

267 O'Connor Limited v. The King, 2024 TCC 161 (Informal Procedure)

In the settlement of an action against it by a third party (“Starwood”) for a failure of a property sale agreement to Starwood to close, the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 169 - Subsection 169(1) | damages paid by the vendor under a failed realty sale did not generate ITCs notwithstanding some IP transferred to it | 257 |

| Tax Topics - Excise Tax Act - Section 169 - Subsection 169(4) | failure of recipient to demonstrate that that it had the supplier’s registration number at the time of its return filing, or to have documentation of an allocation to the alleged taxable supply | 196 |

Autonum, Solutions de financement aux consommateurs inc. v. Agence du revenu du Québec, 2024 QCCQ 1195

An ARQ request to change the pleaded basis of the ARQ assessments from the QSTA equivalent of s. 168(9) to that of s. 182 was rejected in light...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(9) | ARQ request to change the sales tax provision on which its assessment was founded was rejected | 394 |

| Tax Topics - Excise Tax Act - Section 298 - Subsection 298(6.1) | request to change the basis of the ARQ assessments from s. 168(9) to s. 182 (ETA equivalents) was rejected | 314 |

BH Parkway Place Ltd. v. The Queen, 2019 TCC 7 (Informal Procedure)

Following the vacating by a tenant (“Trillium College”) of shopping-mall premises of the appellant (“BH Parkway”) in breach of the terms...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 201 | $74K SUV used for transporting goods was not subject to $30K cap | 233 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Automobile - Paragraph (e) - Subparagraph (e)(ii) | a Mercedes SUV used in transporting goods was not an automobile | 107 |

THD Inc. v. The Queen, 2018 TCC 147

The appellant, which had a trucking business, had a contract with a customer (“McKesson”) for the delivery of pharmaceutical products to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Regulations - Input Tax Credit Information (GST/HST) Regulations - Section 3 - Paragraph 3(b) - Subparagraph 3(b)(i) | requirement to obtain required information at time of ITC claim | 200 |

MEO — Serviços de Comunicações e Multimédia SA v. Autoridade Tributária e Aduaneira (2018), ECLI:EU:C:2018:942 (ECJ (5th Chamber))

Subscribers to the services of a Portuguese telecommunications company (“MEO”) agreed to pay for a minimum subscription period, and when they...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Consideration | payments pursuant to contract for remaining minimum service term were consideration | 463 |

Simon Fraser University v. The Queen, [2013] GSTC 57, 2013 TCC 121 (Informal Procedure)

The appellant, a university, maintained parking spaces around campus and imposed parking fines pursuant to special statutory authority. The signs...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 165 - Subsection 165(1) | 198 |

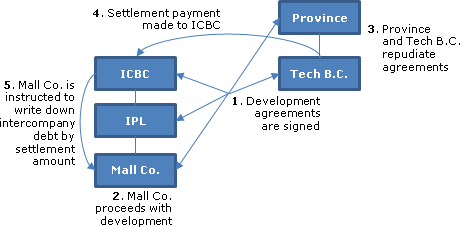

Surrey City Centre Mall Ltd. v. The Queen, 2012 TCC 346

{kind=link}

The appellant ("Mall Co"), its parent ("IPL"), which was the master real estate subsidiary of The Insurance Corporation of British Columbia...

Société en commandite Sigma-Lamaque v. The Queen, 2010 TCC 415

The appellant (“SL”) leased construction equipment (worth approximately $9 million) from Caterpillar for five years and provided Caterpillar...

Mi Sask Industries Ltd. v. The Queen, 2007 TCC 73 (Informal Procedure)

Under a contract of Mi Sask with the City of Medicine Hat for the construction of pipeline river crossings, the City was required to maintain...

Extendicare International Inc. v. Minister of Revenue, 2000 CanLII 5653 (Ont CA)

The appellant, which had been leasing computer equipment, notified the lessor that it would no longer be making the agreed monthly payments nor...

Low Cost Furniture Ltd. v. The Queen, [1997] GSTC 77 (TCC)

A $15,000 lump sum payment made by the registrant to its landlord in order to terminate its lease was found not to give rise to an input tax...

Administrative Policy

18 April 2023 GST/HST Interpretation 245056 - Application of the GST/HST on a rescission fee

S. 42(1) of the Property Law Act (B.C.) provides that a purchaser of residential real property generally may rescind the contract of purchase and...

26 July 2022 GST/HST Ruling 232189 - [Amounts charged as] […] Damages

The City’s construction agreements contained a liquidated damages clause, which required the contractor to compensate the City when work is not...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Supply | per diem damages received by a construction-services recipient for construction delays were free of HST | 161 |

25 March 2021 CBA Commodity Taxes Roundtable, Q.18

Aco (a resident registered corporation) agreed to make taxable supplies in Canada of tangible personal property to Bco (a resident registered...

10 February 2017 GST/HST Ruling 162056 - Application of the GST/HST to an investment transaction

A Canadian registrant (Investor) enters into “Agreement 1” with a Canadian corporation (Corporation 1) under which it pays lump sums in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Debt Security | royalty agreement is not a debt security unless a minimum royalty is specified | 267 |

| Tax Topics - Excise Tax Act - Section 169 - Subsection 169(1) | the purchase of an IP royalty gives rise to non-creditable GST/HST to the investor | 130 |

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Commercial Activity | receipt of royalty not considertion for a taxable supply | 121 |

7 December 2016 Ruling 158637

A registered charity which is also registered for GST/HST purposes charges employers or sponsors fees for providing training to apprentices and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Supply | contract cancellation fee not consideration for a supply | 117 |

| Tax Topics - Excise Tax Act - Schedules - Schedule V - Part V.1 - Section 1 | educational services not excluded | 25 |

| Tax Topics - Excise Tax Act - Section 232 - Subsection 232(1) | choice between supplier refund or recipient rebate | 108 |

B-109 "Application of the GST/HST to the Practice of Naturopathic Doctors" 31 July 2015

Other Charges

...A cancellation fee paid by a patient for a missed or cancelled appointment is treated as payment for the intended supply (i.e.,...

CBAO National Commodity Tax, Customs and Trade Section – 2014 GST/HST Questions for Revenue Canada, Q. 30.

Supplier agrees to deliver 100 widgets to the Recipient at $10 per widget, but is only able to obtain 20 widgets. An action of the Recipient is...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Supply | settlement of right to receive full widget shipment not a taxable supply | 108 |

8 March 2012 Ruling Case No. 137942 [payment, following breach by purchaser, for assignment of purchaser's rights in purchased equipment]

Company X agrees to supply and deliver equipment to Company Y under the "Supply Agreement," with title to pass to Company Y when the stipulated...

Policy Statement P-218R "Tax Status of Damage Payments not Within Section 182 of the Excise Tax Act", August 10, 2007.

Exclusion of certain damages

[S]ituations where one or more of the conditions in subsection 182(1) are not met ... include:

- no prior agreement...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Supply | 0 |

12 August 2003 Ruling Case No. 36831 [no-show charges]

Fees for "no shows" charged by a registrant in the business of conducting independent medical examinations for use by insurance companies and...

31 March 2000 HQ Letter 25522

A break-up fee (referred to as a "non-completion fee") paid in connection with an aborted merger of two companies did not represent consideration...

4 December 1998 Interpretation file no. 11585-1

A Canadian law firm was successfully sued for damages respecting its negligent advice on pension matters to a Canadian corporation that also was a...

13 March 1997 Interpretation 11735-1, 11720-1

A rented car is damaged, the car rental company pays a body shop for repairs plus GST, claims an ITC for such GST and then obtains recovery from...

21 December 1995 Ruling 940411 [tenant pays for improvements on lease termination]

An amount payable by a tenant on the termination of a lease, equal to the amortized value of leasehold improvements, would not be considered to be...