Cases

Macmillan Bloedel Ltd. v. R., 99 DTC 5454, [1999] 3 CTC 652 (FCA)

The taxpayer redeemed U.S.-dollar denominated preferred shares at a time that the U.S. dollar had appreciated relative to the exchange rate at the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(2) | loss on redemption of U.S.-dollar preferred shares | 101 |

See Also

McClarty Family Trust v. The Queen, 2012 DTC 1123 [at at 3122], 2012 TCC 80

A family holding company ("MPSI") paid a stock dividend of preferred shares, having nominal paid-up capital and a redemption amount of $48,000, on...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | 358 |

Gagnon v. The Queen, 2008 DTC 3111, 2006 TCC 194

The taxpayer originally signed an agreement for the sale of his half interest in a business (which was found to be held in a corporation) to his...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | person declared a shareholder retroactively | 149 |

MacMillan Bloedel Ltd. v. R., 97 DTC 1446, [1997] 3 C.T.C. 3012 (TCC), aff'd 99 DTC 5154

The taxpayer was found to have realized a capital loss under s. 39(2) rather than to have paid a deemed dividend under s. 84(3) when it redeemed...

Lalonde v. MNR, 90 DTC 1313, [1990] 1 CTC 2427 (TCC)

The taxpayer established that he purchased the shares of a fellow shareholder as agent for the corporation rather than as principal. Accordingly,...

Belair v. MNR, 89 DTC. 429, [1989] 2 CTC 2186 (TCC)

In the face of inadequate evidence, Morgan J. found that if the corporation had agreed to purchase for cancellation 1/3 of the taxpayer's common...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Legal and other Professional Fees | 60 |

Cabezuelo v. MNR, 83 DTC 769 (TCC)

The taxpayer received $25,000 in cash for shares plus a further balance payable over three years. After finding that these payments should be...

McArdle Estate [No. 2] v. MNR, 62 DTC 402 (TAB)

The president (McArdle) of a private company had been issued “employee redeemable shares,” whose terms provided that they participated on a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Substance | mistaken nomenclature ignored if inconsistent with governing intention | 66 |

Administrative Policy

29 November 2022 CTF Roundtable Q. 3, 2022-0949771C6 - Post-closing adjustments and the impact to escrow shares

Under an agreement for the sale of a corporation (Target) solely for shares of the purchaser, which were validly issued on the closing, a portion...

25 November 2021 CTF Roundtable Q. 1, 2021-0911841C6 - Indemnities and subsection 87(4)

There has been a triangular amalgamation under which a subsidiary of Parent amalgamated with Target and the Target shareholders received shares of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(4) | payment of damages, for breach of reps, by the parent following a triangular amalgamation would not preclude satisfaction of s. 87(4) | 242 |

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(1) | damages paid for breach of rep following an amalgamation did not breach s. 87(1)(a) | 144 |

27 November 2018 CTF Roundtable Q. 5, 2018-0780041C6 - GAAR on PUC reduction

Shareholders of DCco transfer shares of DCco having an aggregate PUC of $10,000 and an ACB of $1,000 and a FMV higher than $10,000 to TCco in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(b) | where Parent acquired the net tax equity in Subco at a bargain price (low share ACB), avoiding a s. 88(1)(b) gain on wind-up through reducing PUC is abusive | 548 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | avoidance of s. 88(1)(b) where insufficient safe income was abusive | 393 |

27 June 2018 External T.I. 2018-0745681E5 F - Wind-up of a partnership

A family farming partnership ("Partnership"), whose three partners equally owned the common shares of Opco, owned preferred shares of Opco, with a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(5) | s. 98(5) inapplicable on simultaneous dissolving transfer of partnership interests | 167 |

| Tax Topics - Income Tax Act - Section 28 - Subsection 28(1) - Paragraph 28(1)(f) | application of s. 28(1)(f) on partnership wind-up | 203 |

26 May 2016 IFA Roundtable Q. 3, 2016-0642111C6 - PUC of Shares of a FC Reporter

CRA considered that a Canadian corporation which has the U.S. dollar as its elected functional currency nonetheless is required to keep track of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 261 - Subsection 261(1) - Canadian Tax Results | deemed dividend calculation for shareholder not part of Cdn tax results | 323 |

2015 Ruling 2014-0532201R3 - Corporate reorganization

Towards the completion of an intricate internal reorganization for a privately-held Canadian corporate group, a newly-amalgamated corporation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 38 - Paragraph 38(a.1) | donation of pubco shares to foundation and immediate cash sale to affiliate | 521 |

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(1) - Total Charitable Gifts | donation and sale-back of public company shares | 85 |

S4-F7-C1 - Amalgamations of Canadian Corporations

1.5 …[S]ubsection 84(3) will not otherwise apply to deem a shareholder of a predecessor corporation to have received a dividend where the...

29 October 2013 External T.I. 2013-0507881E5 - Price adjustment clause

A price adjustent clause in the share provisions for preferred shares issued by Opco to the taxpayer in Year 1 in consideration for the transfer...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | 330 |

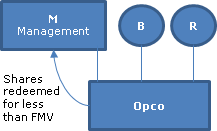

3 July 2012 Internal T.I. 2012-0450821I7 F - Interaction of 84(3) and 69(1)(b)

{kind=link}

A CCPC ("Opco"), whose voting common shares were owned by two individuals (B and R) and by a Canadian-controlled private corporation ("M Holdco")...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(b) | s. 69(1)(b) adjustment generates capital gain even though larger share redemption proceeds in the 1st place would have been exempt | 223 |

29 November 2011 Roundtable, 2011-0426361C6 F - Price adjustment clause and redemption of shares

Subsequent to an estate freeze, the freeze preferred shares were redeemed (in 2006). In 2011, it was determined that the redemption amount was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | deemed dividend through operation of price adjustment clause arises in the adjustment rather than redemption year | 63 |

21 November 2011 External T.I. 2011-0422191E5 F - Price adjustment clause and redemption of shares

if preferred shares with a redemption amount which is subject to a price adjustment clause are redeemed before there is an upward adjustment to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | additional payment, pursuant to price adjustment clause, in year following shares; redemption is recognized then | 54 |

23 July 2007 Internal T.I. 2007-0228601I7 F - Redemption of U.S. Denominated Shares

Parentco owned preferred shares of a subsidiary wholly-owned corporation (Holdco) denominated in U.S. dollars. Holdco purchased the preferred...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(2) | s. 86 exchange of US-dollar denominated prefs does not affect patrimony of issuer | 75 |

15 January 2007 Internal T.I. 2006-0216801I7 - Redemption of US $ Denominated Shares

Confirmation of a previous position that in light of the MacMillan Bloedel decision, CRA intends to assess any redemption of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(2) | s. 39(2) application on USD pref redemption, cf. if USD common shares | 77 |

28 October 2005 External T.I. 2005-0145891E5 F - Redemption of Shares - Balance of Purchase Price

On January 1, 2005, Canco purchases for cancellation 100 common shares, having a fair market value of $100,000, in consideration for paying...

2004 APFF Roundtable Q. 15, 2004-008682

Respecting the situation where a subsidiary purchases for cancellation a portion of the common shares in its capital held by its wholly-owning...

31 December 2004 Internal T.I. 2004-0091781I7 - Redemption for Proceeds Less than FMV

In a situation where preferred shares were redeemed for an amount less than the fair market value, the Directorate stated that "where, in a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(b) | s. 69 rather than s. 84(3) applies where FMV excess | 135 |

10 October 2003 Roundtable, 2003-0030005 F - $500,000 Deduction - Application of GAAR

A purchaser is interested in purchasing an operating subsidiary ("Opco") of a management corporation ("Managementco") and not Managementco....

1 November 2002 External T.I. 2002-0146775 - Share Sale by Employees Yields Cap. Gain

Where employees of Opco (who as a group, own 14% of its issued common shares) are terminated, they are required to sell their Opco common shares...

2002 Ruling 2002-0138993 - XXXXXXXXXX . - 95(2)(a)(ii)(D)

A foreign subsidiary ("Holdco") which is making a takeover bid for a public corporation in the same foreign jurisdiction ("Targetco'), acquires...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(a) - Subparagraph 95(2)(a)(ii) - Clause 95(2)(a)(ii)(D) | 110 |

10 August 2000 External T.I. 2000-0016875 - SAR DISPOSITION, SHARES

"Where an employee has income from employment under paragraph 7(1)(a) related to the disposition, by virtue of subsection 7(1.1), of shares and a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | 83 | |

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(3) - Paragraph 7(3)(a) | 36 |

26 October 1998 Internal T.I. 9803947 - REDEMPTION OF SHARES

Where shares held by a financial institution are redeemed, s. 84(3) will be considered to take precedence over s. 142.5(1), and s. 248(28) will...

6 June 1997 Internal T.I. 9631867 - REDEMPTION OF SHARES HELD BY FINANCIAL INSTITUTIONS

S.142.5(1) takes precedence over s. 84(3). To the extent that an amount has been included in computing income under s. 142.5(1), such amount will...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 142.5 - Subsection 142.5(1) | 38 |

6 July 1995 External T.I. 9316465 F - Payment to Dissenting Shareholders on Amalgamation

In response to a proposal that a payment be made to a separated wife of a husband by her dissenting to the amalgamation of a corporation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 153 |

12 August 1994 External T.I. 9415495 - AMALGAMATION/WIND-UP

Where there is a wind-up of a wholly-owned subsidiary that also owns shares of its parent, s. 84(3) will not apply to the subsidiary because the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(1) | 89 | |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) | 68 |

30 March 1994 External T.I. 9337225 - SHARES HELD AS INVENTORY

On the redemption of shares held as inventory, a deemed dividend will arise pursuant to s. 84(3) and, to the extent that the paid-up capital of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Computation of Profit | 72 |

93 C.R. - Q. 56

Cash payments received from an amalgamated corporation for shares held by shareholders dissenting from the amalgamation will be proceeds of...

3 September 1991 T.I. (Tax Window, No. 8, p. 21, ¶1436)

S.84(3) does not apply to deem a dividend to have been paid when shares of a corporation owned by its wholly-owned subsidiary are cancelled on the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) | 32 |

3 July 1991 T.I. (Tax Window, No. 5, p. 13, ¶1334)

S.84(3) does not apply to an amalgamation to which s. 87 applies.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(2) - Paragraph 87(2)(a) | 23 |

31 May 1990 T.I. (October 1990 Access Letter, ¶1469)

With respect to an argument that where a corporation purchases for cancellation only some of the shares of a given class and pays an amount...

87 C.R. - Q.59

A shareholder dissenting pursuant to s. 184 of the CBCA who receives cash from the amalgamated corporation realizes proceeds of disposition rather...

87 C.R. - Q.69

Where a share having a high stated capital and low paid-up capital is exchanged in a s. 86 reorganization for another share with a high stated...

84 C.R. - Q.45

The calculation of the amount of the dividend arising on a purchase for cancellation will include the value of any type of consideration given for...

Articles

Didier Fréchette, Ryan Rabinovitch, "Current Issues Involving Foreign Exchange", 2015 CTF Annual Conference paper

Whether deemed dividend on redemption of USD preferred shares (pp. 26:35-39)

A Canadian-resident corporation issues preferred shares for US$100...